American Express grace period: 'Please pay by' date isn't your payment due date

Update: Some offers mentioned below are no longer available. View the current offers here.

While banks and credit card issuers haven't always been the most consumer-friendly, things have generally improved for cardholders since the financial crisis of 2008. (An exception to that is recent events with some small- and mid-sized banks.)

Legislation, especially the Credit Card Accountability, Responsibility and Disclosure Act of 2009 (CARD Act), sets strict guidelines for how card issuers communicate with customers about everything from interest rates and benefit changes to payment due dates.

But as a consumer, you should still check the fine print. And if you have an American Express card, figuring out when to pay can be challenging.

American Express: When to pay

Let's look at a personal example: Right now, new The Business Platinum Card® from American Express cardmembers can find out their offer and see if they are eligible for as high as 300,000 bonus points after spending $20,000 on purchases in the first three months of card membership. Welcome offers vary, and you may not be eligible for an offer. This offer is worth up to $6,000 based on TPG's September 2025 valuations.

I applied for the card at the end of 2018. My bonus then wasn't quite as good as the current offer, but I had a $15,000 spending requirement (no longer available).

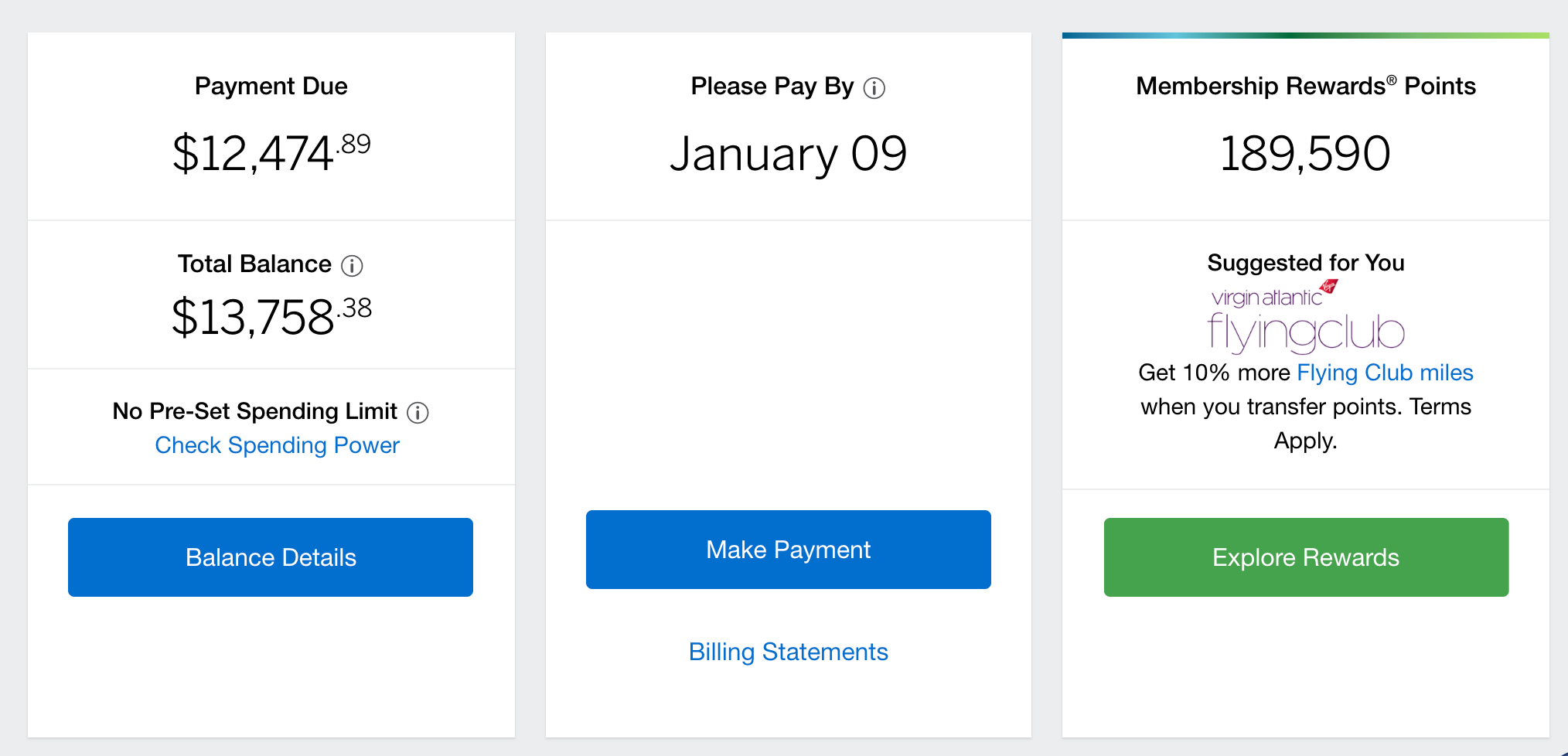

Spending $15,000 in three months is a lot, so after opening the card, I closely monitored my account activity. My first statement closed on Dec. 25, and I was a little alarmed to see that Amex was only giving me 15 days, until Jan. 9, to pay off my five-figure balance.

If you're a small-business owner with other tasks demanding your attention, you might've simply circled that date on your calendar and moved on. After all, paying your American Express balance by its due date is important.

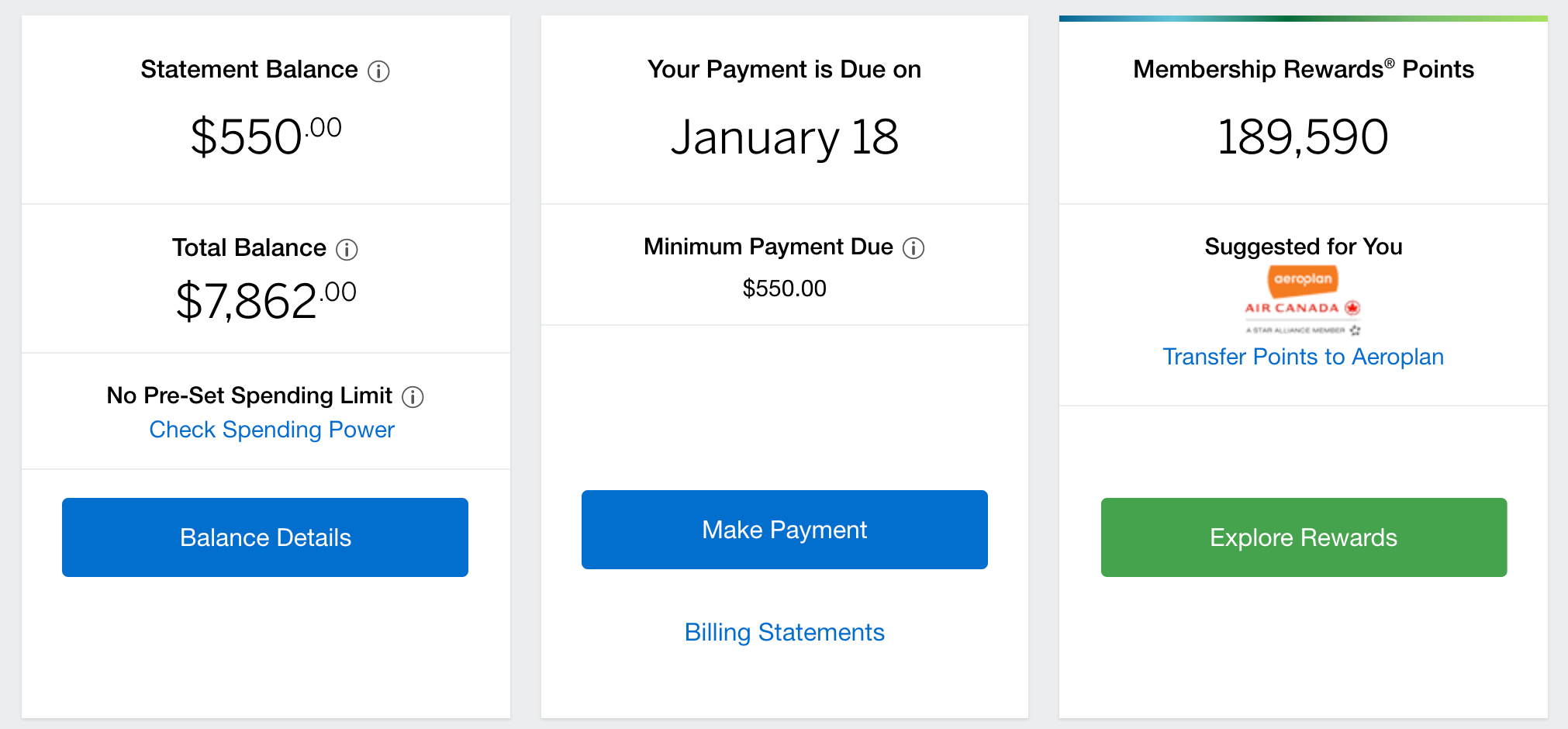

But something didn't seem right. By comparison, here's what my account page for my personal The Platinum Card® from American Express looked like at the same time:

While my personal Amex Platinum card clearly told me the date my payment was due, my Business Platinum card had Amex's suggested "Please Pay By" date.

After calling an Amex rep and digging a little deeper into my statement, I learned that I wouldn't actually be charged a late fee as long as I paid my bill in full by Jan. 19, more than two full weeks after the date Amex suggested I pay (see rates and fees).

It's important to be aware of this since if you think you need to pay your bills two weeks earlier than you have to (to avoid late fees), you may be redirecting funds that could otherwise be used on payroll, inventory and/or growing your business. This two-week squeeze could be especially frustrating for small businesses struggling to manage expenses.

Related: Amex Platinum vs. Amex Business Platinum

Confusing, much?

If you're wondering how it can possibly be legal for a bank to mislead its cardmembers about payment due dates, the answer is that it might not be. Subsection 201 of the CARD Act says the following about late payment disclosures:

"(A) LATE PAYMENT DEADLINE REQUIRED TO BE DISCLOSED.—In the case of a credit card account under an open end consumer credit plan under which a late fee or charge may be imposed due to the failure of the obligor to make payment on or before the due date for such payment, the periodic statement required under subsection (b) with respect to the account shall include, in a conspicuous location on the billing statement, the date on which the payment is due or, if different, the date on which a late payment fee will be charged, together with the amount of the fee or charge to be imposed if payment is made after that date."

The CARD Act references consumer credit plans, so it's unclear whether these same regulations would apply to the Amex Business Platinum. Either way, Amex's behavior is at odds with how Congress wants card issuers to treat their customers.

Nowhere on my five-page monthly statement is there any mention of what, if any, late fees I would owe on what date. The only acknowledgment of late fees is: "You may have to pay a late fee if your payment is not received by the Next Closing Date." Your statement may vary, so make sure to inspect it closely.

Amex has come under fire for its reporting of due dates before, settling and paying an $85 million fine in 2012 for labeling the "Please Pay By" date as the actual due date on the account.

Bottom line

It's easy to trust a company willing to analyze your spending to help you earn the most rewards. However, this is a reminder that you need to be your own advocate.

If you have a card from American Express, when to pay can be hard to figure out. It's worth double-checking the language around your payment due date to ensure you know when to pay your American Express balance. When in doubt, call the number on the back of your card and speak to a representative.

Related: Amex Business Platinum card review

For rates and fees of the Amex Business Platinum, click here.