Are your credit card rewards taxable? Here’s why you’re receiving 1099s

Editor's Note

With tax season on the horizon, credit card enthusiasts may wonder if they have to pay taxes on the rewards they earned in 2025.

The good news? Generally, credit card rewards are not considered taxable income. However, certain types of rewards, such as checking account bonuses and credit card referral bonuses, may prompt your bank to send you a 1099.

Let's break down when you should expect a 1099 for your rewards, along with the steps you should take if you believe you received one in error.

Are credit card rewards taxable?

Most of the time, credit card rewards are not taxable.

This is because you must spend money to earn rewards in most credit card reward programs. To earn a welcome bonus, you'll have to meet a spending requirement. You receive points and miles in exchange for making purchases with your card.

So, generally speaking, rewards you earn from everyday card spending and credit card perks (such as statement credits) aren't considered taxable income. Instead, they're often considered rebates on your regular spending.

However, there is an exception. Bonuses received without spending (think: referral bonuses and automatic bonuses for opening a new bank account) are considered taxable income. This is because you don't have to spend on the card to earn rewards.

If you earned a chunk of points or miles from multiple referral bonuses or opened up a bank account with a welcome bonus just for signing up, you may receive a 1099 this year.

Related: Can you pay taxes with a credit card?

Which credit card rewards are taxable?

As mentioned, most rewards you earn from credit cards are not taxable. The one exception here is a referral bonus you receive when someone applies for a credit card through your referral link.

The bonus is considered income since you don't have to spend to get these rewards. It's worth noting, however, that the person you referred to won't need to pay taxes on the bonus they earn for completing a spending requirement.

Is cash back taxable?

In most cases, no. A 2010 IRS memorandum states that cash back earned from credit card spending is not taxable income.

However, if you receive it as part of opening a bank account where you didn't have to complete a minimum spending requirement, this is considered taxable income, and you must report it on your tax return.

Related: Best cash-back credit cards

Are business credit card rewards taxable?

Just like with personal cards, welcome bonuses and the rewards you earn from making purchases on your business credit card are not considered taxable income.

However, when claiming business expenses, you can only claim the net cost of an item after any statement credits you receive as a credit card perk, rather than the full cost before the credits are applied.

Related: Best business credit cards

Are bank account welcome bonuses taxable?

Yes. Bonuses for opening new bank accounts are under the same umbrella as credit card referral bonuses since you don't have to spend to earn them. This means they're taxable, according to the IRS.

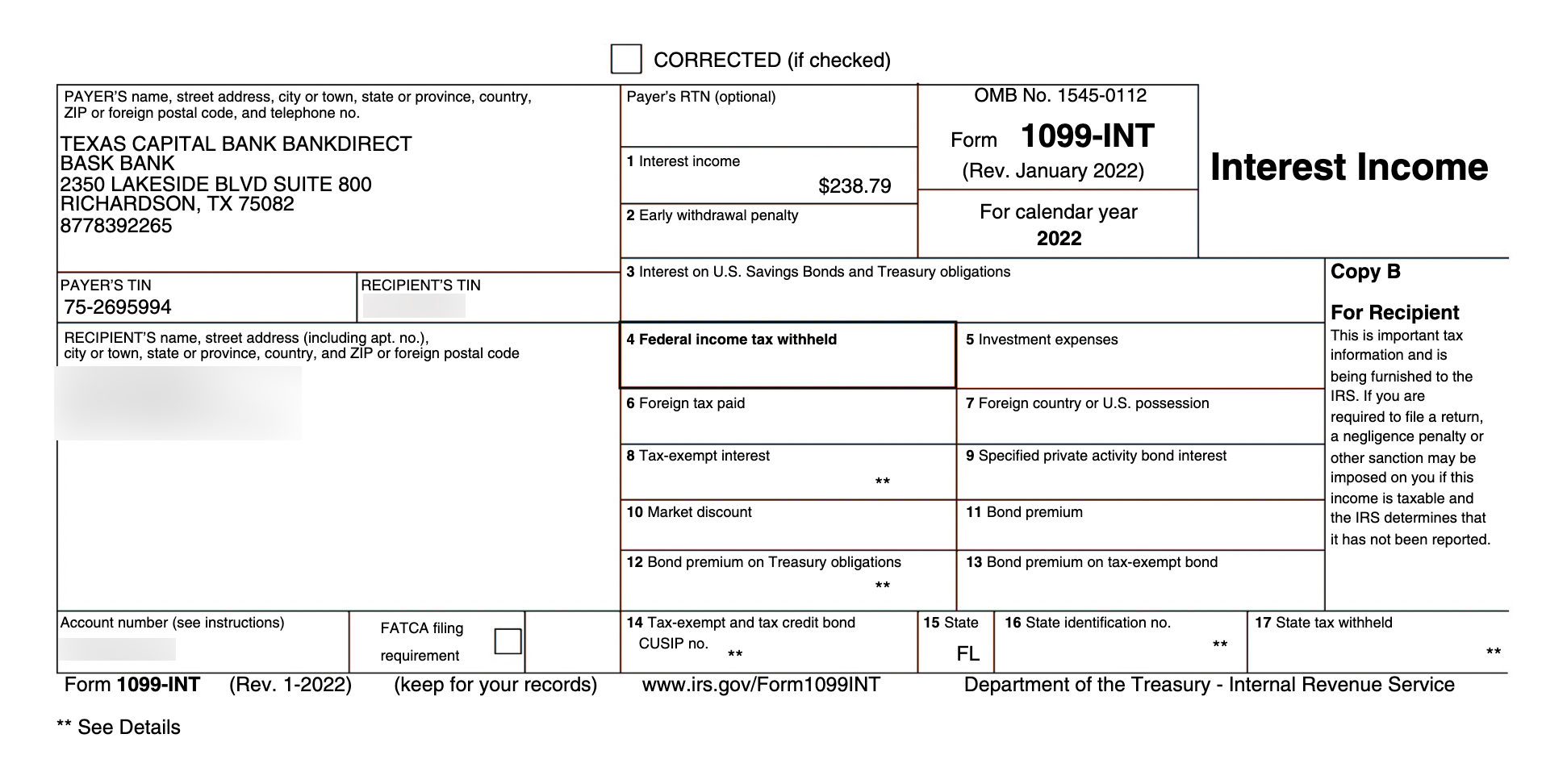

TPG senior editor Lyndsey Matthews received two 1099 forms from checking account bonuses after signing up with SoFi and American Express in 2025. The bonuses were included with interest earned on those accounts last year — both of which are considered taxable income.

Just like with credit card referral bonuses, there's no guarantee you'll get a 1099 for these bonuses, but you're expected to claim them as income regardless.

Will I receive a 1099 for my credit card rewards?

Sometimes, you'll receive a 1099-MISC or a 1099-INT if you have received taxable rewards.

A 1099 is often called an information return document for the IRS that shows the income you've received from a third party.

Not all issuers will send these forms. It's recommended that you maintain your own records since you'll still need to report all your income, even if you don't receive a 1099.

Related: If I cash out my points and miles, do I have to claim it on my taxes?

Which issuers send 1099 forms for credit card rewards?

If you earn $600 or more from referral bonuses, you should expect to receive a 1099 form from most major issuers. If you're expecting a 1099 and it doesn't come, you can request one or estimate the income.

It's important to note that you must report this income to the IRS, even if the bank doesn't send you a 1099.

In other circumstances, you can contact the issuer for clarification or correction if you receive a 1099 that you believe was issued in error.

Historically, banks have treated statement credits and bonus points as rebates on spending, which the IRS does not view as taxable income. So far, we haven't seen banks issue 1099s for statement credits, but we'll keep an eye on it.

Where do I report my credit card rewards income on a 1099?

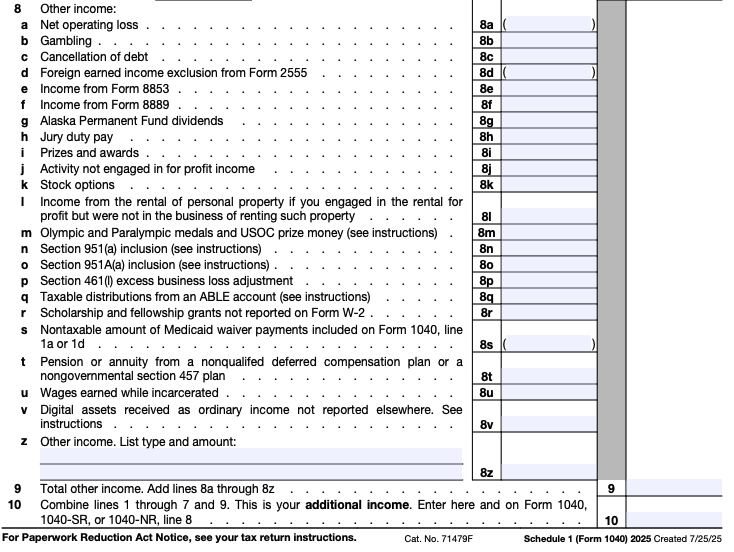

You should include the income under the heading "Other income" on line 8z of your 1040 as reported under the "Other income" from Schedule 1.

If you need to calculate referral bonus value, use the issuer's valuation of its points or miles or a third-party valuation.

For example, Capital One values its miles at 1 cent per point, while TPG's February 2026 valuations place them at 1.85 cents per point. When calculating the value of Capital One referrals, it's often in your best interest to use its 1-cent-per-point valuation.

Bottom line

Even if you've received thousands of dollars in value from credit card welcome bonuses and everyday spending, you generally won't have to pay taxes on these awards.

However, that is not the case if you've received bonus rewards from opening bank accounts or collecting multiple referral bonuses. You will have to pay taxes on these rewards.

Be sure to keep notes on your income sources. While many banks will issue 1099s for these earnings, some may not. However, you will still be expected to pay taxes on these earnings since they're considered income.

If you're concerned about owing taxes for your credit card rewards or have further questions, we recommend consulting a tax professional.

Related: Earn points, miles and cash back while doing your taxes

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.