3 ways a new credit card could increase your credit score

Editor's Note

For many reasons, you might be in the market for a new credit card. Perhaps you want the opportunity to earn a new welcome bonus or valuable rewards from your everyday purchases or you're looking for a way to boost your credit score.

If the latter is the case, it's important to understand how a new credit card account might affect your credit score.

There are several ways a new credit card could help your credit score, yet there are a few pitfalls to beware of as well. Otherwise, opening a credit card could set your credit score back — either temporarily or in the long term.

Let's discuss three ways a well-managed credit card account has the potential to help your credit score.

Lowers your credit utilization rate

Perhaps the biggest benefit you might receive from a new credit card is the possibility of lowering your overall credit utilization ratio. Credit utilization is a term that describes the percentage of your credit card limits that are in use. Lower credit utilization is better for your credit score.

A new credit card comes with a new credit limit. The new account could trigger a drop in your credit utilization rate if you already have other open credit cards with outstanding balances. This, in turn, might improve your credit score.

Of course, paying off your credit card balances is the best way to lower credit utilization. But if you can't afford to zero out your credit cards, asking for a higher credit limit or opening a new credit card might help you in the short term. You could also consider using a balance transfer credit card as a way to consolidate outstanding credit card balances and reduce your credit utilization at the same time.

Establishes good payment history

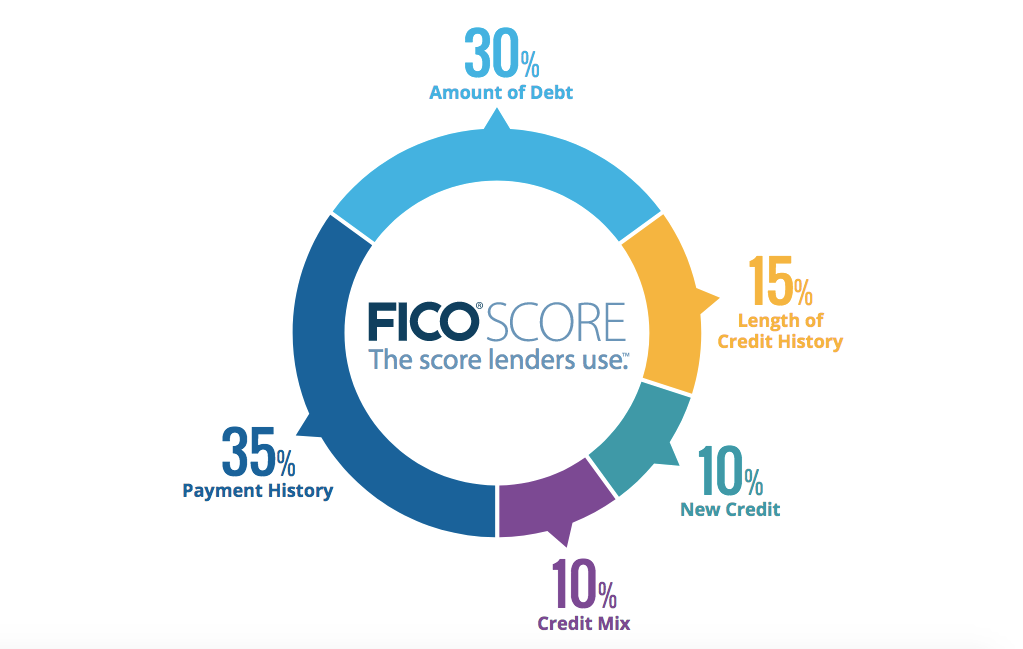

Another way a new credit card might help your credit score is by allowing you to build a solid credit history. Payment history makes up 35% of your FICO score and 41% of your VantageScore credit score. Therefore, if you open a new credit card and always pay on time, the account can help you establish a strong payment history over time.

Additionally, you might benefit from opening a new credit card if you only have a few accounts on your credit report. When you have a "thin" credit file — fewer than five credit accounts — you could have trouble qualifying for a mortgage, leasing an apartment or opening a mobile phone account.

Related: Why paying off credit card balances is more important than ever

Diversify your credit mix

A new credit card might help your credit score by adding account diversity to your credit report. Credit scoring models like FICO and VantageScore pay attention to many details on your credit report.

One of the factors these scoring models evaluate is the mixture of account types you have experience managing, also known as your credit mix. Credit mix is worth 10% of your FICO Score and 20% of your VantageScore.

There are two main categories of credit accounts — installment and revolving. Installment credit generally includes mortgages and auto, student and personal loans. Revolving credit includes credit cards and lines of credit. Having a mixture of these accounts on your credit report can increase your credit score.

Adding a credit card to your credit report might help your credit score if you've never had a credit card. However, if you already have other revolving credit cards appearing on your credit report, you probably shouldn't expect any extra credit score bump in this area.

Related: How do credit scores work?

Credit score pitfalls to avoid when opening a new credit card

- Late payments: Always pay on time. Late payments have the potential to destroy a good credit score. Plus, negative information like late payments can stay on your credit report for up to seven years.

- High credit utilization: A high balance-to-limit ratio tends to be bad for your credit score. Plus, when you revolve an outstanding credit card balance from month to month, you'll typically pay high interest charges as well. It's best to pay your full statement balance every month.

- Applying for too many accounts: You don't have to be nervous to apply for a new credit card when you want to take advantage of an attractive offer. But an excessive number of inquiries in a 12-month period could damage your credit score.

- Opening too many new accounts: When you open a new credit card, your average age of accounts becomes younger. This could trigger a credit score drop in the short term. And if you open too many new accounts at once, credit cards or otherwise, you might see a bigger negative score impact.

- Closing old accounts: In general, it's not a good idea to close old credit cards just because you open a new one. Closing an old credit card (especially an account with a zero balance) can increase your overall credit utilization rate and drop your credit score.

Related: TPG's 10 commandments of credit card rewards

Bottom line

A new credit card often has the potential to help you improve your credit score when you open an account and use it responsibly. However, it's critical to always pay on time. Plus, it's best to pay off your full credit card balance every month as well.

You should also consider reviewing your three credit reports to see where your credit stands before you apply for a new account. Once you know where your credit stands, you'll be better positioned to shop around for the best credit card for your situation.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app