Select Citi/AAdvantage cardholders targeted for temporary 5x bonus on online spending

Update: Some offers mentioned below are no longer available. View the current offers here.

Editor's note: This post has been updated with the latest credit card information. Citi is a TPG advertising partner.

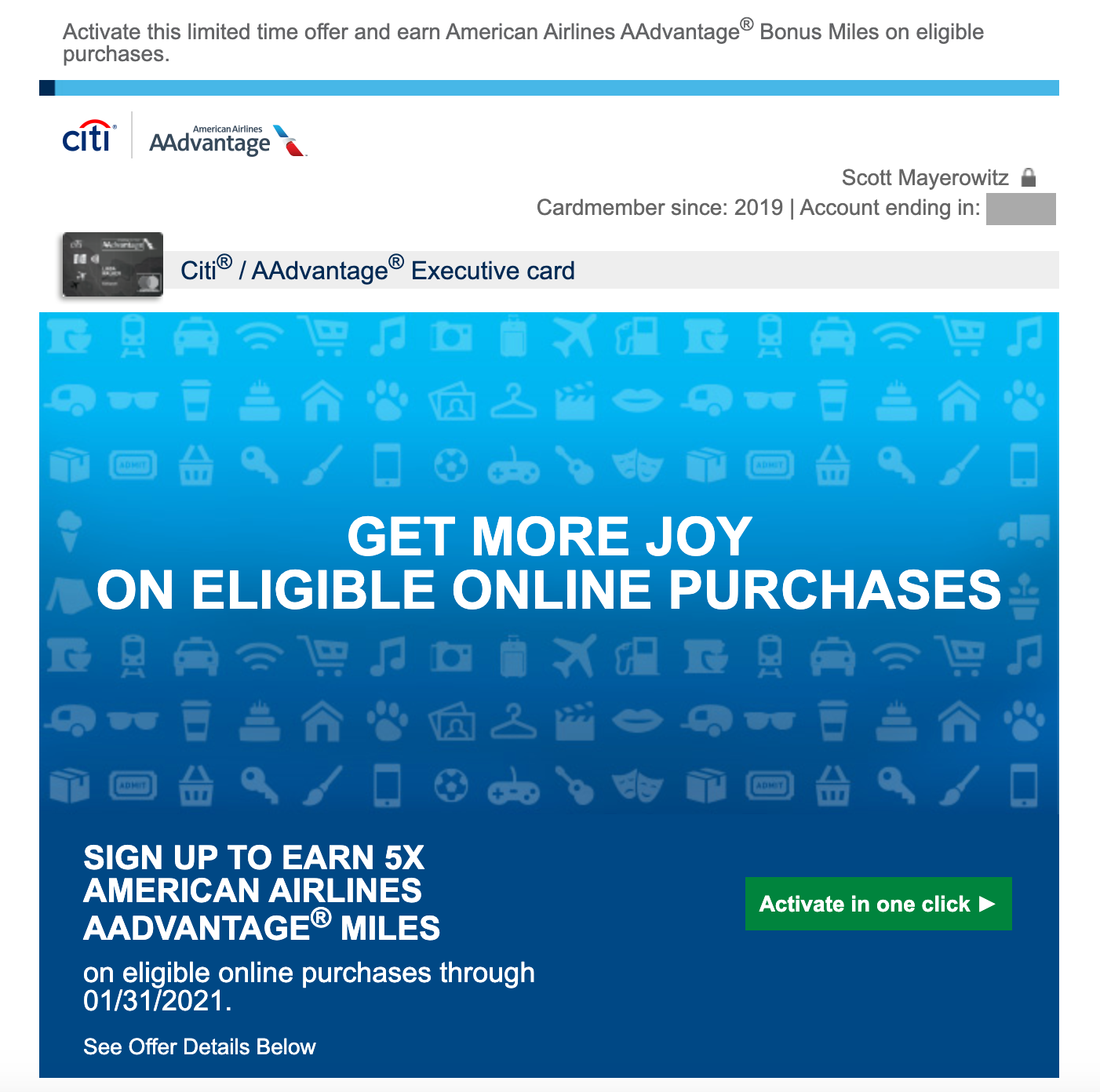

Check your emails! Citi sent out another round of what appears to be targeted offers to Citi® / AAdvantage® Executive World Elite Mastercard® cardholders.

On the Citi/AAdvantage Executive Card, targeted cardholders are being offered 5x miles across online purchases. Online spending is a broad category, but Citi lists the following as examples of qualifying purchases:

- Purchases made at your favorite retailer's website

- Online drugstore orders (including prescription orders made online)

- Online grocery orders

TPG Executive Editorial Director Scott Mayerowitz received the offer today with a special one-click link to activate. According to the email he received, targeted cardholders have until Dec. 15, 2020, to enroll their card and until Jan. 31, 2021, to take advantage of the spending bonus.

Is this offer worth moving your spending?

While 5x is an impressive earning multiplier — especially across such a broad category such as online spending — the spending cap is a bit disappointing. In line with previous Citi/AAdvantage 5x earning offers, it states you can earn up to 2,500 miles in combined bonus category spending, which equates to just $500 in spending. TPG values AAdvantage miles at 1.4 cents each, meaning those who max out this offer will only earn a total of $35 in additional rewards.

Considering the number of cards currently offering temporary bonus categories during the coronavirus pandemic, this offer may not be enough to tempt people to switch spending to this card versus others offering higher spending caps for temporary categories. Plus, there are some cards that offer better spending across some online purchases.

For example, if you are a new cardholder of the Chase Freedom Flex or Chase Freedom Unlimited, you can get 5% back on up to $12,000 spent in the first year (which is really 5x — and a 10% return according to TPG valuations — if you also have a card that earns Ultimate Rewards such as the Chase Sapphire Preferred Card) on groceries, which includes any online grocery orders from platforms that code as groceries (which generally includes Instacart). Freedom Flex and Freedom Unlimited cardholders also get 3% back on drugstores (a 6% return if you have an Ultimate Rewards card), which would include any online drugstore purchases.

However, if you don't have a card that offers a better return on certain online purchases, getting 5x on your eligible Citi/AAdvantage card certainly beats the 1x or 1% you'd earn otherwise.

Bottom line

With spending habits changing for many cardholders this year, card issuers have launched a number of new ways for customers to earn rewards in order to encourage spending on cards that otherwise would have been resigned to the sock drawer in 2020. This isn't the first round of 5x categories Citi has sent out for its AAdvantage cardholders — back in September, many cardholders were targeted to earn 5x at restaurants, grocery stores, gas stations, drug stores and mass transit.

Citi is neither the first nor my guess the last issuer we'll see add temporary spending categories this year. We've seen Chase dominate in this area, consistently offering cardholders new ways to earn rewards across both branded and cobranded card options. Some Amex and Capital One cards have also been among those to get temporary bonus categories and other related perks added.

While 5x on certain non-travel categories is definitely a nice temporary offer, the 2,500-mile earning cap dulls some of my excitement for this offer.