Do I Earn Points if I Don't Pay My Credit Card Bill?

Update: Some offers mentioned below are no longer available. View the current offers here.

Reader Questions are answered twice a week by TPG Senior Points & Miles Contributor Ethan Steinberg.

With credit cards serving as the fastest way to earn points and miles these days, award travelers are caught in a game of tug and war between spending more to earn more points while still trying to stay financially responsible. TPG reader Kayla wants to know if she needs to pay her credit card bill in order to earn points...

[pullquote source="TPG READER KAYLA "]If I have a large balance on my credit card, I won't receive my points until I pay the balance in full, right?[/pullquote]

Before we address this question, it's important to reiterate that carrying a balance on your credit cards ignores one of the most important rules of travel rewards. The interest charges you'll pay from month to month will quickly erase the value of any points you're earning, especially since travel rewards cards tend to have higher interest rates. If you find yourself carrying a balance on your cards or are working on getting out of debt, it might be prudent to clean up your financial situation before you start pursuing travel rewards.

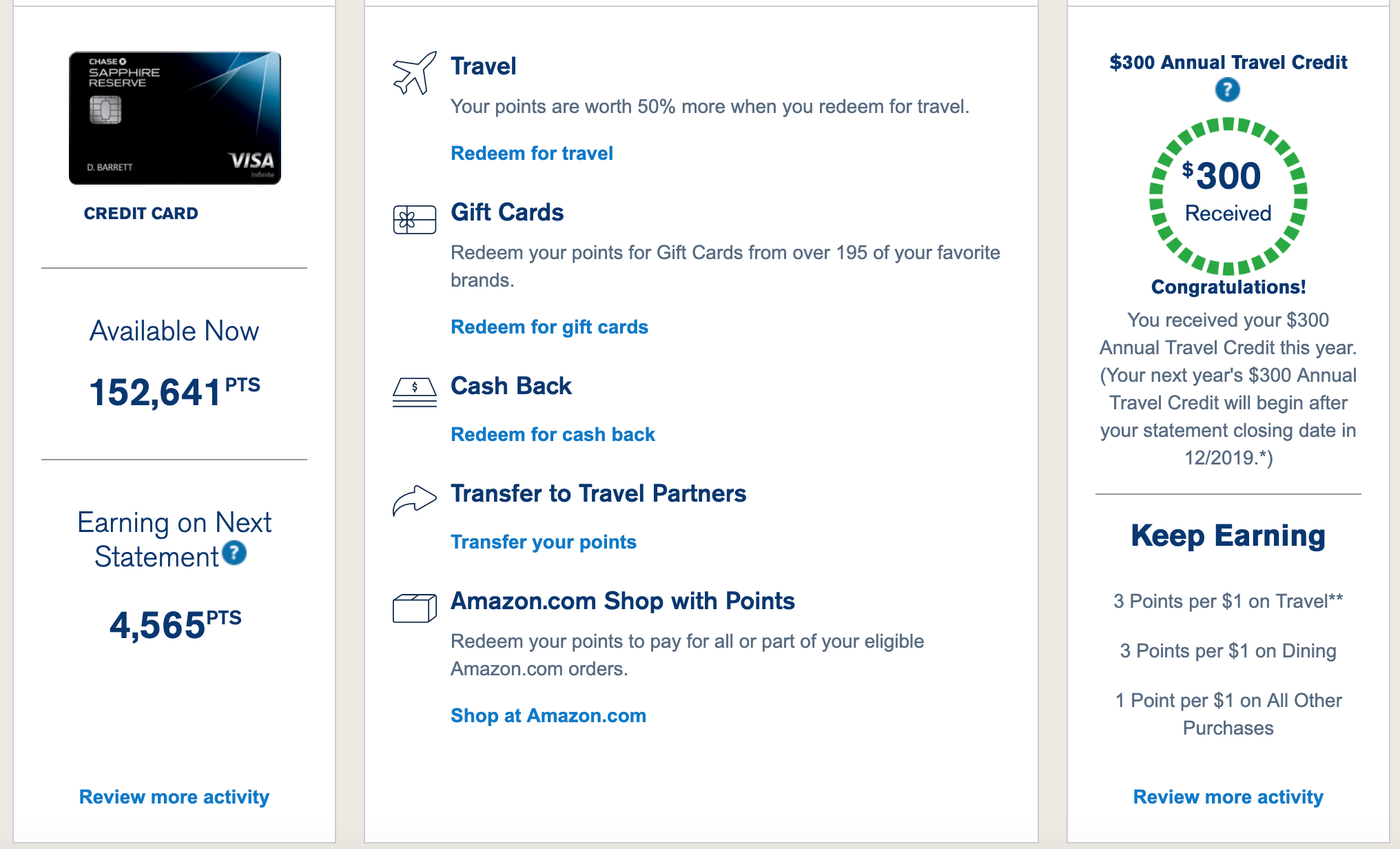

Now to get to Kayla's question. With a majority of credit cards, you earn your points based on the purchase and not when you pay your bill. If you look at my Chase Ultimate Rewards account for my Chase Sapphire Reserve, you'll see that I'm set to earn 4,565 points on my next statement. Chase will deposit these points into my account at the same time that my bill for this month becomes available, and I'll earn these points even if I haven't yet paid my bill.

This is how most credit cards operate, although there are a few exceptions to note. One that jumps to mind instantly is the Citi® Double Cash Card, which effectively offers 2% cash back on all purchases. You'll earn 1% at the time of purchase and another 1% when you pay your bill.

Another exception involves cards that earn American Express Membership Rewards points. Here's how this is described on the issuer's FAQ page:

When you earn Membership Rewards® points from spending with your Card, they initially appear on your billing statement as "pending." These are available for use a full monthly billing cycle after you pay the amount due on your billing statement, as long as your account remains current.

In essence, American Express delays the regular points you earn for a month, and you must pay the amount due before they're actually posted to your account.

Here's a snapshot from TPG Editor Nick Ewen's Amex account that shows this in action:

The 1,402 points designated as "Available on Payment" are from his statement that most recently closed. Once he makes his payment on that statement, the points will post to his account within 24-72 hours.

However, the 5,995 "Pending Points" will take a bit longer. Those correspond to purchases made since his last statement closed. Once that statement closes, they'll shift into the "Available on Payment" category and will then post when he submits a payment, and it's worth noting that even a minimum payment on an Amex account will result in the points posting.

When it comes to welcome bonuses, the terms typically state that it can take a month (or even three) for those points to post, but the terms typically don't require full payment to earn those bonuses. Again, though, not paying your balance in full and on time could result in interest charges that far outweigh the value of those points, so keep that in mind before you add a new travel rewards card to your wallet.

Bottom Line

Kayla should rest assured that the points she earns on her rewards cards will almost always be connected to the purchases she makes and not her payment activity, but that isn't a license to exercise poor financial judgement and start carrying a balance from month to month. There's a reason that "thou shalt pay thy balance in full" is the first commandment of travel rewards.

Thanks for the question, Kayla, and if you're a TPG reader who'd like us to answer a question of your own, tweet us at @thepointsguy, message us on Facebook or email us at info@thepointsguy.com.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.