How many credit cards do you have?

Update: Some offers mentioned below are no longer available. View the current offers here.

When I discuss credit cards with friends and other travelers, I'm frequently asked: "How many credit cards do you have?" I have 14 open accounts. And, some staff at The Points Guy have even more cards, including TPG Executive Editorial Director Scott Mayerowitz, who has 19 cards.

Scott and I are the outliers -- the vast majority of The Points Guy readers and American consumers have far fewer cards. So, to assess the average American consumer's credit card usage, The Points Guy recently commissioned YouGov to conduct a survey on credit cards. Today, we'll recap the results.

New to The Points Guy? Sign up for our daily newsletter and check out our beginner's guide.

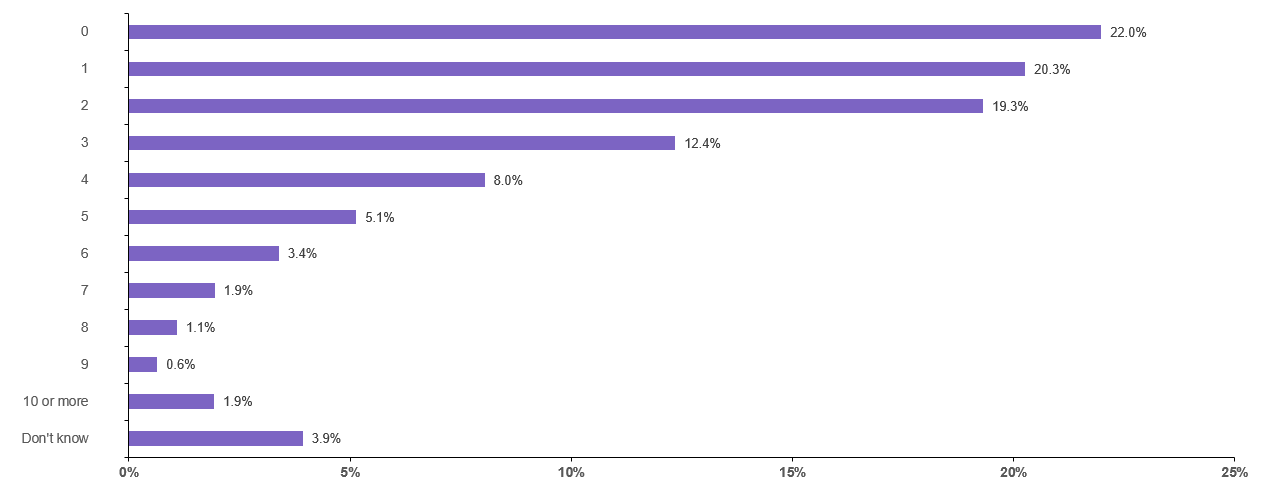

Number of credit cards

Question: How many credit cards do you have?

Our survey found that 22% of U.S. adults don't have a credit card. There are various reasons why it makes sense to have at least one credit card, even if the card is secured or an authorized user account. If you don't have a credit card yet, here are some of our top picks for your first card, as well as some of the common mistakes to avoid with your first card.

As you can see in the graph above, most U.S. adults who have a credit card only have a couple of cards. There's no set number of cards you should have, since this is a personal decision that's dependant on your lifestyle and preferences.

Related reading: How to assess and build your credit card portfolio

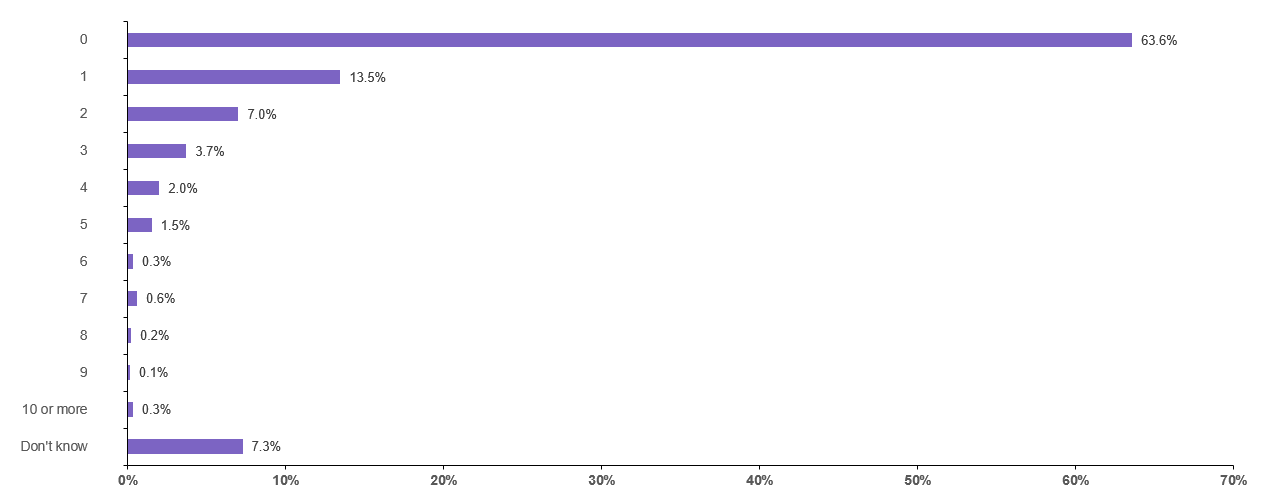

Number of premium cards

Question: How many of your cards are premium cards (i.e., have a $300 or higher annual fee)?

As you can see, 63.6% of U.S. adults with at least one credit card have no premium cards. If you've been reading The Points Guy for a while now, you know that premium travel rewards cards such as the Chase Sapphire Reserve, The Platinum Card® from American Express and The Hilton Honors American Express Aspire Card offer excellent benefits and earnings that can be worth well more than the annual fee for cardholders that can use and get significant value from these perks. The information for the Hilton Aspire Amex card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Considering that there are some excellent travel rewards cards with annual fees under $300 — such as the Chase Sapphire Preferred Card, American Express® Gold Card and the American Express® Green Card — it's not that surprising to learn that 63.6% of U.S. adults who have at least one credit card don't have a premium credit card with an annual fee of $300 of more. Perhaps more surprising is that 7.3% of U.S. adults who have at least one credit card don't know how many cards they have with annual fees of $300 or higher.

The information for the Amex Green Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related reading: Battle of the premium travel rewards cards: Which is the best?

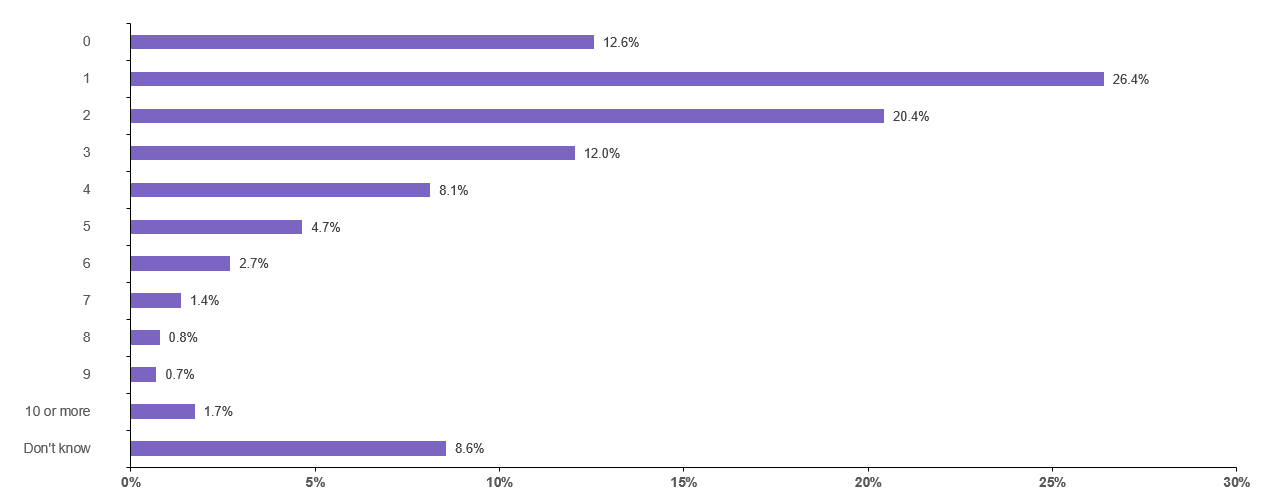

Number of no-annual-fee credit cards

Question: How many no-annual-fee credit cards do you have?

Out of U.S. adults with at least one credit card, 12.6% have zero no-annual-fee cards, 26.4% have one and 20.4% have two such cards. No annual-fee cards are easy to carry in your wallet long term, since there is no cost to carry them – some even earn valuable rewards.

If you are one of the 12.6% of U.S. adults with at least one credit card but no no-annual-fee cards, you may want to consider whether a no-annual-fee card in the same rewards family can boost your earnings. For example, if you have the Chase Sapphire Reserve or the Chase Sapphire Preferred, you can boost your Chase Ultimate Rewards earnings by adding the no-annual-fee Chase Freedom (No longer open to new applicants) and Chase Freedom Unlimited cards to your wallet and using them for purchases on bonus categories and regular spending. The information for the Chase Freedom has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related reading: The best no-annual-fee credit cards

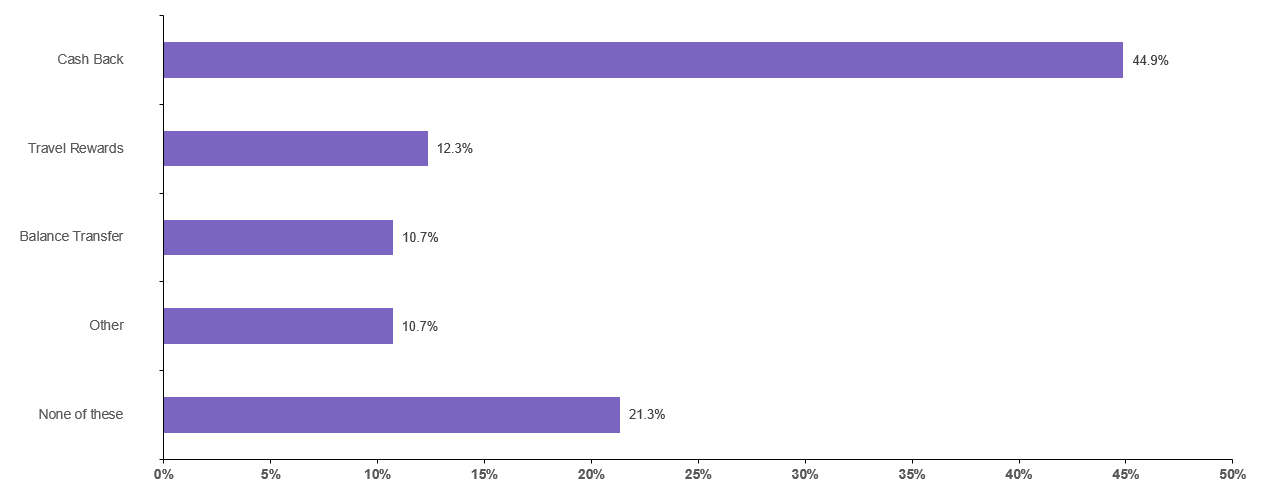

Goals when choosing a credit card

Question: Which of the following is your main goal when choosing a credit card?

When choosing a credit card, 44.9% of U.S. adults who have at least one credit card said that earning cash back is their primary goal, followed by 12.3% who are primarily interested in travel rewards and 10.7% who are primarily interested in balance transfer opportunities. Out of the options written in for those responding other, the primary concerns were low interest rates and no annual fee.

Related reading: Cash back vs. points and miles credit cards: The pros and cons of each

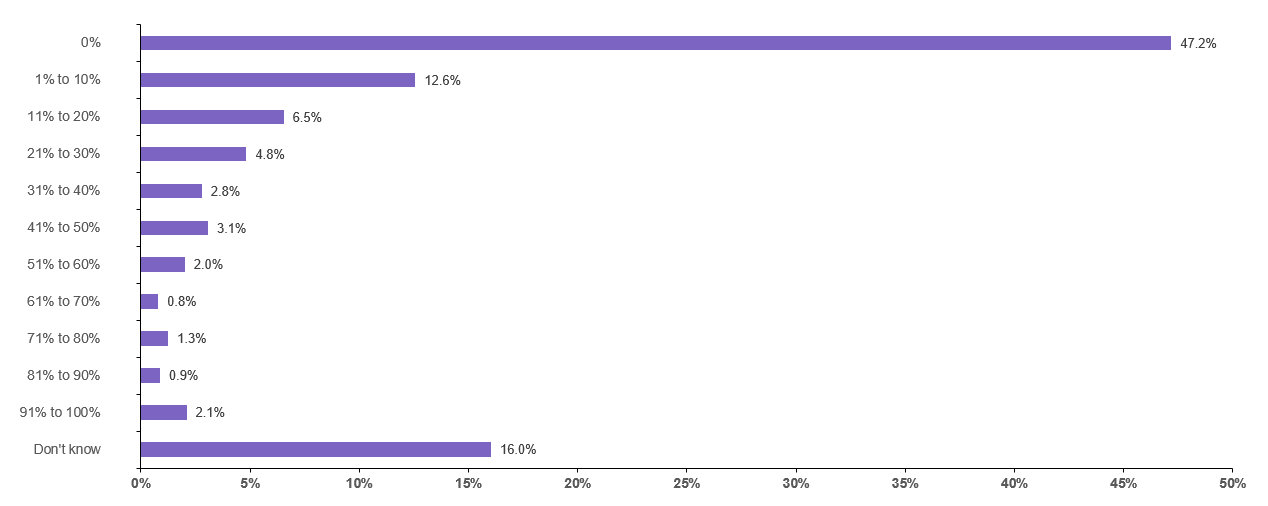

Frequency of using contactless payment in-store

Question: What percentage of your in-store credit card payments would you say are contactless (i.e., just tapping your card, Apple Pay, Samsung Pay, etc.)?

Despite many cards now having contactless chips, smartphones offering mobile wallet functionality and an increasing number of businesses supporting contactless payment, 47.2% of U.S. adults with at least one card reported that they use contactless methods for 0% of their in-store purchases. And, only 2.1% of U.S. adults reported they use contactless payment methods for 91% to 100% of their in-store purchases.

Related reading: Best contactless credit cards: Tap to pay

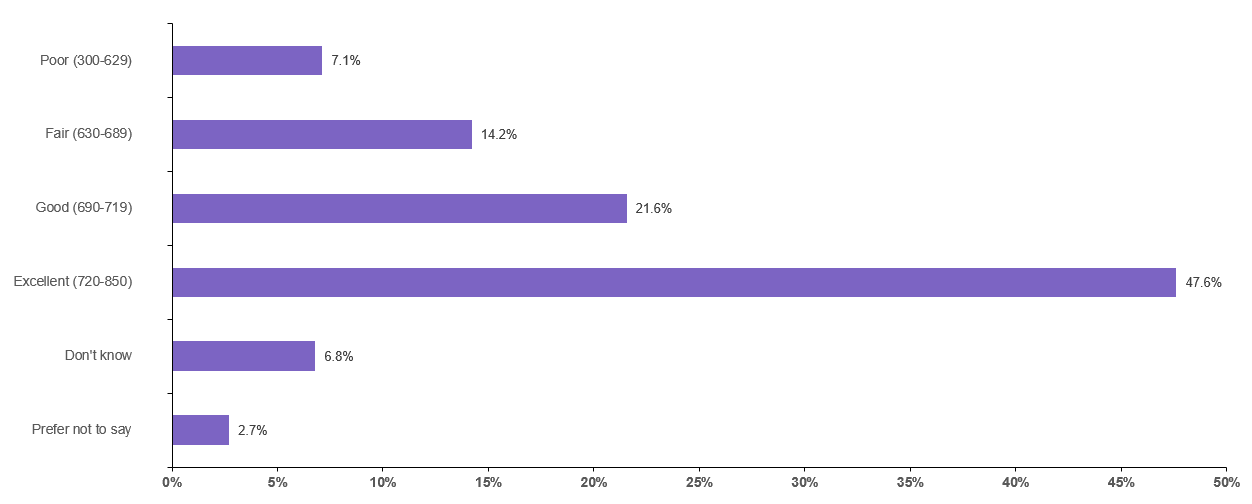

Credit score range

Question: To the best of your knowledge, what's your credit score range?

Out of U.S. adults who have at least one credit card, 7.1% report to have poor credit (300-629 credit score), 14.2% report fair credit (630-689), 21.6% report good credit (690-719) and 47.6% report excellent credit (720-850). You might be surprised to see that only 7.1% report to have poor credit, but remember that this percentage only considers U.S. adults with a credit card.

You may still be able to get a credit card with less than excellent credit. But, higher credit scores certainly unlock more and better card options. So, it's worth taking the time to understand how credit scores work and determining whether you can improve your credit score.

For the 6.8% of U.S. adults who have at least one credit card but don't know their credit score range, remember that some cards provide your FICO score for free. Plus there are plenty of other ways to check your credit score for absolutely free.

Related reading: 5 ways to improve your credit score

All figures, unless otherwise stated, are from YouGov Plc. The total sample size was 2,447 adults. Fieldwork was undertaken between 25th - 27th March 2020. The survey was carried out online. The figures have been weighted and are representative of all U.S. adults (aged 18+).