6 things to weigh before canceling a discontinued credit card

Update: Some offers mentioned below are no longer available. View the current offers here.

Credit card issuers (along with their hotel and airline partners) launch new cards, rebrand and revamp existing cards and even discontinue card products all the time.

There are several reasons for this. In some cases, an airline or hotel group switches credit card partners. That's what happened a few years ago when Hilton Honors dropped Citibank to consolidate its line of cards with American Express. In another instance, when Marriott took over Starwood, it kept both American Express and Chase as credit card partners, and we have products like Chase's Marriott Bonvoy Boundless Credit Card and the Marriott Bonvoy Brilliant® American Express® Card to choose from. When shifts in the credit card market occur, some cards are "converted" into new products: the Starwood Preferred Guest® Business Credit Card from American Express turned into the Marriott Bonvoy Business® American Express® Card.

When credit cards are discontinued altogether, cardholder accounts are either closed automatically, or cardholders are issued entirely different products from the same bank. That's what happened when Chase phased out the Fairmont Visa and sent cardholders the new Chase Sapphire Preferred Cards. Interestingly, some discontinued cards that are no longer open to new applicants remain available to existing cardholders. Those cardholders, who are "grandfathered in," can continue to use cards such as Chase's United MileagePlus Select and United Presidential Plus, the Hyatt Visa or the IHG Rewards Club Select.

It might seem easier to "upgrade" to a new card, or simply close your discontinued card account and apply for a new offer, but there are many reasons why you should keep your card open. Here are a few things to consider before closing your account:

Top reasons to keep a discontinued card open

Whether to keep or cancel a discontinued card depends on several factors: the impact on your credit score, the value you get from the card's annual fee, and the availability of benefits on your old card versus the newer products.

1. The impact on your credit score

The single most important consideration in keeping or canceling a discontinued card is the impact it might have on your credit score.

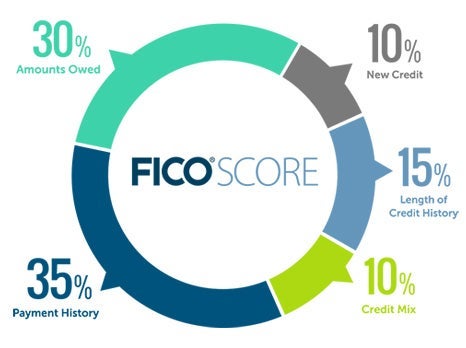

Your credit score is based on five major elements. Your payment history (whether you pay your balances in full and on time every month) counts for 35% of your score. The amounts owed, also sometimes referred to as the debt-to-utilization ratio, counts for 30% of your score. It is a snapshot of how much you are using your overall credit line.The other factors are the length of your credit history and age of accounts, the types of credit you have (i.e., cards versus loans) and how many new lines of credit you have opened recently.

When you close a credit card account, you reduce your overall credit limit and thus increase your utilization rate. Depending on the credit limit you had on that card (as well as the total available credit you have across other cards), that will usually cause a temporary dip in your score.

Before you decide to cancel a discontinued card, check its place in your card lineup — how long you've had the card versus other credit cards, and how much closing it will reduce your overall line of credit. Based on these factors, you might want to keep it open, especially if you are thinking of applying for a mortgage or a car in the near future.

2. Its benefits still make the fee worth it

This consideration is not unique to discontinued cards. If you pay an annual fee for your rewards card, ask yourself each card anniversary year whether or not you get as much or more value from its benefits than the annual fee costs.

After all, it's no good paying $695 per year for the Platinum Card® from American Express (see rates and fees) if you don't take advantage of valuable perks like up to $200 in airline incidental fee credits, up to $200 in Uber credits, a Global Entry or TSA PreCheck reimbursement once every four years (up to $100), access to Centurion Lounges, Delta Sky Clubs and Priority Pass lounges, and elite status with Marriott and Hilton. Enrollment required for select benefits.

To put this into context with discontinued cards, the United Presidential Plus Card costs $450 per year, but comes with United Club access, much like the United Club Card does. That's about $200 less than access costs most travelers without a card. If you use the United Club, this benefit alone could be worth it, though the card offers more, like double miles on purchases from United, hotels and car rental agencies, Premier Access priority check-in and boarding when traveling, and free checked bags.

The information for the United Club card has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.

3. Its benefits aren't available through other cards

Along the same lines, one of the best reasons to keep a discontinued card is that it might offer perks you will not find on newer versions. This is the case for a number of products out there.

One example is the old Hyatt Visa that has an annual fee of $75 and comes with an automatic free night at Category 1–4 hotels each cardmember year. The World of Hyatt Credit Card offers the same benefit (and increased earning on some categories), but costs $95 per year. So you might as well save $20 by hanging onto the old card if this perk is your primary reason for having the card.

On the airline side, Chase still honors the United MileagePlus Select Card, though it's not available to new applicants. It earns 3x miles per dollar on United purchases (currently not offered by any other United card) and 2x on tickets purchased from other Star Alliance member airlines as well as at gas stations, grocery stores, restaurants and home improvement stores. It also awards cardholders with 5,000 bonus miles on each account anniversary, worth around $65 by TPG valuations. In short, it's a top earner for United flyers.

Finally, the Diners Club Premier and Diners Club Elite cards, which are not available for new applications, have some great benefits. The Elite version, which costs $300 per year, earns 3x points per dollar at gas stations, grocery stores and drugstores. Cardholders can access over 700 airport lounges and transfer points to over a dozen airline partners including Air Canada, Delta, Southwest and British Airways.

Before making a decision to cancel or product change, look at the benefits offered by your discontinued card versus those offered by newer versions and see if you would be missing out by canceling.

4. Is an upgrade or downgrade opportunity worth it?

When an issuer discontinues a particular card, members are typically offered the chance to switch to a different product altogether, or "upgrade" to a newer (and generally more expensive) version of the same card. Before doing so, however, make sure the offer is worth it.

For instance, when the Hyatt Visa was first discontinued and cardmembers were asked to upgrade to the World of Hyatt Credit Card, they were offered 2,000 points for doing so – worth around $34. However, folks who were under Chase's 5/24 limit and had gotten the old card more than two years before, should have been eligible to submit an application for the new card and have a shot at sign-up bonus instead.

In a similar circumstance, when Chase shuttered the Fairmont Visa, the bank offered to transition cardholders to the Chase Sapphire Preferred with no sign-up bonus. However, anyone who didn't already have the Sapphire Preferred, should have applied for a new card rather than accept the conversion to have the opportunity to earn its sign-up bonus of tens of thousands of Ultimate Rewards points.

In another case, folks with the old Barclays US Airways Mastercard were automatically sent one of the American AAdvantage Aviator cards. But given the similarity in benefits between those cards and the Citi/AAdvantage cards, it was like having duplicate cards … and having to pay multiple annual fees to boot.

5. Sign-up bonus eligibility

Closing your discontinued card can affect your eligibility for sign-up bonuses on future applications. For example, when Citi discontinued the Citi ThankYou Preferred, the bank soon launched the Citi Rewards+® Card to replace it in Citi's lineup.

Both cards charge no annual fee, and some people might have been tempted to close their account at that point, figuring they could apply for the new card and earn its sign-up bonus. However, Citi has clear language on its applications for ThankYou Points-earning cards that if you opened or closed a card within the ThankYou portfolio in past 24 months, you are ineligible for a sign-up bonus until you are outside that time frame. So closing that account might have made folks ineligible for bonuses on that card as well as the Citi Prestige® Card and the Citi Premier® Card for a substantial period of time.

(The information for the Citi Prestige has been collected independently by The Points Guy. The card details on this page have not been reviewed or provided by the card issuer.)

Before making any moves, read the terms and conditions for closing your current account as well as eligibility requirements for any new card applications to make sure you don't miss out on bonus opportunities.

6. Leverage any unused benefits

If your discontinued card includes a time-sensitive or annual benefit such as anniversary bonus points or a free hotel night, be sure you use it before canceling your card. That's because many of these perks state in their terms and conditions that your account must be open and in good standing in order to receive benefits. You wouldn't want to miss out on hundreds of dollars in valuable perks simply by canceling at the wrong time.

Bottom line

As the credit card marketplace continues to expand and evolve, chances are you have (or will have) a discontinued card. When that happens, evaluate your options carefully, think about whether keeping your card open or closing it will be more or less beneficial to your overall rewards strategy, and how your decisions might affect your credit score and other earning opportunities.

For rates and fees of the Amex Platinum card, click here.