Why More Retailers Than Ever Are Accepting Amex

Perks and welcome bonuses aside — none of which are insignificant, of course — your credit card is only as useful as the merchants that accept it. That's one area where Amex has historically lagged behind other card issuers such as Visa and Mastercard, which are accepted at many more retailers both in the US and abroad.

Five years ago, Amex started to heavily focus on increasing acceptance so that you can use your card where you want to. Here's a look at the progress it's made in that time.

The Case for Amex

It's obvious why Amex wants you to be able to use your card at more merchants, but the issuer makes a compelling case for merchants to want this as well.

According to a Nilson report, Amex customers spend on average 3.1x a year more than non-Amex customers. Similarly, the average transaction size of an Amex customer is 1.8x larger than a non-card member's. The same report also showed that Amex customers spend an average of $14,000 a year on their cards. In short, Amex customers can be more valuable to merchants because they tend to spend more and make larger purchases.

So why do fewer merchants accept Amex? Historically, the answer has been because Amex charged higher credit card merchant fees than Visa and Mastercard.

According to Amex, this is no longer the case. On average, the cost for merchants to accept Visa and Mastercards has risen, while the cost to accept Amex has decreased over the last 10 years. In that time, Amex has invested heavily in fraud prevention capabilities and other business tools such as Shop Small/Small Business Saturday and Amex Offers. With Amex adding 10 million new card members globally in 2017, businesses now have a much better reason to accept Amex.

It's clear that Amex's initiatives are working, with 1.5 million new locations in the US alone deciding to accept Amex cards in 2017. In 2018, Amex has added at least a million more locations. A big part of this has been Amex's OptBlue program to support small businesses.

OptBlue

The primary goal of OptBlue is to remove the hurdles associated with accepting Amex cards. This program highlights an important point: It's the credit card processor that sets the credit card merchant fees, not Amex itself. OptBlue will help you find a rate that works for your business, and combine your statements and payments no matter what cards you're accepting. This means if your customers use a mix of Visas, Mastercards and Amex cards, you'll still receive one single payment and one statement.

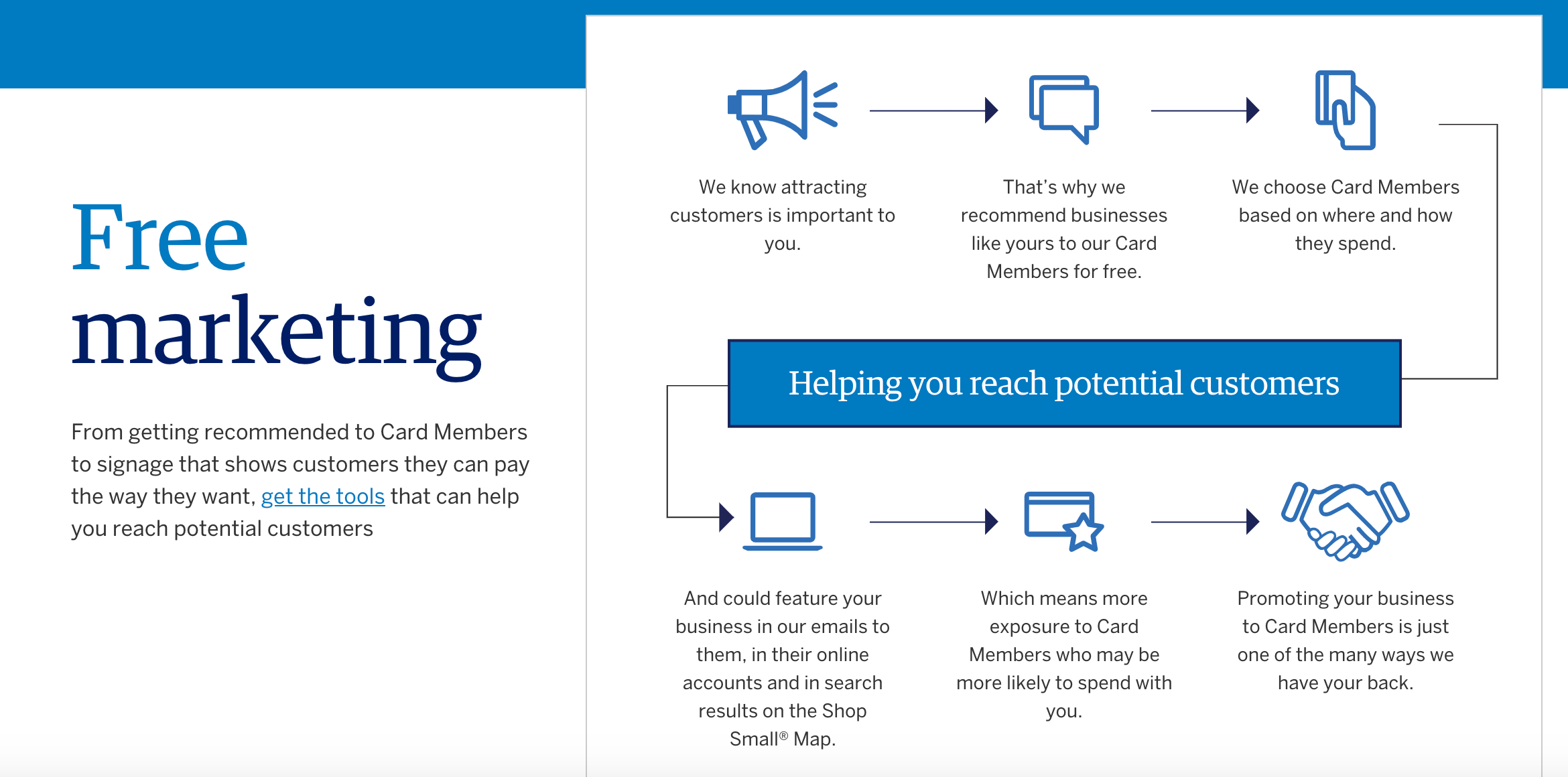

Amex also provides free marketing for OptBlue merchants to drive customer traffic and help Amex customers discover all the places where they can use their cards.

This means everything from providing free signage indicating that a business accepts Amex to promoting the business to Amex card holders, both in email alerts and through their online accounts. Amex will even use a customer's transaction history to promote businesses where they are most likely to spend, all at not cost to the business.

Bottom Line

Amex still has work to do before it completely closes the acceptance gap with Visa and Mastercard, but programs like OptBlue go a long way toward that goal. The issuer expects "virtual parity," or essentially the same level of acceptance as Visa and Mastercard, by the end of 2019. Amex clearly understands how valuable its customers are, and are taking a constructive approach to support businesses and make it easier and cheaper for them to accept Amex cards.

While TPG is partnering with American Express to promote Amex acceptance to merchants, this content is not provided by Amex and any opinions, analyses, reviews or recommendations expressed here are those of the author's alone.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app