A comparison of the top ‘buy now, pay later’ services — and what to watch out for

Editor's Note

Paying your credit card balances in full every month is one of the 10 credit commandments here at TPG — not just for maximizing your travel rewards but also for smart personal finance management.

However, there may be occasions when you need to make payments over time for larger purchases and don't want to pay high interest rates for the ability to do so. Enter "buy now, pay later," or BNPL, services.

A comparison of buy now, pay later services

Most BNPL services operate similarly. They do a soft credit check to qualify you and determine your spending limit, offer no interest fees and require you to make the first payment at the time of purchase. Typically, you'll have three remaining payments, due every two weeks. You can usually get instant approval at checkout, and some services offer a virtual card to add to your phone's digital wallet to pay in-store.

With many BNPL services available, it can be difficult to distinguish between all of them and decide which one to use. The notable differences between services include purchase limits, whether or not fees are charged for late payments and whether you can pay in monthly installments (but you'll often have to pay interest on this option).

We looked at Affirm, Afterpay, Klarna and PayPal, the top four services according to Statista. Since the original publish date of this article, Apple Pay Later launched; so we've added it as a fifth option in our comparison.

Affirm

- How it works: "Pay in 4" by making four payments (one every two weeks) or choosing a plan with monthly installments. You can pay anywhere, even in-store, using a one-time-use virtual card.

- Repayment methods: Bank account, debit card, credit card (but only for some purchases), check payments by mail.

- Purchase limit: Up to $20,000.

- Credit check: Soft. Payment history, including delinquent payments, may be reported to Experian.

- Interest: No interest for the Pay in 4 plan; 0%-36% for the monthly payments plan.

- Late fees: None.

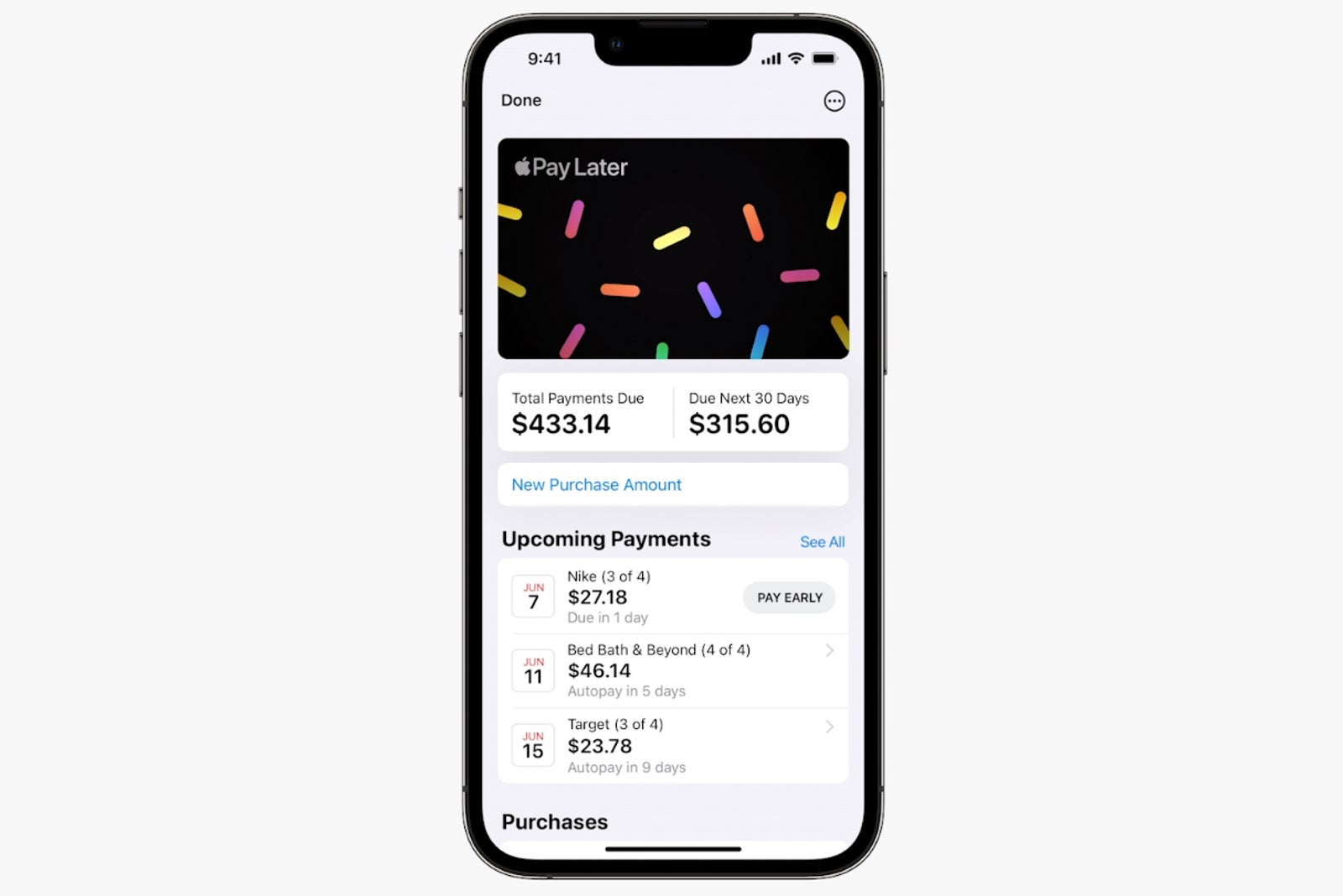

Apple Pay Later

- How it works: Make the first payment with the purchase, then three additional payments over six weeks.

- Repayment methods: Debit card.

- Purchase limit: Up to $1,000.

- Credit check: Soft; payment history may be reported to credit bureaus.

- Interest: None.

- Late fees: None.

Afterpay

- How it works: Choose payment plans of four interest-free payments (with the first due at purchase) or monthly installments of six or 12 months. In-store payments are available with select merchants, also.

- Repayment methods: Bank account, debit card, credit card. Monthly installments can only be paid by debit card.

- Purchase limit: Spending limits begin at around $500 and increase gradually over time.

- Credit check: Soft.

- Interest: None on the four-payment option; varies on monthly installments.

- Late fees: Capped at the lesser of 25% of the original order value or $68, regardless of the order amount.

Klarna

- How it works: "Pay in 4" with four interest-free payments, paid every two weeks. Additional options include a no-interest "Pay in 30 days" plan and a monthly plan with flexible financing. Shop online and pay with the Klarna app. To pay in-store, you can create a single-use card and add it to your phone's digital wallet. Klarna has a waitlist for its credit card currently.

- Repayment methods: Bank account, debit card, credit card.

- Purchase limit: No predefined spending limit. An automated approval decision is made with every purchase.

- Credit check: Soft for the Pay in 4 option. Hard for the monthly financing option.

- Interest: None on Pay in 4 or Pay in 30 days options; variable APR on monthly plans.

- Late fees: For the Pay in 4 option, up to $7 may be charged for late payments after 10 days (not to exceed 25% of the installment payment amount).

PayPal

- How it works: The "Pay in 4" option requires the first payment to complete the purchase, then three remaining payments (one every two weeks. Or go with the "Pay Monthly" plan, where the cost is broken into monthly payments over a 6- to 24-month period, with the first payment due one month after purchase.

- Repayment methods: Bank account, debit card, credit card (your PayPal balance can't be used for repayments, and credit cards can't be used for Pay Monthly).

- Purchase limit: $30-$1,500 for Pay in 4; $199-$10,000 for Pay Monthly.

- Credit check: Soft for Pay in 4; Pay Monthly does a soft check for prequalification and a hard inquiry when a customer accepts the loan and moves forward with financing options.

- Interest: None for Pay in 4; 9.99%-35.99% for Pay Monthly.

- Late fees: None.

Should you use buy now, pay later?

The simplicity of paying off a purchase in four payments and not paying any interest charges is appealing.

If you want to maximize your points and miles earning, BNPL is not ideal. Though many services allow you to link a credit card for repayment, you'll lose out on any category bonuses you may have received from shopping directly with the merchant.

In addition, using one form of debt to pay another form of debt isn't wise, especially if you're not able to pay off the charge on your credit card when the bill is due.

Additionally, C+R Research found that many people used BNPL services to buy items they otherwise couldn't afford. This creates debt, adds extra interest and can negatively affect your credit score.

Related: Apple's 'buy now, pay later' feature is rolling out: Here's how it works

Can I use my Chase card for buy now, pay later?

Chase credit cards cannot be used as a payment method for Buy Now, Pay Later services from Oct. 10, 2024. Debit cards and checking accounts can be linked.

Can I use my Capital One card for buy now, pay later?

If you decide to use a credit card for repayment, you won't be able to use any Capital One credit cards as the bank blocks its cards for buy now, pay later transactions. However, Capital One debit cards and checking accounts can be linked.

Related: Are consumers choosing 'buy now, pay later' options over credit card rewards?

Bottom line

For larger purchases that you'd like to pay off over time but still want to earn rewards on, consider credit cards with 0% introductory annual percentage rates and credit card services such as Chase's My Chase Plan (no enrollment required) and Amex's Pay It® Plan It® (no enrollment required). These offer installment plans with fixed monthly fees and no interest charges.

Whichever BNPL service or credit card offering you decide to use, responsible spending should always be top of mind.

Related: Alternative options for holiday purchase financing: My Chase Plan vs. Amex Pay It Plan It

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app