Here's why you still earn points on purchases made in a foreign currency

Update: Some offers mentioned below are no longer available. View the current offers here.

Reader Questions are answered twice a week by TPG Senior Points & Miles Contributor Ethan Steinberg.

While credit cards make it easy to spend money abroad, there are a few things you'll want to pay close attention to. For starters, you'll want to make sure you're using a card that doesn't charge any foreign transaction fees, and you'll want to avoid getting scammed by dynamic currency conversion or DCC (when asked, make sure to always pay in the local currency, not in your home currency). TPG reader Adham wants to know if he'll earn points on purchases made in a foreign currency...

[pullquote source="TPG READER ADHAM"]A Chase rep once told me that purchases made in local currency (rather than in U.S. dollars) are *not* eligible for bonus points — for example, the extra points one gets for travel or dining by using the Chase Sapphire Reserve card. Is this true, and if so can you shed any light on this?[/pullquote]

For more TPG news delivered each morning to your inbox, sign up for our daily newsletter.

Having not been on this specific phone call myself, I want to give the representative who Adham spoke to the benefit of the doubt. Normally I find Chase's front line customer service representatives to be very competent, knowledgeable, and overall good at their jobs. That being said, mistakes are occasionally made and it would appear that that's what happened here. Whether your rewards credit card is issued by Chase, Amex, Capital One, Citi or any of the other major issuers, you can rest assured that you will always earn bonus points on foreign transactions, provided the merchant is coded properly.

When awarding bonus points for things like travel or dining, credit card issuers rely on the Merchant Category Code (MCC) that each retailer uses. There are thousands of different codes that can identify a business as a hotel, a bar, an airline, or many other options. Card issuers look at the MCC associated with your transactions and award bonus points this way. This is also the root of the problem most times when points are awarded incorrectly. Sometimes a bar or restaurant inside a hotel will code as a hotel, meaning you wouldn't earn any bonus points if you swiped your American Express® Gold Card.

MCCs may not be used as thoroughly or as accurately in some foreign countries, so it never hurts to audit your statement whenever you get home from a trip abroad. For example, there are a few small restaurants on my block in Shanghai that take American credit cards, but I highly doubt these mom-and-pop food stalls have bothered to set up an MCC that Chase will be able to use. Still, if you're in a fancier establishment you have a good chance of getting your bonus points automatically without any extra work.

Related: The best credit cards for dining

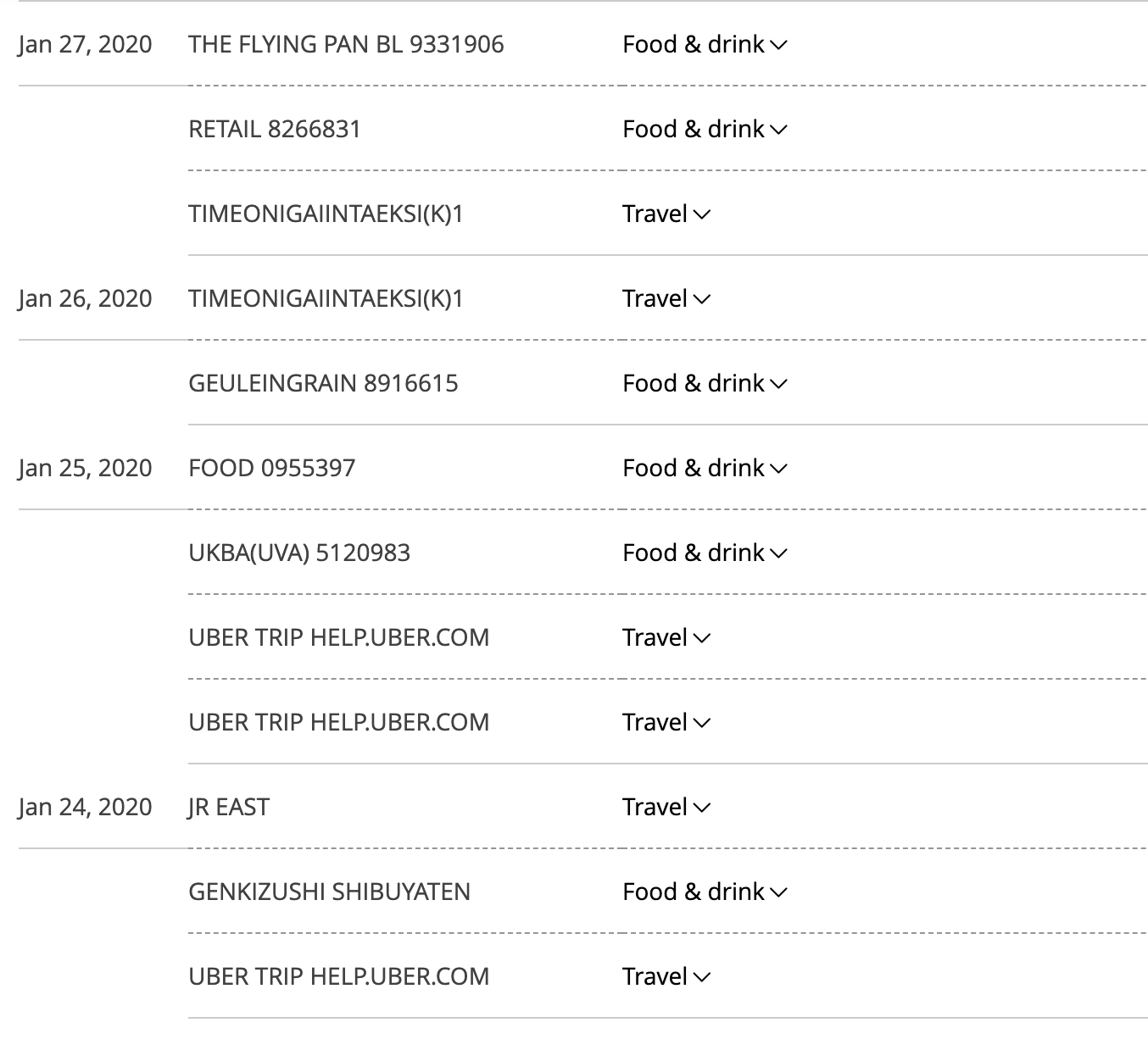

One of Chase's strongest selling points is how easy it is to work with the Ultimate Rewards program, from broadly-defined bonus categories to a travel credit with almost no restrictions on the Chase Sapphire Reserve. I spend about 85% of the year outside of the U.S., and I can count on one hand the number of transactions that have not coded correctly with my Sapphire Reserve. Just as an example, here's a screenshot of my statement from a recent trip to Japan and Seoul, showing all the purchases code correctly as either dining or travel:

Bottom line

The Chase Sapphire Reserve is one of the best cards to use both in the U.S. and abroad, and as long as you're shopping at a store that has set up its MCC code correctly, you'll earn bonus points without any problem. If for some reason you don't, you can always call in and Chase may be willing to make a manual adjustment.

Thanks for the question, Adham, and if you're a TPG reader who'd like us to answer a question of your own, tweet us @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.