How to build credit when moving to the US

Update: Some offers mentioned below are no longer available. View the current offers here.

Many things are uniquely a part of the American experience. Much like cheeseburgers and college football, having access to credit is one of the most foundational aspects of living in the U.S.

If you're moving to the U.S., one of your top priorities should be to build your credit. That's because you'll likely need credit to apply for an apartment, mortgage or car loan and secure the lowest interest rates possible.

And eventually, if you're interested in opening a travel credit card to earn and redeem points and miles, you'll need to establish good credit to qualify for any of the top cards.

In this guide, we'll explain how to build credit when moving to the U.S., as well as delve into the fundamentals of credit and tell you how to ensure financial success. Plus, depending on what country you're from, you may be able to use your existing credit history after moving to the U.S.

Here's a closer look.

How credit works in the US

When you move to the U.S. — whether for school, work or other reasons — it can seem intimidating to start from ground level. Fortunately, there's a strategic approach to building credit, though it requires time and patience.

Credit involves a lender (typically a bank) and a borrower (you). When you apply and are approved for a line of credit, you borrow money from the lender for goods and services with a vow to pay them back — generally with interest.

As you start to finance big-ticket purchases that cost thousands of dollars, such as a new car or even a mortgage, you'll need access to credit to prove to lenders that you are reliable and financially able to repay your debt. And a higher credit score has two important implications:

- It can increase your likelihood of being approved for new lines of credit.

- When you're approved, you may enjoy lower interest rates.

Both of these happen because your positive financial history tells lenders they can trust you.

There are many ways to start building up your credit portfolio, but perhaps the most accessible path is by opening a credit card. When used correctly, credit cards can be incredible tools for financial success. You won't accrue interest if you pay your balance on time and in full, and doing so also builds your positive credit history — which demonstrates how you responsibly handle credit.

If you only use a debit card or cash to pay for everyday expenses, you lose the benefit of building up your credit since you aren't building those relationships with credit lenders.

However, credit cards are a huge financial responsibility that should not be taken lightly. It's crucial that you never charge more than you can afford to pay.

Related: Why Dave Ramsey is wrong about credit cards

What is a credit score?

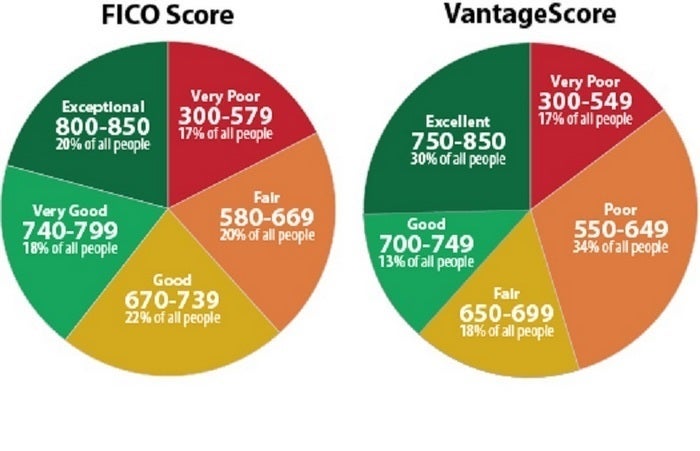

A credit score is a three-digit number (typically ranging from 300 to 850) and serves as a report card indicating your creditworthiness as a borrower. Lenders will send details about your credit behavior to three major consumer credit bureaus in the U.S.: Equifax, Experian and TransUnion.

There are two major credit scoring models: the FICO Score and the VantageScore. While the scoring methods are slightly different, scores greater than 700 are considered to be good in both models.

For instance, with FICO, these are the five factors that are taken into consideration to calculate your credit score:

- Payment history: 35%.

- Amounts owed: 30%.

- Length of credit history: 15%.

- New credit: 10%.

- Credit mix: 10%.

As you can see, the two most important factors are payment history and amounts owed — accounting for 65% of your total FICO score. Paying your balance on time and in full is critical if you want to increase your score. The other three factors — length of credit history, new credit and credit mix — are still important, though you have less control over these. However, those elements will naturally improve with usage over time.

Related: How your credit scores work

How to build credit in the US

Now that you understand the basics of credit, here's a step-by-step guide on hitting the ground running by opening your first credit card.

Review your credit card options

There's no shortage of credit card options on the market today. Besides the ability to build credit, you can potentially earn valuable points and miles through rewards credit cards that can be redeemed toward travel, cash back and more.

However, when you're first starting out in the world of credit cards — or credit in general — you likely won't qualify for premium cards like The Platinum Card® from American Express or the Chase Sapphire Reserve. These cards are much harder to gain approval for and will usually require good-to-excellent credit scores.

There are a few options that offer better approval odds for those who have a limited credit history. If you're a student, consider applying for a student credit card specifically designed for students without any credit history. There are many options, but Capital One has a preapproval tool that allows you to see which of its cards you're eligible for before filling out an official application. The issuer currently offers three student credit cards that enable cardholders to earn and redeem rewards — all for no annual fee.

- Journey Student Rewards from Capital One. (Product is no longer available).

- Capital One Savor Student Cash Rewards Credit Card.

- Capital One Quicksilver Student Cash Rewards Credit Card.

The information for the Journey Student Rewards card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

Another option is to apply for a secured credit card, which is best for those having difficulty getting approval for other credit cards. To open your account, a secured credit card requires you to put down a fully refundable security deposit that determines your initial credit limit.

For instance, if you put down $1,000, your credit limit on your secured card will be $1,000. Depending on your issuer, you may be transitioned into a "normal" credit card after making consistent on-time payments for a period of several months.

The OpenSky® Secured Visa® Credit Card is an ideal option since there's no credit check involved in the application process. You'll need to put down a minimum security deposit of $200, but you may be able to secure a credit limit of up to $3,000. Keep in mind that it has a $35 annual fee.

Understand the credit card application process

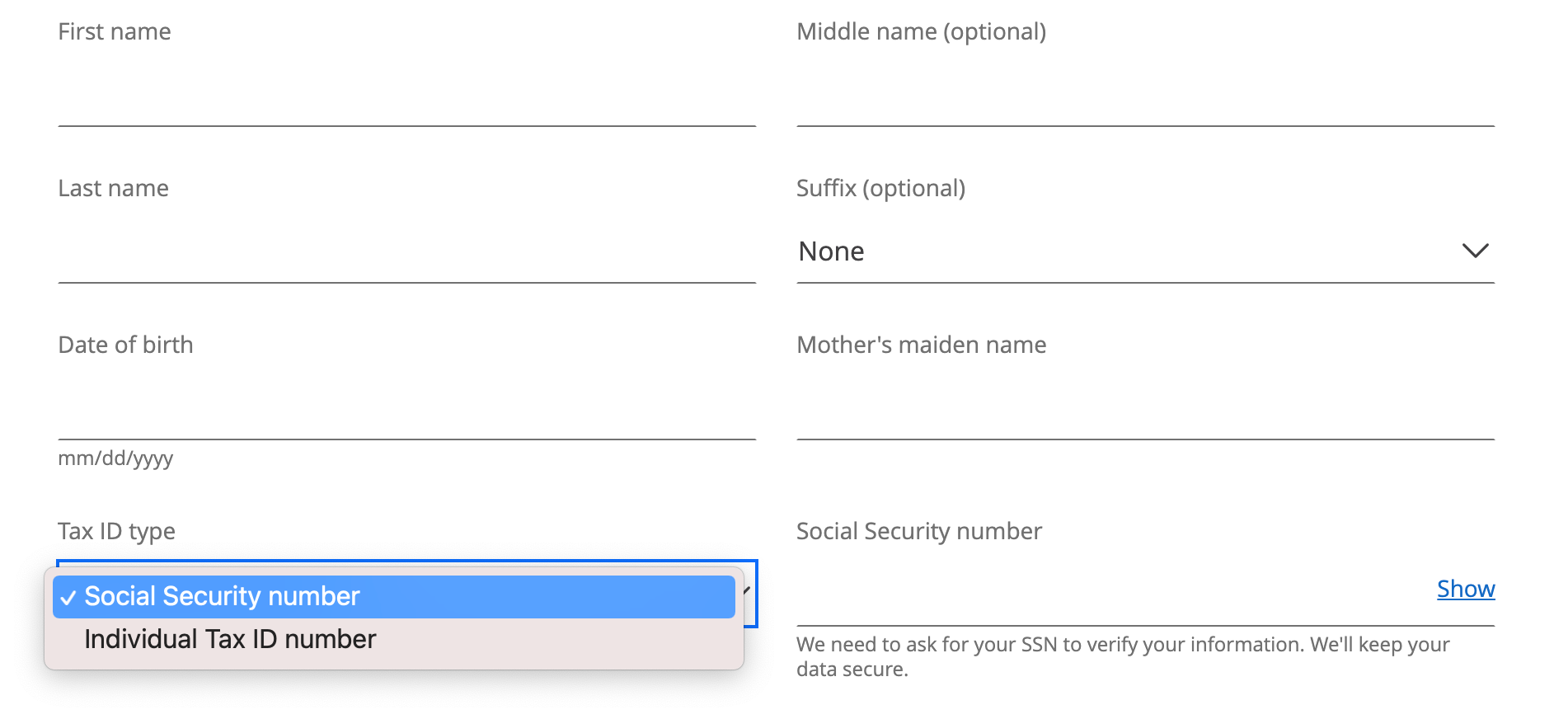

After choosing a credit card, you'll want to understand how the application process works. Generally, when applying for a credit card, you'll need to be at least 18 years old and have these:

- Social Security number.

- Checking or savings account.

- Source of income.

The biggest roadblock is likely the first requirement on this list: you may not have a Social Security number if you've just moved to the U.S. However, if you don't qualify for one, you may be able to get an individual taxpayer identification number, or ITIN, through the Internal Revenue Service instead and use that on your credit card application.

To obtain an ITIN, you'll need to mail your W-7 form, tax return, proof of identity and foreign status documents to the IRS. For further information on how to obtain an ITIN, click here.

See if you're eligible to transfer your international credit history to the US

You may be able to transfer your credit history from your home country to the U.S. with Nova Credit. This service is free for consumers, and here's how it's described:

Nova Credit has partnered with lenders and international credit bureaus to help newcomers apply for products and services using their foreign credit history. When you apply with Nova Credit, you generally have the option to add your international credit history to your application.

Credit history from the following countries can be used:

- Australia.

- Brazil.

- Canada.

- Dominican Republic.

- India.

- Kenya.

- Mexico.

- Nigeria.

- United Kingdom.

- South Korea (new as of February 2023).

- Switzerland (new as of February 2023).

If you're moving from any of the countries already on Nova Credit's list, you can use its services to transfer your international credit history so that you're not starting from zero in the U.S. — and you won't need a Social Security number or ITIN. On Nova Credit's website, you'll answer a few questions to determine your financial eligibility and get personalized credit card recommendations based on your financial history. If you're looking for a car, you can pre-qualify for an auto loan through Nova Credit based on your credit history.

Credit-building tips you need to know

Once you establish a line of credit, follow these credit-building tips to improve your score over time.

Always pay your bill on time and in full

If you miss a credit card payment, you'll likely be on the hook for a late fee. Plus, not paying your entire monthly credit card bill results in interest. Additionally, carrying a credit card balance can harm your credit score and cost more in fees/interest than the value of any credit card rewards you earned.

Related: The best way to pay your credit card bills

Check your credit score often

Set up a routine for monitoring your credit score. There are several ways to check your credit score for free. Otherwise, consider using resources like Credit Karma to check your Vantage 3.0 credit score for free.

Access your credit report

You're legally entitled to obtain a full credit report from the three major credit bureaus once a year for free. Visit annualcreditreport.com to obtain your full credit report to ensure that there are no mistakes.

Request a credit limit increase

As you become a trusted borrower and develop solid credit habits, you may be eligible for a credit limit increase through your issuer. You may be able to request a credit limit increase online or by calling customer service. It's important to gain a higher credit limit over time. This will reduce your credit utilization ratio, which is the relationship between your balances and your total available credit limit. The lower your credit utilization ratio, the better, since 30% of your FICO credit score is determined by the "amounts owed."

Read through TPG's 10 commandments for credit card rewards

Be sure to review TPG's 10 commandments for credit card rewards, a detailed guide on the best practices for using credit cards. You'll want to avoid common mistakes like paying foreign transaction fees or letting your rewards accidentally expire.

Related: English not your 1st language? Use these 8 tips to help your credit card rewards game

Bottom line

Here at TPG, we have dozens of free resources to help you understand the foundations of credit and improve your credit score over time. As a newcomer to the U.S., you can form positive credit habits now to ensure financial success later on.

Related reading: