5 basic credit card terms you need to understand

Update: Some offers mentioned below are no longer available. View the current offers here.

If you're new to credit cards, the jargon and acronyms can be intimidating.

TPG can help you demystify the terms, decide which credit card is best for you, and show you the best ways to earn and redeem points and miles.

In this post, let's learn some essential terms and phrases.

Credit score

First, you must understand the concept of a credit score, the number that indicates your "creditworthiness." Credit scores typically range from 300 to 850.

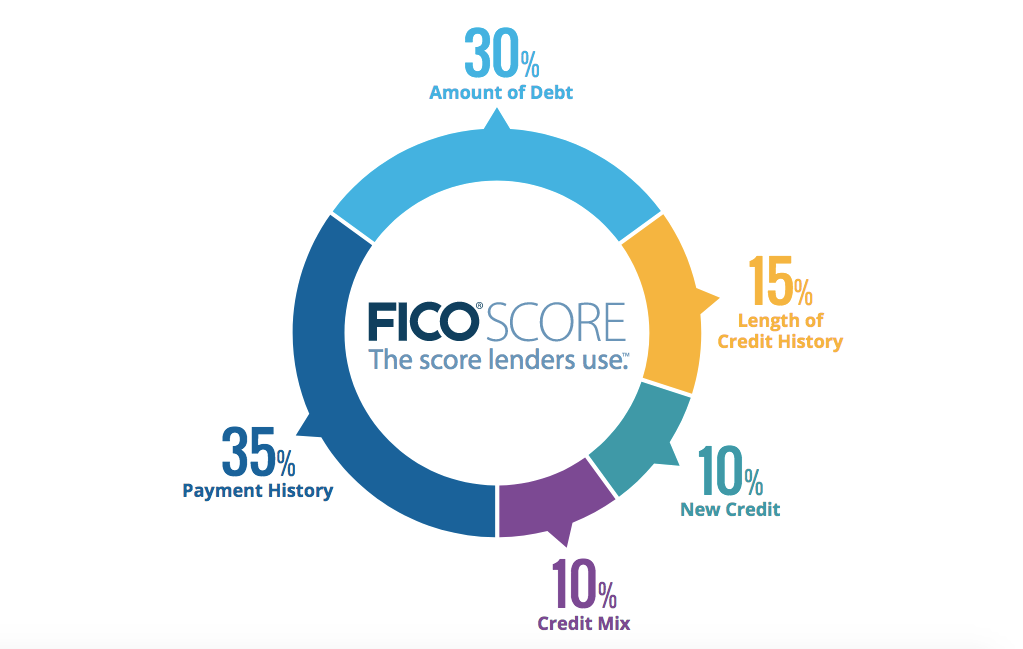

Credit card companies use credit scores to determine if you're a trustworthy candidate for a new account — they are lending you money, after all. FICO is the company most lenders use to obtain your credit score. Your FICO score is based on the following factors:

- Payment history (35%): More than one-third of your credit score is based on how you've managed payments on your credit obligations in the past. Derogatory marks like collection accounts, bankruptcy, foreclosures or tax liens hurt you in this category.

- Amounts owed (30%): You can maintain a good credit score even when you owe a lot of money. However, it's important to keep your debt-to-limit ratio (your "credit utilization") low on revolving credit cards. In fact, paying down credit card balances is often one of the most effective ways to boost your credit score.

- Age of credit history (15%): The average age of your accounts, the age of your oldest account and the age of your newest account can have an impact on your FICO score: Older accounts can help your score, while newer accounts might do the opposite.

- Credit mix (10%): Your credit score could benefit when you have a variety of revolving and installment accounts on your credit report. Revolving accounts are generally credit cards and home equity lines of credit, known as HELOCs. Installment loans can be mortgages, auto loans, personal loans, credit builder loans, etc.

- Credit inquiries (10%): Too many "hard" inquiries on your credit report in a 12-month period can hurt your FICO score. A hard inquiry occurs when you apply for a credit card.

You can check your three credit reports — Experian, Equifax and TransUnion — online for free once every 12 months via AnnualCreditReport.com. Here are other ways to check your credit score for free. It's important to monitor your credit report periodically.

What is a good credit score?

Ideally, you should aim for a credit score of 760 or higher. A score of 760 and up should get you the best treatment available from lenders (including mortgage lenders, auto lenders, and more). In the credit card world, a 740 score may grant you access to almost any credit card on the market.

Related: What is a good credit score?

What does this mean for you?

All the factors that influence your credit score reflect previous activity on your credit report. When you have no open lines of credit, you are said to have "no credit." With a no-credit score, credit card companies may be reluctant to issue you a card.

If you're in this situation, the first step is to establish credit. If you can't qualify for a traditional, unsecured account, consider starting with a secured credit card. With a secured card, you'll need to make a security deposit with the card issuer equal to your new account's credit limit.

The payments you make on the secured card are generally reported to the three major credit bureaus. Be sure to confirm this fact with the card issuer before you apply.

As long as you manage your new secured card properly with on-time payments and low credit utilization, you may be able to qualify for a traditional unsecured credit card in the future. Pay attention to the scoring factors listed above to maintain or improve your credit score over time.

APR

APR stands for annual percentage rate which, by itself, doesn't explain much about the term. Your APR is the interest rate you are charged on your credit card balance over the course of a year.

Credit card interest is generally calculated daily — 1/365 of the APR is multiplied by your current balance and added to it. This process, called compounding, is repeated daily for as long as you carry a balance. However, any interest charged is typically forgiven if you pay your statement balance in full by the due date every month.

Related: 5 mistakes to avoid when you get your first credit card

What is a good APR?

The average APR for credit cards that incur interest was nearly 21.51% as of May 2024, according to the Federal Reserve. An APR closer to 10% may be considered good; 20% or higher is bad. However, the APR on attractive rewards cards is generally higher, even for applicants with good credit. That's why TPG recommends paying off your balance in full each month.

Many cards offer a low introductory APR — as low as 0%. Again, your best bet is to not have to worry about APR at all by paying off the balance every month.

What does this mean for you?

No interest payment, no worries about APR. If you pay your balance each month, it's essentially a short-term, interest-free loan.

Rewards programs

Now, the fun part. Many credit cards offer some type of rewards program, such as:

- Rewards to an airline or hotel loyalty program

- Rewards to a transferable points program

- Cash back

What is a good rewards program?

A good rewards program gives you more bang for your buck. You can often earn up to earn up to 5 points per dollar spent on certain purchases (or even up to 10).

The estimated monetary value of the points varies greatly depending on the rewards program and its redemption options. Our points valuations generally range from 0.5 to 2.05 cents per point, depending on the program. The higher the points valuation, the more value you stand to get when you redeem your credit card rewards.

What does this mean for you?

The credit card you should use depends entirely on your situation. Find a card with annual travel benefits, free hotel nights or other perks that you can use before you apply.

You can start by looking through our best first credit cards or our best rewards credit cards.

Annual fee

Credit cards often charge a fee on your account anniversary to offset the rewards they offer for that account. Annual fees can range from $0 to $550 or more. Typically, the higher the fee, the more generous the card perks.

What is a good annual fee?

If the value of the benefits or bonus earnings associated with the card outweighs the annual fee, that is a good annual fee. Read more about weighing a card's fee against its benefits.

What does this mean for you?

Of course, a good annual fee is determined by the benefits and bonuses that you will use. For example, the $150 annual fee (waived for the first year) for the United℠ Explorer Card (see rates and fees) comes with a free checked bag. The card's annual fee is covered by your savings on checked bags once you take two round-trip flights as a solo flyer. If you fly with a companion, you can also cover the cost of your annual fee with one round-trip flight since you both receive the first checked bag for free. On the other hand, that annual fee does not make sense if you never fly United.

It's a good idea to do a yearly checkup on your cards. Your account anniversary is a good time to evaluate the credit card and decide if the benefits are worth the fee for another year. Typically, credit card companies give you a grace period of a few weeks to get the annual fee refunded after it has been posted if you want to cancel your card. But before you cancel, see if the card issuer is willing to extend a credit card retention offer that might waive or offset your annual fee for the upcoming year.

Credit card vs. charge card vs. debit card

A debit card is different from a credit card in many ways.

For starters, you're not borrowing money when you use a debit card for a purchase. When you use a debit card, the money is deducted from your checking account. There is no credit involved.

Charge cards are much the same as credit cards, at least in practice. Every swipe of a charge card or credit card is a temporary loan from the bank. With charge cards, however, you must pay your balance in full every month. You generally don't have the option to make a minimum payment or to pay a lesser amount.

Charge cards are also different from credit cards when it comes to credit limits. You can't spend an unlimited amount on a charge card, but they don't have a published spending limit like a credit card.

For the merchant, there's a big difference between transaction fees for debit, credit and charge cards. Credit card fees are significantly higher than debit cards. Charge cards are typically the highest of all. But these fees, at least in the U.S., are rarely passed on to the consumer — at least not in a direct way.

What does this mean for you?

When you make a purchase, use the credit card or charge card that gives you the highest return on spending for that specific purchase category. The best choice for dining purchases will usually be different than the optimal pick for spending at office supply stores, for example.

Related: The best cash-back credit cards for each bonus category

Because banks make very little money off a debit card transaction, they typically don't give rewards for debit card purchases. Debit cards are useful for ATM withdrawals and places where credit cards aren't accepted. If you have the option, use a rewards-earning credit or charge card. (Just make sure to manage your cards well and pay off your full statement balance each month to avoid interest.)

In short, carrying a credit card, debit card, and charge card often makes sense.

Bottom line

Obviously, this is only the beginning of the credit card cosmos. Pair this knowledge with our beginner's guide to points and miles and you'll be ready to start earning valuable rewards in no time. Once you get rolling, the sky is the limit.

Related: Getting started with points, miles and credit cards to travel