The credit reporting agency your bank uses matters — here's why

Editor's Note

One of the most important things to know when you apply for a credit card is which credit bureau the bank uses to pull your credit report.

Your credit report is a detailed record of your credit history that can determine whether or not you are approved for a new line of credit, such as a credit card.

In the U.S., there are three major credit bureaus — also known as credit reporting agencies — that banks and credit card companies can pay to access your credit report: Equifax, Experian and TransUnion.

Related: How to check your credit score for free

The credit reporting agency (CRA) used by a card issuer to see your credit report can determine whether your application is approved or denied, especially when you apply for various cards in a short period of time. If several card issuers pull from the same credit reporting agency, it could affect your chances of being approved.

However, if card issuers go to different credit bureaus to buy your reports, one issuer might not see that you're applying for a new account elsewhere. As a result, your chances of being approved for several cards should increase.

Multiple credit applications may reduce your score, so it's important to know what you're getting into before you decide to apply for several cards at once.

Before you apply for a new line of credit

Knowing where your credit stands before applying for any type of new credit is critical. Make sure to check your credit score and reports before you fill out a new application.

Check your credit report

Your credit report is a record of your credit activity, including your payment history, outstanding debts and credit inquiries. Understanding your credit health gives you a better idea of how your application may look to potential credit card issuers. Fortunately, checking your three credit reports is easy.

You can request a free report from Equifax, TransUnion and Experian once every 12 months online at AnnualCreditReport.com.

Related: How to correct errors on your credit report

Check your credit score

While your credit report paints a detailed picture of your credit history, it does not typically include your current credit score, so you'll want to check that too.

Checking your credit score, however, can be a bit more complex. Instead of just three scores — one for each of your credit reports — there are hundreds of commercially available credit scores, and some lenders even use their own custom models. This means there are thousands of possible credit score variations.

The two most widely used credit score models in the U.S. are FICO and VantageScore. VantageScore, created by the three major credit bureaus, has been gaining in popularity since its launch in 2006.

However, FICO remains the industry standard, with 90% of lenders relying on it for credit decisions. Many banks offer free FICO scores to cardholders as a helpful perk.

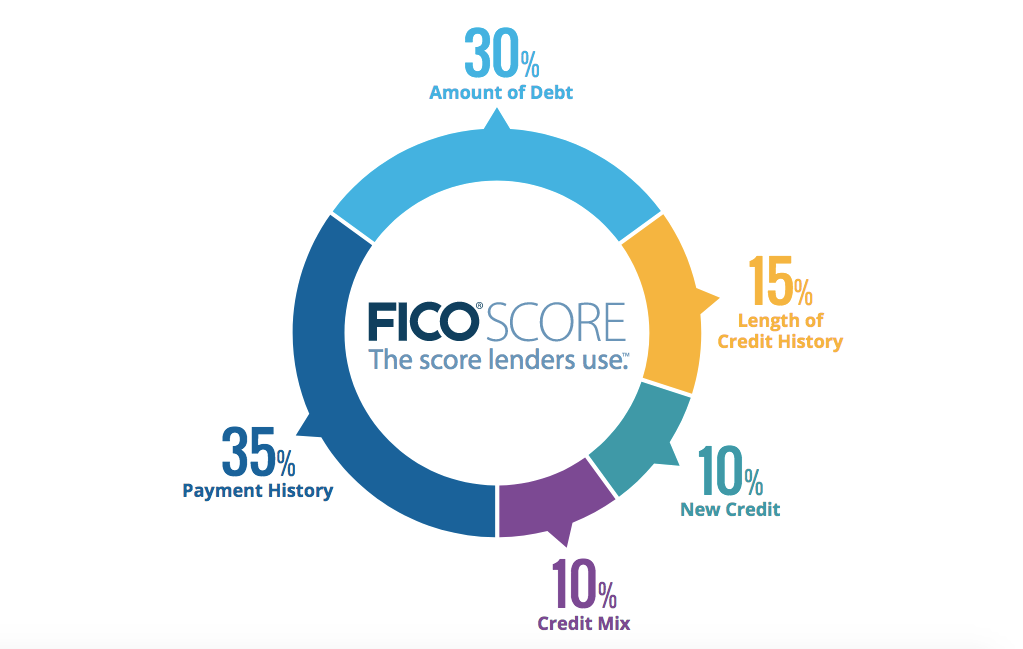

What is a FICO score?

Your FICO score is a number between 300 and 850 based on the information in your credit report.

FICO scores are calculated using many different pieces of credit data in your credit report. This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%).

Lenders use this score to assess your creditworthiness — the higher your score, the better your chances of getting approved for credit cards and other loans.

According to FICO, a "good" credit score falls between 670 and 739, while a score of 740-799 is considered "very good" and 800+ is considered "exceptional." However, chasing a perfect 850 score isn't necessary. In most cases, credit card issuers don't differentiate much between scores above 720, so a strong score in this range is typically enough to secure the best offers.

Which credit bureaus do banks check — and why does it matter?

When you apply for a credit card, the issuer contacts a credit bureau (or several) to purchase a copy of your credit report. Included in your report are the five categories mentioned above.

Related: What is a good credit score?

You'll notice one credit report category, which counts for 10% of your score, is called "new credit." If you have too many credit applications opened within a short period of time, it may affect your credit score negatively.

Imagine the following scenario: You've filled out several applications for new credit (think loans or credit cards) in the last 12 months. These applications show up on your credit reports as "hard inquiries" and could potentially damage your credit score.

You then decide to apply for another new credit card. In addition to your score potentially taking a hit, you might experience another road block.

The bank processing your application might be concerned about why you're applying for so much new credit in a short period of time. As a result, there's a chance you could be turned down for a credit card even if your credit score is in good shape.

Knowing which credit reporting agency card issuers use to pull reports might help you avoid this problem. With this knowledge in hand, you can time your applications (or bundle them, as the case may be) in such a way that you improve your approval odds for the credit cards you want.

Related: 5 things to check before applying for your next credit card

Many credit card companies tend to rely on one bureau when they process credit card applications. The credit bureau they use to buy reports, however, may differ depending on the state you live in and the specific credit card you want.

Here are the credit bureaus commonly used by three popular issuers:

- Citi uses all three credit bureaus, but usually pulls credit reports from Equifax or Experian.

- American Express uses all three credit bureaus but primarily pulls reports from Experian, though sometimes Equifax or TransUnion as well.

- Chase uses all three credit bureaus but favors Experian, yet may also buy Equifax or TransUnion reports.

However, keep in mind that you can never know for sure which credit bureau a credit card company will use.

Bottom line

Your credit report is a key part of your financial profile that can have a notable impact on your creditworthiness. By understanding which credit reporting agency banks use to review your credit, you may be able to increase approval odds on your next credit card application.

Related: 4 common credit score myths