What credit score do you need to be approved for the Chase Sapphire Preferred Card?

Editor's Note

The Chase Sapphire Preferred® Card (see rates and fees) is one of the best travel rewards cards for beginners and experienced travelers alike. If you're thinking about applying, you're probably wondering whether your credit score is high enough.

While Chase doesn't publish a minimum credit score requirement, applicants with a FICO score of around 700 or higher generally have the strongest approval odds. However, your credit score is only one piece of the puzzle. Chase also considers your credit history, your income, your existing relationship with the bank and your application history.

Here's what you should know before applying.

What credit score do you need for the Chase Sapphire Preferred?

The Sapphire Preferred is widely considered one of the best travel rewards cards for beginners, making it a popular first travel card for many applicants.

Although Chase doesn't publish a minimum credit score requirement, we generally recommend having a FICO score of at least 700 before applying. That's in the middle of the "good" credit score range (670 to 739) and should give you solid approval odds.

Applicants with good-to-excellent credit typically have the best chance of approval, though no credit score guarantees you'll be approved.

Using the FICO scoring model, credit scores fall into the following ranges:

- Exceptional: 800 to 850

- Very good: 740 to 799

- Good: 670 to 739

- Fair: 580 to 669

- Poor: 579 and below

Keep in mind that it's possible to be approved with a score below 700 — or denied with a much higher one. Chase evaluates your overall credit profile, not just your credit score.

Related: How to check your credit score for free

What factors affect your approval odds?

Your credit score is only one part of your application. Chase also considers several other factors when deciding whether to approve you.

Credit history

Although the Sapphire Preferred is an excellent starter travel card, applicants with very limited credit history may have a harder time qualifying. If you're brand-new to credit or have only one credit card, consider building your credit history with a starter card before applying.

Income

Chase doesn't disclose a minimum income requirement, but your income helps determine your ability to repay borrowed money. Higher income can strengthen your application, particularly when paired with responsible credit management.

Credit utilization

Credit utilization — the percentage of your available credit you're using — is another important factor.

While Chase doesn't publish a target utilization ratio, keeping your balances low (generally below 20%) demonstrates responsible credit use and can improve your approval odds.

Existing relationship with Chase

Having an existing banking relationship with Chase may also help. While it's not a formal application requirement, longtime Chase customers — especially those with checking, savings or investment accounts — may have stronger approval odds than new customers.

Related: 8 ways to maximize your chances of being approved for a credit card

Should you apply for the Sapphire Preferred before the Sapphire Reserve?

If you're considering the Chase Sapphire Reserve® (see rates and fees), it often makes sense to start with the Sapphire Preferred. Approval is generally easier, and you can always upgrade to the Sapphire Reserve later if you decide its premium benefits better fit your travel style.

Related: Chase Sapphire Preferred vs. Sapphire Reserve: Which is better for you?

How to check your credit score

Under no circumstances should you pay to check your credit score. Many credit cards come with a free FICO score calculator. And even if yours doesn't, there are many other ways to check your credit score for free.

Many free sites can help you keep better track of your score and its factors. You can even use these services to dispute any information on your score that isn't accurate or appears to be fraudulent. If you want even more credit services, you may also consider paying for a credit-monitoring service like myFICO.

Related: Credit cards 101: The beginners guide

Factors that affect your credit score

Before you start applying for any credit cards, it's essential to understand the factors that make up your credit score. After all, the mere act of applying for a new line of credit will change your score.

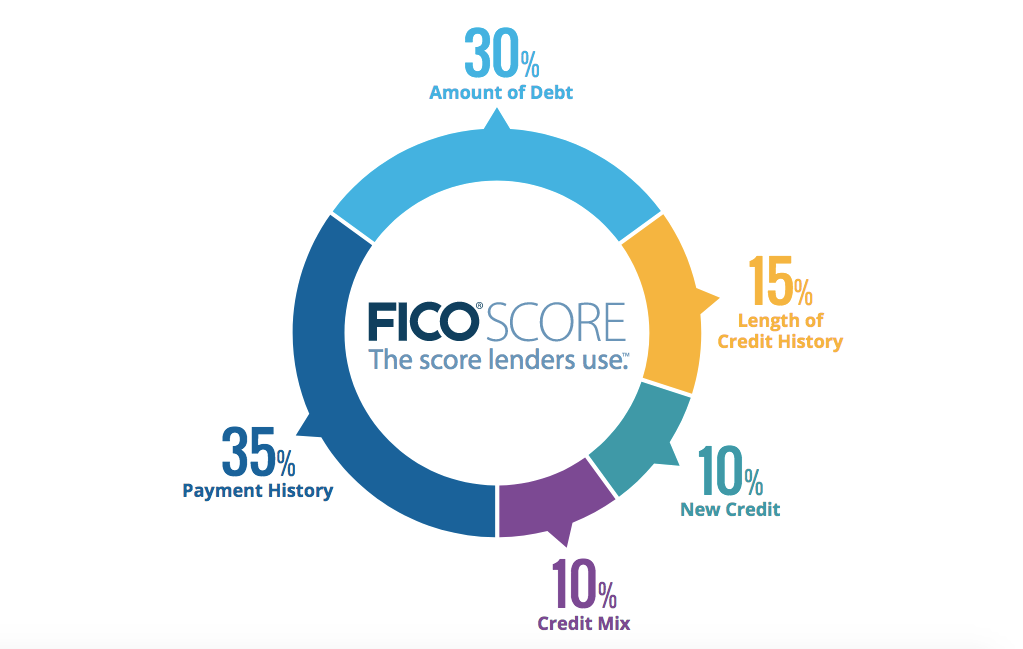

While the exact formula for calculating your credit score isn't public, FICO is transparent about the factors they assess and the weightings they use:

- Payment history: 35% of your FICO score is based on your payment history. So, if you get behind in making loan payments, this part of your credit score will suffer. Also, the more extended and more recent the delinquency, the more significant the negative effect.

- Amounts owed (credit utilization): 30% of your FICO score consists of the relative size of your current debt. In particular, your debt-to-credit ratio is the total of your debts divided by the total available credit across all your accounts. Many people claim that having a debt-to-credit ratio below 20% is best, but it's not a magic number.

- Length of credit history: 15% of your score represents the average length of all accounts on your credit history. The average length of your accounts can be a significant factor if you have a limited credit history. It can also be a factor for people who open and close accounts quickly.

- New credit: Your most recent accounts determine 10% of your credit score. So, this part of your credit score will suffer if you've recently opened too many accounts. After all, obtaining a lot of new credit is one sign of financial distress.

- Credit mix: 10% of your score is related to how many different credit accounts you have, such as mortgages, car loans, credit loans and store credit cards. While having a mix of loan types is better than having just one type, we don't recommend taking out unnecessary loans solely to boost your credit score.

With regard to the Sapphire Preferred, one crucial factor to consider is the average age of your accounts. While a lengthier credit history will boost your score, many issuers focus on the one-year cutoff. That means that having an average age of accounts of more than a year can go a long way toward increasing your odds of approval. However, you might have trouble getting approved with 11 months of credit history — even if your numerical credit score is excellent.

If you have any delinquencies or bankruptcies on your credit report, Chase might hesitate to approve you for a new line of credit. It's important to remember that your credit profile is more than just a number. Your credit profile is a collection of information given to the issuer to analyze your creditworthiness.

As a result, there is no hard-and-fast rule about a specific credit score that will automatically get you approved (or denied) for the Sapphire Preferred.

Related: 7 things to understand about credit before applying for a new card

Chase Sapphire Preferred application requirements

After you've checked your credit score, there is another Chase-related factor to consider before you apply for the Sapphire Preferred.

5/24 rule

As with most Chase cards, the Sapphire Preferred is subject to Chase's 5/24 rule, which states that Chase will automatically reject your application if you've opened five or more personal credit cards (with any issuer) in the last 24 months.

The 5/24 rule is hard-coded into Chase's system, so agents generally can't manually override it. As such, if you're over 5/24, your only option for getting the Sapphire Preferred is to wait until you're under 5/24 again.

Related: Want to open a new Chase card? Here's how to calculate your 5/24 standing

What to do if your application is rejected

If Chase rejects your credit card application, don't give up. If you receive a rejection letter, you should first examine the reasons for your rejection. By law, card issuers must send you a written or electronic communication explaining what factors prevented you from being approved.

Once you've figured out why Chase rejected you, you can call the reconsideration line.

Tell the person on the phone that you recently applied for a Chase credit card, were surprised to see that Chase rejected your application and would like to speak to someone about getting that decision reconsidered.

From there, it's up to you to build a case and convince the agent why Chase should approve you for the card.

For example, if Chase rejected you for having a short credit history, you can point to your stellar record of on-time payments. Or, if Chase rejected you for missed payments, you could explain that those were a long time ago and your recent history has been perfect.

Chase is also known to limit a customer's total credit line across all cards. You may have success overcoming a rejection by offering to shift unused credit from an existing card to a new one.

There's no guarantee that your call will work, but it's worth spending 15 minutes on the phone if it might help you get the card you want.

Related: Your guide to calling a credit card reconsideration line

Bottom line

While Chase doesn't publish a minimum credit score for the Sapphire Preferred, a FICO score of at least 700 generally gives you the best chance of approval.

Just remember that your score is only one factor. Your credit history, your income, your credit utilization ratio and whether you're under Chase's 5/24 rule can all have a significant impact on your application.

If your credit profile is in good shape, the Sapphire Preferred remains one of the best travel rewards cards for beginners and frequent travelers.

Apply here: Chase Sapphire Preferred Card