Chosen for an American Express financial review? Here’s what to expect

Editor's Note

While using credit card rewards for amazing travel deals is legal, certain behaviors can appear questionable.

Card issuers have instituted rules to limit credit card churning and attract valuable long-term customers instead (think: Chase's 5/24 rule). Much of the tension between award travelers and the big banks comes from suspicious credit card usage.

Each card issuer handles this differently. Take American Express, for example. If your credit card activity triggers a fraud alert, American Express may place your account under "financial review," which can be nerve-wracking.

Let's examine Amex's financial review process to better understand what it entails and how you can avoid it altogether.

This post is based on the firsthand experiences of several travel rewards experts who've all gone through Amex financial reviews. Given the sensitive nature of this topic, they asked to remain anonymous but provided us with documentation to verify their stories.

What triggers an American Express financial review?

While American Express doesn't publish the details of its fraud detection algorithm, one of the most common causes of a financial review appears to be a rapid ramp-up in spending. If you've been a cardmember for a few years, routinely spending $2,000 a month on your card, and suddenly, you begin to spend $15,000 to $20,000 a month, you might trigger a review.

Another common and easy-to-avoid cause is cycling your credit limit. Cycling refers to maxing out your available credit limit, paying off your card and repeating the process during a single billing statement.

One of the people I spoke to believes that his first review came from cycling on one of his Amex cards too often. The card had a $3,000 credit limit, and he was charging over $50,000 each month.

Sometimes, perfectly innocent behavior might lead to a flag of your account. A friend of mine, let's call him "Joe," made a $100 purchase using his American Express® Gold Card. The purchase appeared on his billing statement as a $100 balance owing.

After returning the item for a refund, his balance went to $0. The refund acted as his "payment" for the month. However, it tripped the fraud alert as his balance went from $100 to $0 without a direct payment. As we'll see later, this was a relatively simple case, and his financial review experience was not difficult.

Other interesting behaviors that have been reported to trigger financial reviews include having a payment bounce to one of your Amex cards and overusing the "check spending power" tool that Amex cards have.

Some Reddit users have reported receiving financial reviews from Amex after using the "check spending power" tool multiple times in a seven-day period.

Hundreds of people, myself included, spend large amounts on their Amex cards and never run into any problems. High spending doesn't guarantee a review, but specific acts can trigger it, such as rapidly increasing your spending and cycling your credit limit.

Related: The complete guide to American Express Membership Rewards

What is an American Express financial review?

For most people, the first indication that their account is under review is that it gets declined during a transaction. During the review, your charging privileges will be suspended, and you won't be able to use your Amex cards. (I have heard of people being given a $1,000 credit limit during the review.)

When you log in to the Amex app or website, a red triangle will appear, alerting you that charging has been suspended and directing you to call a number.

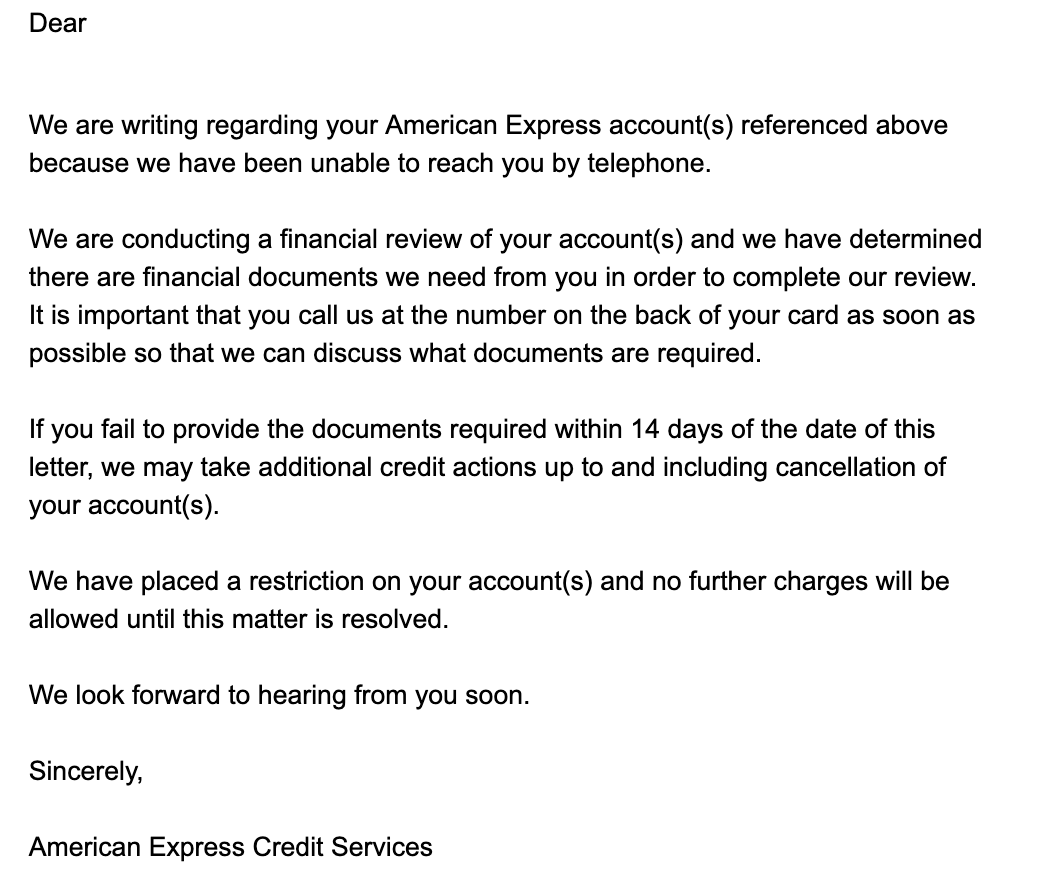

You'll also receive an email from Amex with additional information, confirming that your account is under review and advising that it may be closed if you fail to provide the documents Amex requests. Here is a screenshot of an email that one customer received.

As you can see above, "Joe" was given 14 days to contact Amex and provide all requested documentation. This is why you must address these types of requests promptly.

What is the process of an American Express financial review?

Cases vary based on individual circumstances, but generally, Amex will ask you to fill out Form 4506-T, which authorizes the issuer to access your IRS tax information.

I spoke with someone who survived four financial reviews (two each for him and his wife). He explained that Amex would use the adjusted gross income on your tax return to reevaluate your credit card application instead of the income you provide.

If you were honest about your income, as you always should be, this shouldn't create any problems. If you weren't forthcoming and your adjusted gross income is significantly lower than the income you listed on your application, Amex may reduce your credit limit or close some or all of your accounts.

In this way, he explained that the financial review process is more about income verification than anything else.

"Joe" had it a bit easier, likely because his case was more about a system error than anything he did. Amex asked him to provide bank statements for two different banks, including the one he uses to pay his credit cards. For those worried about privacy, this process is less invasive than giving Amex access to your full tax return.

Related: Who should (and shouldn't) get the American Express Platinum

Do I have to comply with an American Express financial review?

Your tax returns and bank statements are very personal documents, and you might not want them viewed by anyone for many reasons. Amex cannot compel you to produce documents during your financial review, but understand that you can expect your accounts to be closed if you don't comply.

Keep in mind that your Membership Rewards points will also be frozen during the financial review, meaning you can't transfer them to airline or hotel partners or redeem them through Amex Travel. That might be enough incentive to comply with Amex's requests, as account closure will lead to you forfeiting your points.

Bottom line

Sometimes, the appearance of impropriety is enough to get you in trouble, so it's important to understand some red flags that can trigger a financial review from Amex. You might not be able to avoid this if you have a business with spending levels that shift from one month to the next, but let this serve as a reminder to always be honest on your credit card applications.

If you experience a financial review, remain calm while responding quickly. Amex isn't looking to punish you for using your cards and travel rewards efficiently; they want to ensure you can afford to pay back the charges you're making.

Related: How to maximize points and miles when starting a business