Why the JetBlue Plus Card remains firmly in my wallet

Editor's Note

I currently have more than 20 different travel rewards credit cards. Some of these are great for everyday spending, while others offer valuable perks that can make my travel experience less costly or more comfortable — or both. Most carry annual fees, including some hefty ones. Every time one comes up for renewal, I crunch the numbers and make sure it's worth keeping the card for another year.

One card that has made the cut for several years now is the JetBlue Plus Card.

Here's why I continue to carry this card in my wallet — even though I only take a handful of JetBlue flights each year.

The information for the JetBlue Plus Card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Related: JetBlue Plus Card vs. JetBlue Premier Card: Should you go mid-tier or premium?

Why I first got the JetBlue Plus Card

Barclays first introduced three new JetBlue credit cards back in March 2016, and I quickly jumped on the opportunity to make my travels with the carrier even more rewarding.

I live in South Florida, about halfway between Orlando International Airport (MCO) and Fort Lauderdale-Hollywood International Airport (FLL), two airports with significant JetBlue operations. The carrier also flies to several cities out of Palm Beach International Airport (PBI), which is my closest departure gateway.

But JetBlue is appealing for a number of other reasons, too. I love the ability to pool points with my wife and daughter. Plus, the inflight experience for our frequent hops to the New York area is solid — including free Wi-Fi, unlimited snacks and complimentary DirecTV.

We also get to use the fantastic Sapphire Lounge at New York's LaGuardia Airport (LGA) whenever we fly home, thanks to my Chase Sapphire Reserve® (see rates and fees).

I even tried JetBlue Mint for the first time last year, and it was terrific. I'm still hoping to snag a good price on a Mint flight to Europe, as JetBlue now serves six destinations from the East Coast. And there's a lot more to come — including the airline's first-ever airport lounges and a new domestic first class.

Related: How JetBlue's 25 years of flying helped reshape US aviation

Why I'm keeping the JetBlue Plus Card

The $99 annual fee on my JetBlue Plus Card just posted, so I analyzed the previous year of card membership to see just how much value I got from the card. Ultimately, I wanted to see if the card should stay in my wallet.

And not surprisingly, the answer was a resounding yes.

While I personally don't utilize the perk of spending my way to Mosaic status, and I don't use the card for everyday purchases, there are many other benefits that carry tremendous value for me, namely:

- Points bonuses

- 10% of my redeemed points back

- Free checked bag on JetBlue fares

- 50% discount on inflight purchases

Let's break this down by each benefit to show you the total value I got from the card in the past year.

Bonuses

When you first open a new credit card, the welcome bonus should virtually always cover the card's annual fee (and then some). The JetBlue Plus Card is no exception, as new cardholders can earn 70,000 bonus points after spending $1,000 on purchases and paying the annual fee in full, both within the first 90 days.

Based on TPG's March 2025 valuations, this haul is worth an excellent $945.

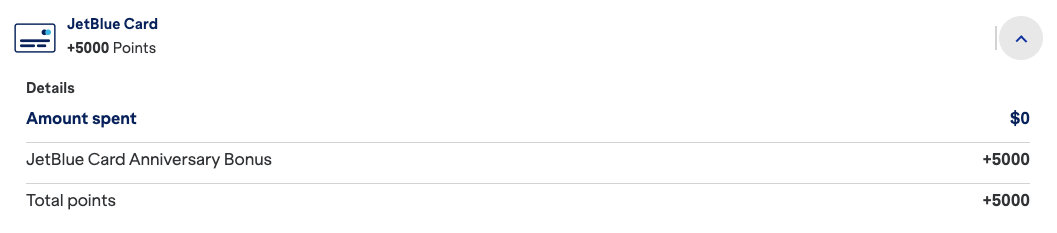

Of course, the welcome bonus only applies to the first year of card membership, and I am long past that point, so I won't include it in my calculations. However, there's another bonus awarded to cardholders in year two and beyond: 5,000 points on (or around) their anniversary date.

Again, using TPG's valuations, these points are worth around $68, so without ever setting foot on a JetBlue plane, you're already covering over two-thirds of the card's $99 annual fee.

Value: $68

10% of my redeemed points back

Another fantastic perk of the JetBlue Plus Card is that on every award ticket you book, you'll get 10% of those points back as a credit to your TrueBlue account. While the FAQ indicates that this will take four to six weeks, I typically see the rebate post to my account within a week of completing the trip.

Here's a list of how many points I got back during this past year of card membership:

- October 2024: 1,610 points on a flight from PBI-LGA for my wife

- December 2024: 1,780 points on a flight from LGA-PBI for me

If you do the math, I've kept 3,390 points in my account simply by carrying this card at the time of redemption, a savings of $46 (based on TPG's valuations).

What makes this benefit even better is that it doesn't matter who is actually flying; anytime points are redeemed out of the TrueBlue account of the primary cardholder, the bonus will apply. In addition, since I am also the primary TrueBlue member in a pooled family account, all of the points I spend (including those contributed by my wife and 10-year-old daughter) are eligible for this rebate.

Value: $46

Free checked bag on Blue fares

Last year, JetBlue updated its pricing for checked bags on domestic and short-haul international flights. Now, the first bag added at least 24 hours before departure during off-peak dates starts at $35. However, this can climb as high as $50 if you wait until check-in opens and travel on a peak date.

But not for those with the JetBlue Plus Card, as you and up to three companions on your reservation can get your first checked bag for free.

This really came in handy when traveling from New York's John F. Kennedy International Airport (JFK) in early April. We had a total of three checked bags as we were flying home from a 10-day vacation in the Philippines. I checked one, my wife checked one and my daughter checked one — for $0 out of pocket.

In addition, I also checked a bag on two flights I took by myself from New York back to Florida — one in October and another just last month.

With those trips, that was five checked bag fee waivers, saving us $175.

Value: $175

50% discount on inflight purchases

The fourth and final benefit that helps me justify keeping the JetBlue Plus Card is the 50% discount it offers on inflight purchases, including alcoholic drinks and EatUp snack boxes. This discount is applied automatically, generally on the day the charge posts to your card account. I used this perk twice over the last year:

- October 2024: One EatUp box ($5 savings)

- February 2025: Two cans of wine ($11 savings)

Value: $16

Total value from the JetBlue Plus Card

So given this activity, here are the totals for my past year of card membership:

- Anniversary points bonus: $68

- 10% points back: $46

- Checked bag: $175

- Inflight discounts: $16

When you add these together, I've enjoyed $305 of value in this past year alone simply by carrying the card in my wallet. When you consider that the annual fee is just $99, it's clear that I'm getting my money's worth.

Related: The complete guide to credit card annual fees

Is the JetBlue Plus Card right for you?

While the numbers make the card a no-brainer for me, it's important to note that this analysis may not be as simple for others.

For starters, I have many options for flying on JetBlue, with dozens of nonstop destinations from three different airports within 90 minutes of my house. Readers in New York, Boston, Orlando and Fort Lauderdale have a comparably extensive route map.

However, many other airports have much more limited service, including the following hubs of other major carriers:

- Hartsfield-Jackson Atlanta International Airport (ATL): Two nonstop destinations

- Charlotte Douglas International Airport (CLT): Zero nonstop destinations

- Chicago's O'Hare International Airport (ORD): Two nonstop destinations

- Dallas Fort Worth International Airport (DFW): One nonstop destination

- Denver International Airport (DEN): Two nonstop destinations

The card may not present such a strong value proposition if you live near any of these airports.

Finally, be sure to consider whether the other perks deliver actual value. If you only travel with a carry-on bag, you won't get much value out of the checked bag fee waiver. And if you never make inflight purchases, the 50% discount may also be irrelevant.

Bottom line

Every travel rewards credit card appeals to different profiles of travelers, and for me, the JetBlue Plus Card has offered tremendous value year in and year out. Based on my calculations, keeping the card in my wallet for the long run is worth my while — even though I'm only taking a few JetBlue flights each year.

While this card may not be the best one for you, hopefully this post has given you a framework to use as you evaluate whether to keep other cards beyond the first year.

Learn more: JetBlue Plus Card