Chase shut down my accounts after I applied for too many cards -- but there's a happy ending

Update: Some offers mentioned below are no longer available. View the current offers here.

This is a story about when greed is not so good.

Let me start by saying I'm a huge fan of Chase cards. I've been able to redeem Chase points for some of the most expensive hotels in the world, including the Park Hyatt Sydney and the Park Hyatt Tokyo.

New to The Points Guy? Sign up for our daily newsletter and check out our beginner's guide.

I've had the Chase Sapphire Preferred Card and the Chase IHG Club Rewards Select Mastercard (old version; no longer available) for years, and I love them both.

Last year, I closed my Chase World of Hyatt Credit Card and my Chase Marriott Rewards card (now the Marriott Bonvoy Boundless Credit Card) because I didn't want to pay annual fees (this was before I started at The Points Guy). In hindsight, this wasn't a great move on my part. I already miss the automatic status that comes with the Hyatt card and the free-night certificates from both cards.

Related reading: The Classic First Credit Card: Chase Sapphire Preferred

But after starting at The Points Guy, I also realized that I was just under Chase's 5/24 rule, and could now open a new Chase card for the first time in two years. On the advice of several TPG colleagues, my strategy was to first get the Chase Ink Business Preferred Credit Card, and then open a couple of personal cards if they'd let me.

Usually the Chase business cards don't count against your 5/24. But here's what happened when I tried to follow that advice.

Related reading: Chase's 5/24 rule: everything you need to know

Applying for new cards

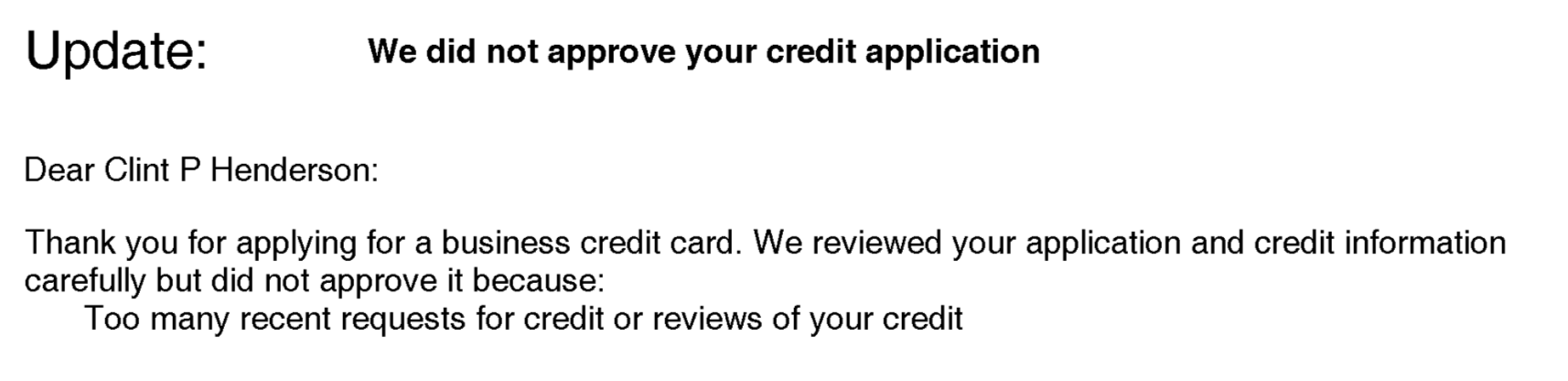

On Jan. 4 of this year, I applied for the Chase Ink Business Preferred card. I was excited about the 60,000 bonus points after you spend $4,000 on purchases in the first three months from account opening.

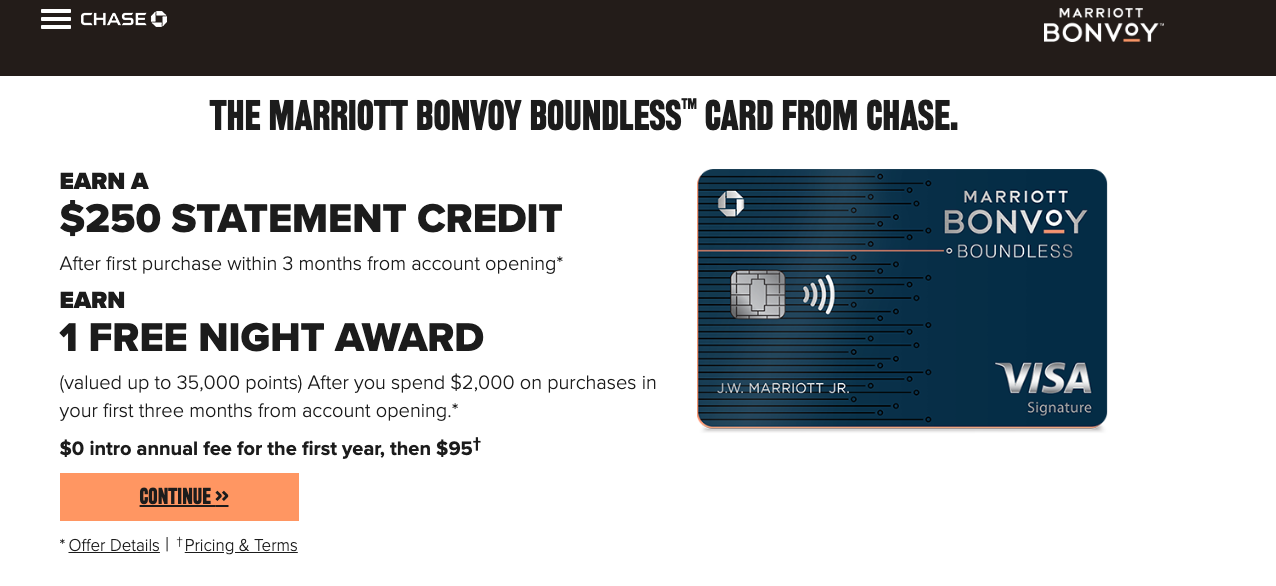

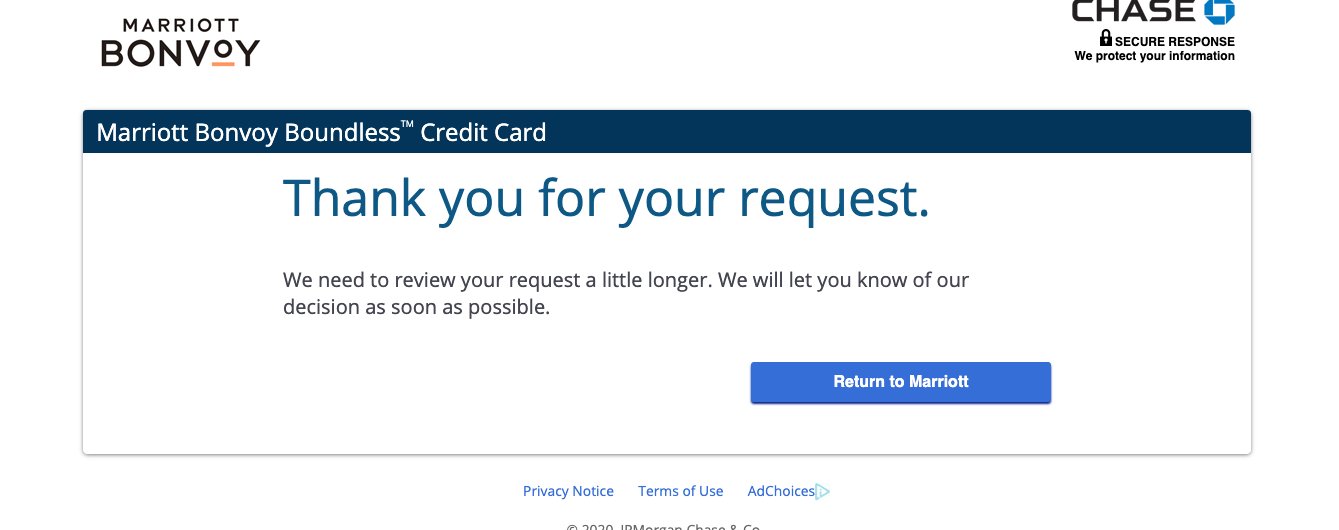

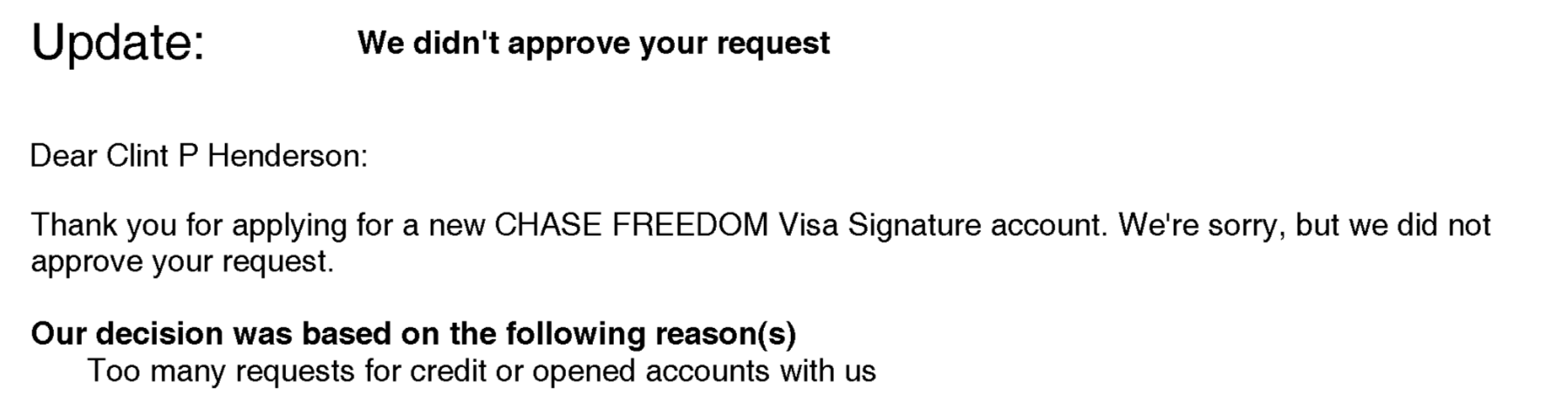

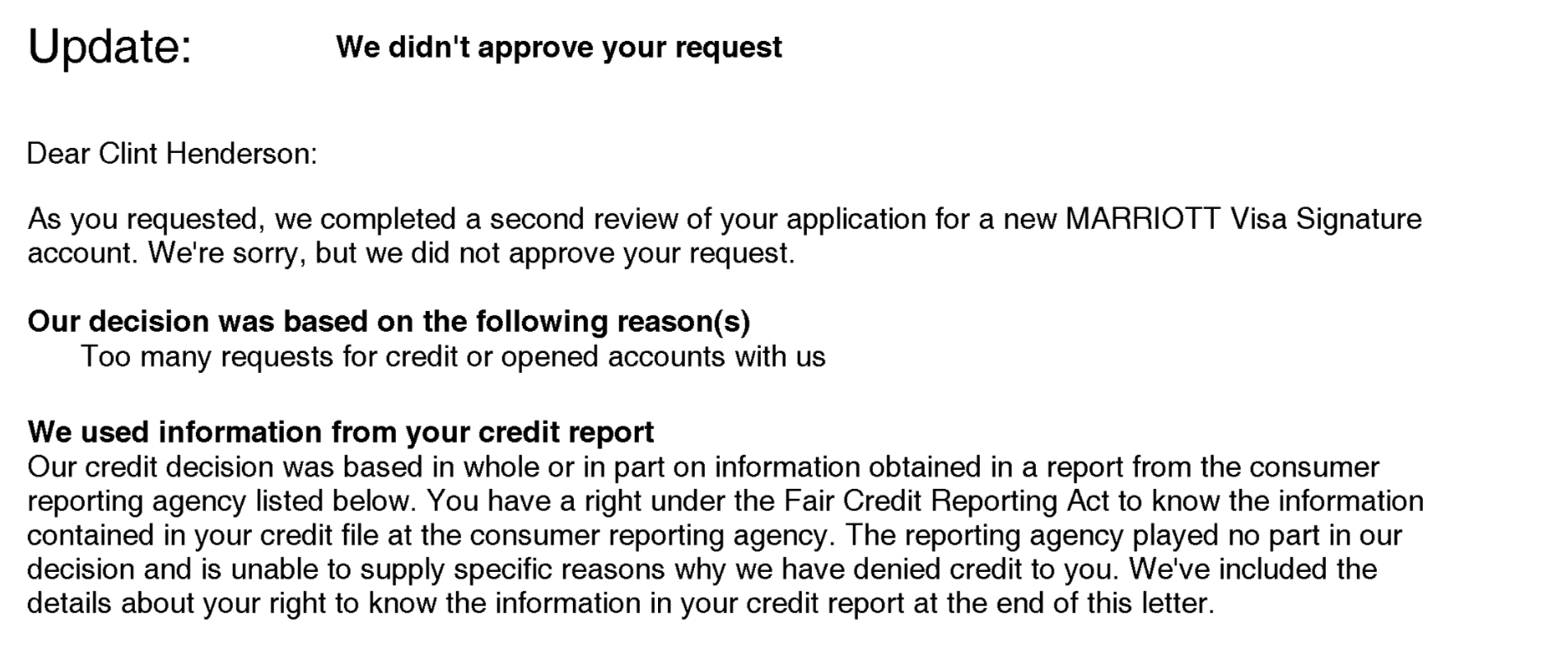

Unfortunately, I got the dreaded "pending" notice. I figured I'd be approved eventually, so I went ahead and also applied for the Chase Freedom card (No longer open to new applicants). This time, I got a blunt "can't approve at this time," message. I then thought I might as well press my luck and, soon after, I applied for the Marriott Bonvoy Boundless Credit Card via a hotel booking promotion.

The information for the Chase Freedom has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

This time, I got another form of that pending letter saying, "We need to review your request a little longer."

Denials and account shutdowns

At this point, I wasn't really that worried, figuring I'd get approved for at least one or two of the cards. I wasn't prepared for what happened next.

I called the following Monday, and, unusually, the agent wouldn't tell me the actual status of my applications -- only that they were pending. Not long after, I realized all my Chase credit card accounts had been shut down, and I was denied for all three cards.

Related reading: Don't let Chase's shutdown pattern bite you

I received letters on Jan. 13 in the mail that same week confirming that all my accounts had been shut down. I totally panicked. I worried most that I was about to lose my balance of about 99,000 Chase Ultimate Rewards points. I immediately transferred them to my World of Hyatt account. That points transfer was confirmed, but strangely, the points never made it into my Hyatt account.

Related reading: Redeeming Chase Ultimate Rewards for Maximum Value

I called for reconsideration on Jan. 14, and reached an agent who was surprisingly helpful. She told me it looked to her like it was because I had too many accounts, but said they would research the issue and get back to me.

I was sweating it out, but a company representative finally called me back on Jan. 17 to say Chase had reopened my old accounts. The company wouldn't tell me exactly why they'd been closed in the first place, but I suspect it was an over-active account supervisor. As you can imagine, I was very relieved. That said, I still was not approved for the cards I'd been applying for.

Related reading: The ultimate guide to credit card application restrictions

I saw later that I also had received an official denial for the Chase Ink on Jan. 9, which came as a notification in my Chase bank account.

On Jan. 17, I got a second denial for the new Marriott card.

What may have triggered all this is that I had called Chase on Jan. 3 to find out all the current cards I had with them -- as well as what my limits were and when they had expired (or were closed). In true TPG fashion, I was trying to put together a Google sheet tracking all my credit cards. (I think I'm up to about 25.) I may have triggered a red flag on my account with that call. The number of applications could also have triggered interest by the fraud department.

Related reading: How to maximize your Chase Ultimate Rewards points

Happy ending

In a huge surprise, after all of that drama, I was finally approved for the original Chase Ink card after I was initially denied. I only found out when I received the card in the mail. According to Chase, I had been approved on Jan. 28, more than a week after my old cards were reinstated.

It's such a strange result, but I'm happy with it -- and I already received my 60,000 Chase Ultimate Rewards sign-up bonus points.

Oh, and those 99,000 Chase Ultimate Rewards Points I had transferred to Hyatt? They never did show up in my Hyatt account, but they are safely back in my Chase account, so all is right in the universe.

Bottom line

Before you start applying for new credit cards (on top of the ones you already have), be aware of application restrictions. Know if you're ineligible before you apply, because if you get denied, you'll have a hard inquiry on your credit report worth nothing (except a temporary drop in your credit score).

Make sure you request reconsideration if you are denied, or get an explanation if it's a hard "no." If you're denied, don't reapply right away. You should wait at least three to six months before applying again (and make sure you're below the 5/24 rule in the case of Chase cards). Finally, consider applying for non-Chase cards if they also fit with how you want to use them. Learn more about what it means to be denied here.

Related reading: 5 ways to improve your credit score

Apply here for the Chase Sapphire Preferred Card with a 80,000 bonus points after you spend $4,000 on purchases in the first three months from account opening.