Want to open a new Chase card? Here’s how to calculate your 5/24 standing

Update: Some offers mentioned below are no longer available. View the current offers here.

Unless you're new to opening credit cards, you're probably familiar with Chase's 5/24 rule. Put simply, the rule is this: if you've opened five or more personal credit cards across all issuers in the last 24 months, Chase almost certainly will deny your next card application.

Although some cobranded cards used to be exempt from the rule, it now applies to almost all Chase-issued cards — including business cards (though they won't add to your personal card count if you already have them and are applying for a new personal credit card).

To avoid wasting your five Chase slots or applying for a Chase card only to be denied, you should keep track of your 5/24 standing. Doing so is very easy and doesn't require any complicated spreadsheets.

The fastest way to check your 5/24 status is by using Experian's website and mobile app.

How to calculate your 5/24 standing

You could use practically any free credit report monitoring service to calculate your standing. While you can do this manually by tediously checking each account, let's save those options for later. First, let's look at the fastest option.

Sort by date with Experian

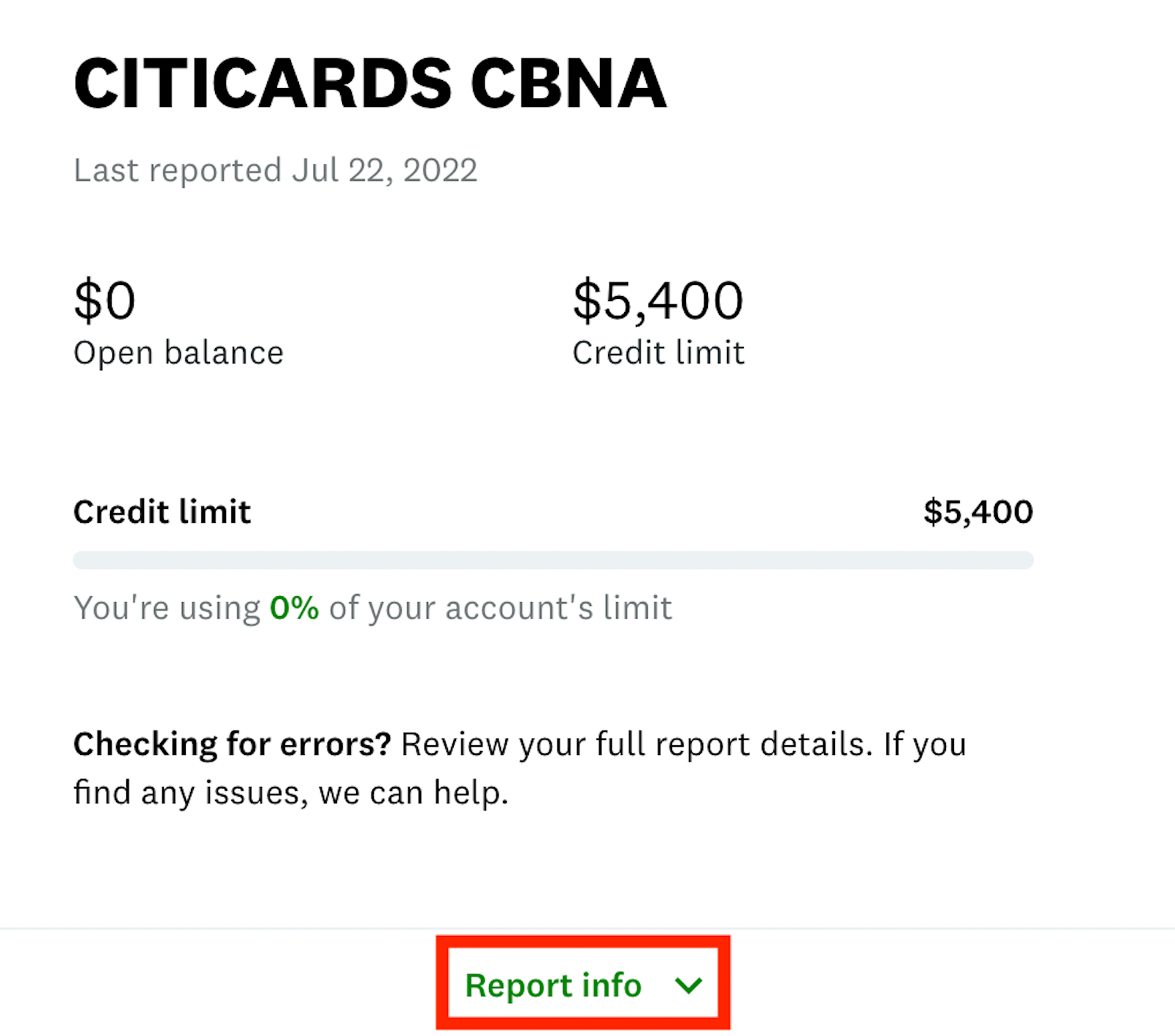

To start, sign up for a free account with Experian. Setting up your account is easy. You'll be asked for some personal information and must verify your identity through security questions.

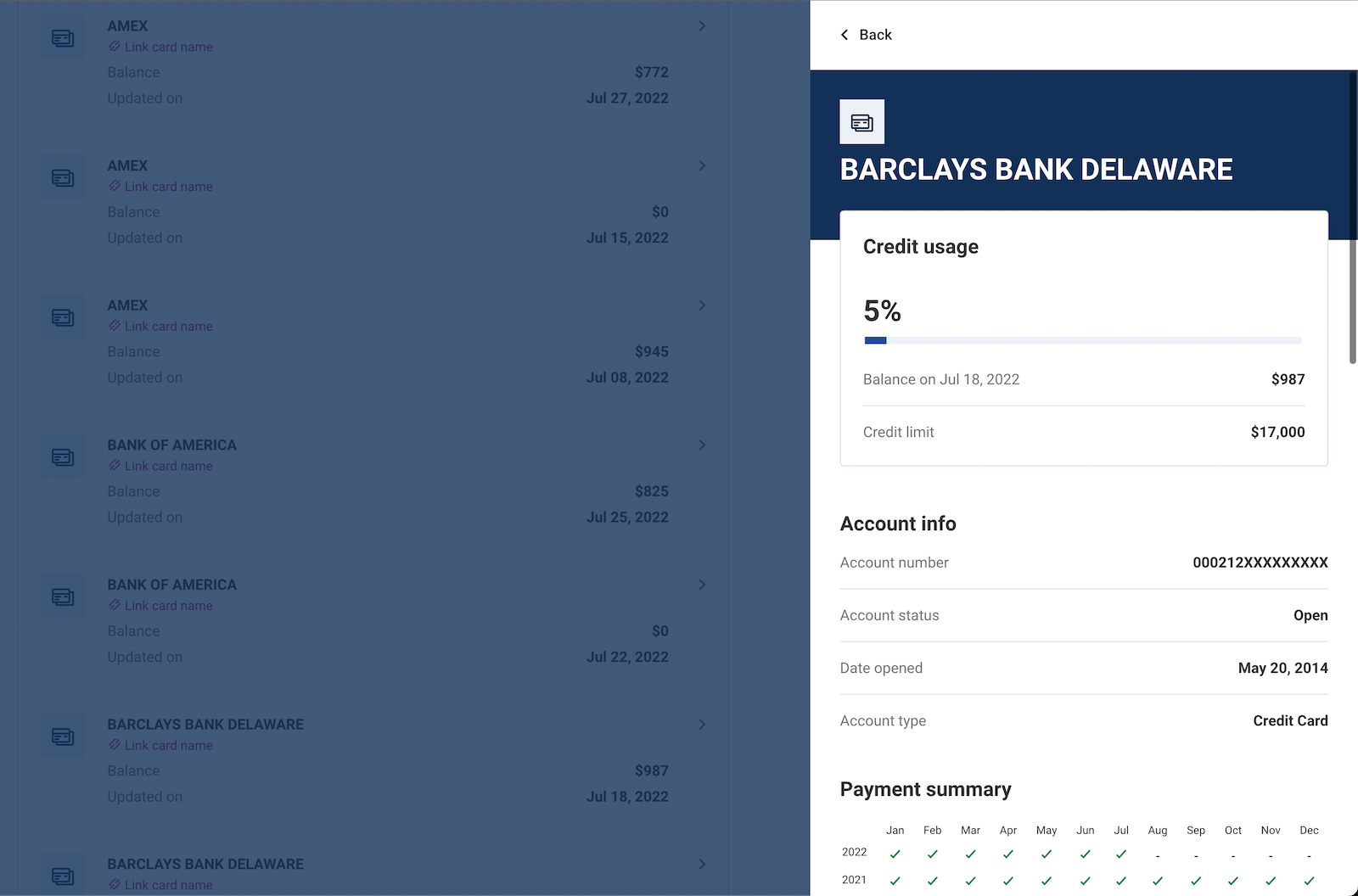

Once you're viewing your credit report, you can view a list of all your accounts — open and closed — sorted alphabetically by bank and credit card issuer on the desktop version of the website.

Unfortunately, you must click on each account individually to view the opening dates.

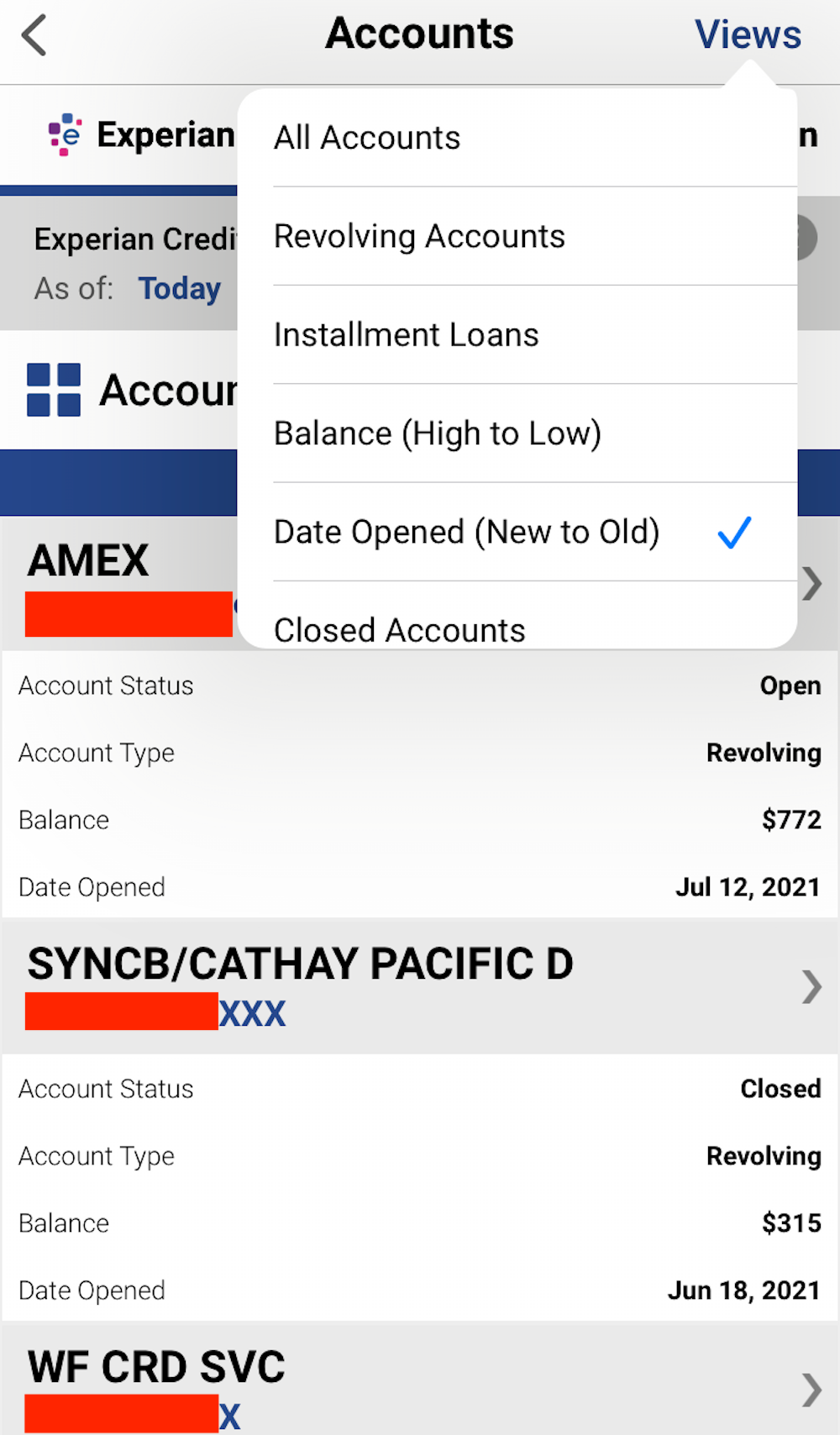

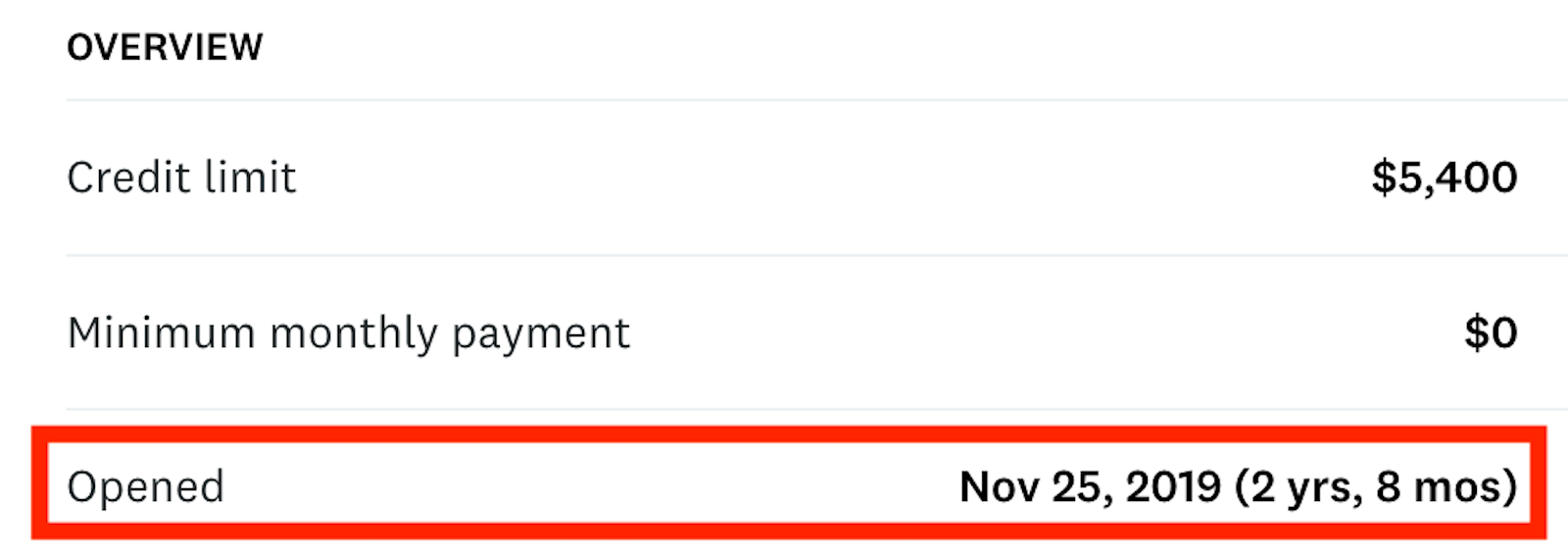

However, the mobile app can make this much easier. Within the app, go to your credit report, click on your accounts, and then select "Views" in the top right corner. From here, you can choose "Date Opened (New to Old)."

In this view, count everything that you opened within the past 24 months.

It's important to note that Chase only examines whether an account was opened. If you've closed an account that was opened in the last 24 months, it still counts toward your standing. Also, data points suggest that you will need to wait until the first day of the 25th month after your fifth account was opened to actually be below the 5/24 limit — that's an important technicality.

Chase's computer systems will add authorized-user cards from another person's personal credit or charge card to your 5/24 score, as they're reported on your credit report. However, if you're otherwise under 5/24, you can still apply for a Chase card and call the reconsideration line to ask that these accounts not be considered. Also, note that auto loans, student loans and mortgages show up on your credit report but do not count toward your 5/24 number.

Manual methods for checking your 5/24 number

Your free credit report from the three major agencies doesn't allow you to sort your accounts by the date they were opened. However, you can still establish your 5/24 status by obtaining a free credit report or by clicking on each account on Experian's desktop browser or other similar credit report trackers.

From here, you can see your account opening date.

What to do if you're under 5/24

Your first plan of action should be to apply for the Chase trifecta, which consists of theChase Sapphire Reserve®, Chase Freedom Unlimited® or Chase Freedom Flex® and Ink Business Preferred® Credit Card. Using these cards together will allow you to maximize the Ultimate Rewards program and help you make the most of your everyday purchases.

However, the card opportunities don't end there. There are several other Ultimate Rewards points-earning cards, as well as plenty of lucrative cobranded airline and hotel cards worth considering, such as the United℠ Explorer Card and the World of Hyatt Credit Card.

Related: The best ways to use your Chase 5/24 slots

What to do if you're over 5/24

Some points enthusiasts swear by Chase and refuse to apply for other cards when they're over 5/24. That could be a big mistake. The "opportunity cost" of waiting multiple months to apply for another credit card — in the hopes of picking up a single Chase card, though approval is not guaranteed — is far too high. Plus, it's always a good idea to diversify your earning strategy.

Your options for valuable cards outside of the Chase ecosystem are endless. For instance, American Express has its own trifecta of cards that can unlock a powerful combination of earning rates, welcome offers and perks — The Platinum Card® from American Express, the American Express® Gold Card and The Blue Business® Plus Credit Card from American Express. Then there are all of Amex's cobranded cards, such as the Marriott Bonvoy Brilliant® American Express® Card and the Delta SkyMiles® Platinum American Express Card.

And that's before you even consider all of the other issuers out there, such as Bank of America, Capital One and Citi.

Related: The best cards to get after you hit 5/24

Bottom line

To maximize Chase's credit card lineup, you must be wise about which cards you get and when you apply for them. Calculating your 5/24 standing is easy thanks to free credit report monitoring services like Experian. If you're over 5/24, don't make the mistake of overlooking cards from other issuers.

For more on Chase's 5/24 rule, see these related articles: