Common credit card mistakes and how to avoid them

We've partnered with American Express to bring you personal finance insights, advice and more. Check out Credit Intel, Amex's financial education center, for more personal finance content.

One of our primary goals here at TPG is to demystify the world of credit cards in order to help people travel the way they want without breaking the bank. That often requires overcoming a lifetime of misconceptions about how credit cards work and building good habits moving forward.

No matter how easy we make it look, there are a number of mistakes that can derail your plans if you aren't careful. Today, we're going to take a look at some common credit card mistakes and how you can potentially avoid them.

Carrying a balance

Whether you're looking to earn travel rewards, cash back, or simply use credit cards as a cash flow management tool, carrying a balance from month-to-month works against your goal of earning valuable travel rewards. No matter how many points or miles you earn from a credit card, the rapidly compounding interest charges you accrue when you carry a balance will likely wipe away any gains and put you squarely in the red.

Some of the most popular travel rewards credit cards also have the highest interest rates, often north of 20%. That number might seem abstract, but here's a quick way to understand how fast your bills will go. Whenever you're dealing with compound interest, be it the return on an investment or how fast your loan balance will grow, you can use the "rule of 72." Simply divide 72 by the interest rate, and that's how fast it will take your balance to double. This means that a credit card balance with a 20% APR will double about every 3.6 years, with new hefty interest charges getting added each month.

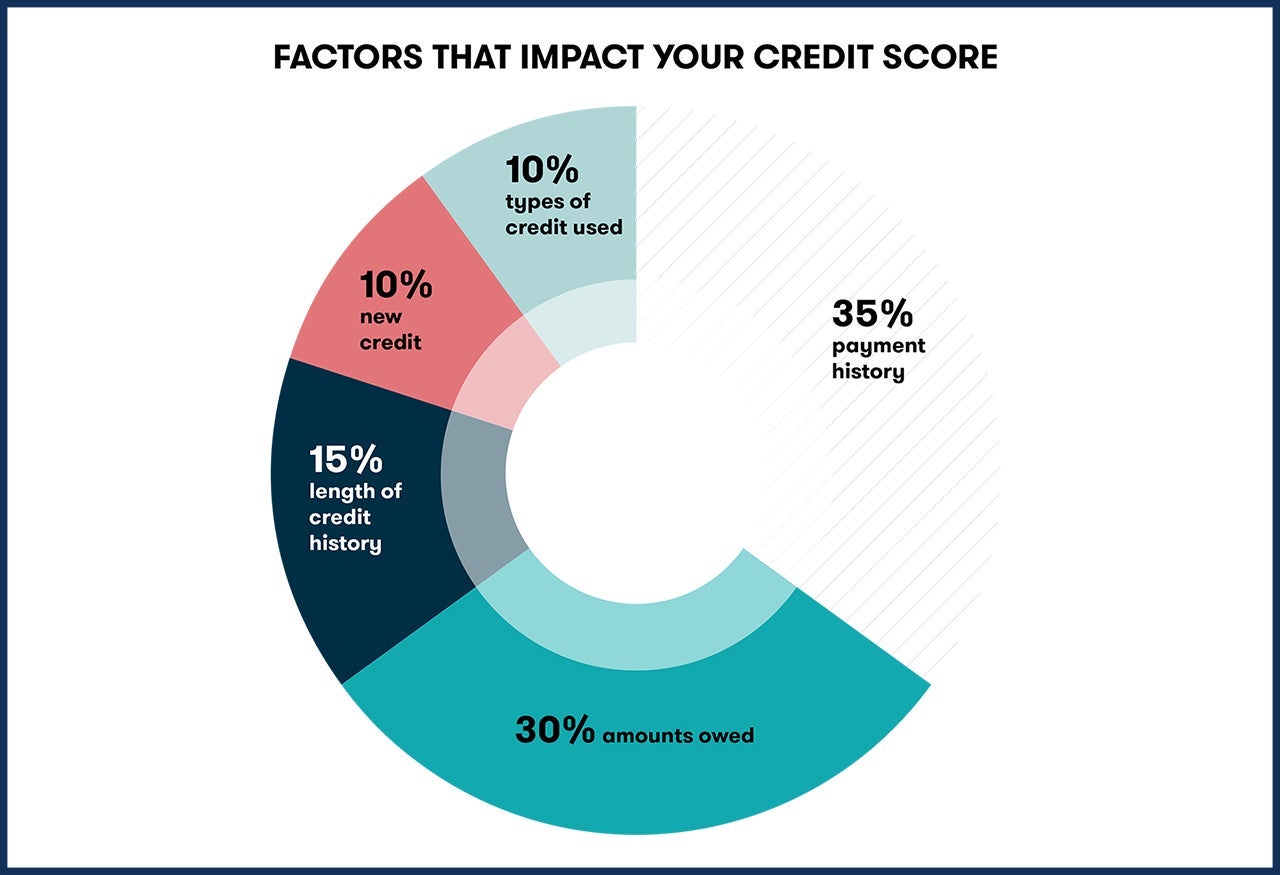

This is to say nothing of the negative impact to your credit score. 35% of your score is related to your payment history, making it a significant category. Since your credit score affects your ability to buy a house or get a car loan, it's especially important to pay your bills on time and keep your credit score in top shape.

Simply put, you should do everything in your power to pay your credit card bills on time. If you're currently carrying balances on your credit cards, you should also try and understand why before applying for a new credit card and exposing yourself to more risk.

Still, there are tens of millions of people around the world who use their credit cards responsibly. While you should be aware of the risks involved if you miss a payment, that alone shouldn't deter you from applying for a credit card and pursuing travel rewards. If you are getting a credit card for the first time and worried about staying on top of everything, here are a few suggestions to make your life easier:

- Set up autopay. This is one way to backstop your account and make sure you pay on time, but you will have to make sure you have sufficient funds in your checking account to cover the bill.

- Change your statement end date. Most credit card companies will let you change the date your statement closes. I set all my cards up to close on the 1st of the month, and I have a recurring reminder set for the 5th of every month to log in and check my bills. This gives me a few weeks to sort out my payments.

- Understand how long you have to pay your bill. With most credit cards, you'll have roughly a month from the end of your billing statement until your bill is due. Make sure you circle that date on your calendar so there are no last-minute surprises.

Further Reading: How and When to Pay Your Credit Card Bill

Not earning your welcome bonus

While there are lots of reasons to pick one credit card over another, one of the most immediate considerations is the welcome bonus you can earn. Most cards follow a similar script when offering welcome bonuses: "spend $X,000 in the first 3 months, earn a certain amount of points or a cash back reward."

These bonuses are one-time offers, and if you miss the cutoff you're out of luck when it comes to a pretty significant haul of points, often worth hundreds or even thousands of dollars. While most issuers follow this same template, some use a 90-day window instead of three months, and many issuers have started switching to tiered bonuses that require more spending over a longer amount of time. It's also worth noting that the clock starts ticking when your account is approved and opened, not when you physically receive the card which can often be 7-10 days later.

After you get your new credit card, it's a good idea to take out a calendar and circle the deadline you have for earning your welcome bonus. If you're not 100% sure or don't trust your own math, you can call or chat your issuer and they can provide it for you (this has the added benefit of giving you written proof if there are any discrepancies down the road).

When it comes to making sure you meet that new spending requirement you have two jobs: keeping an eye on the calendar, and making sure all of your charges post on time the way you expect them to. Some online retailers won't charge your card until an item ships, and some travel providers may not pre-charge you for future travel. This means that even though you're swiping your card now, the transaction could fall outside of the three month window.

What this means is that if you have the intention of earning the welcome bonus and you plan to meet the minimum, it may be helpful to have a plan in place, before you apply for the card, for how you can meet the minimum spending requirement that is connected to that welcome offer. While some people naturally spend $3,000-$5,000 over a three month period, not everyone does.

Further Reading: What Credit Card is Best for You in 2020?

Not understanding how your credit score works

Many of the myths, misconceptions and mistakes that people make with credit cards come from not understanding how their credit score is calculated. Many things are likely to affect your credit score, from opening and closing an account to making charges and paying off your balance. It's important that you understand how a score is calculated and how often a score updates, so you can differentiate between the transient (and rather meaningless) score changes, and the more serious ones that require attention.

Further Reading: 7 Best Ways to Help Build Your Credit

Here are a few important things you should consider before you start applying for credit cards, though this is by no means an exhaustive list:

- Your score goes down when you submit a new application. That new inquiry may cause a roughly 5 point drop in your score, though it will fade over time. Within two years your score will be back to normal and the inquiry will disappear from your report entirely.

- Your score will fluctuate month to month depending on how much you spend as your card issuer reports your utilization (total balance divided by available credit) to the credit bureaus. This can be scary, especially if you spend more than usual one month and your score takes a 10-20 point drop. It's important to remember that this is transient, and once you pay off your balance your score will go back up. Some people like to pay down their balances entirely a few days before the statement closes to avoid this volatility. While that might be a good idea if you plan on buying a house or car in the near future, it's probably not worth the extra work otherwise.

- Adding an authorized user can affect your credit score. When you add an authorized user, your entire account (payment history, account age, etc.) usually gets added to your credit report. This can be a great way to boost the score of someone who is just starting out in the world of credit cards, but it might preclude them from applying for that same card. As a general rule of thumb, if you want to apply for a credit card but you're an authorized user on that same card, you should remove yourself from the account and wait 3-6 weeks.

Further Reading: How Often Does A Credit Score Update?

Missing out on bonus points and credit card perks

Another major shift that we're seeing in the world of credit card rewards is issuers opting for more premium cards that come with more perks and bonus categories, and steeper annual fees. This can work out in the consumer's favor, but if you're paying $400 or more each year just for the privilege of using a credit card, you better make sure you're getting at least that much value from it each year.

Premium credit cards these days offer a myriad of annual statement credits, many of which are travel or retail related. This can serve as a dollar for dollar way to reduce your out-of-pocket cost each year, though you have to stop and ask yourself whether you would have shopped with that merchant if you weren't getting it "for free."

The same goes for credit card bonus categories. While you might not be able to recoup the value of a hefty annual fee through statement credits and perks alone, take a look at how much you spend in that card's bonus categories and calculate the value of the rewards you're earning compared to your next best option. If you're a big spender in a 4x or 5x category, that can easily add up to a few hundred or thousand dollars a year in bonus value.

While the premium credit card market lay dormant for decades, people are rapidly coming around to the idea that they can actually come out ahead, even when they're paying high annual fees. That being said, you have to look at your own personal situation and make sure you're remembering to use every perk the card has in order to get the best value possible.

Further Reading: 7 Ways to Get More from Your Travel Points Credit Card

Bottom line

Credit cards can be scary if you've never used them before, and a healthy dose of skepticism can help you avoid making some pretty serious mistakes. If you're still feeling hesitant about diving into the world of credit card rewards, the best antidote is knowledge. The more you learn about how credit scores are calculated, how welcome bonuses are awarded and how card benefits and bonus categories work, the better you'll be able to do for yourself and the easier a time you'll have avoiding these common mistakes.