How to make sure your credit is in great shape for the new year

A good credit score can make life easier in so many ways. Good credit (or better yet, excellent credit) can make it easier to qualify for generous rewards credit card offers, of course. It can also help you when you want to apply for other types of financing, such as a mortgage or auto loan. In some states, good credit can even come in handy when you set up an auto insurance policy, since better credit scores may equal lower insurance premiums.

Related: How much money can good credit really save you?

If you're looking for ways to improve your credit or to make sure your credit stays in great shape, we've got you covered. Read on for five tips that can help you achieve and maintain a good credit score.

Review your three credit reports

Knowing where you stand is a critical part of attaining good credit. In other words, you need to review your credit reports from Equifax, TransUnion, and Experian.

Related: Your next credit card approval is in the hands of these 3 agencies

The Fair Credit Reporting Act (FCRA) lets you check your credit reports for free once every 12 months. AnnualCreditReport.com is the website you can visit to claim your federally mandated free reports, where all three major credit bureaus are now allowing free weekly credit report access through this same website.

Take notes

Once you have your credit reports, review each of them from top to bottom. You should make a note of any of the following details you come across.

- Suspicious information: If you find credit reporting errors, incorrect balances, accounts or credit inquiries that you don't recognize, add them to your list.

- Credit cards with balances: The best way to manage your credit cards is to pay off your full balance each month. If you have accounts that you haven't been paying off monthly (and you can't afford to do so), make a list of each credit card and the balance you owe.

In the sections below, we'll break down what to do if you find any of the issues above on your credit report.

Related: 4 incorrect assumptions about your credit score

If you find credit errors, dispute them

Having accurate information on your credit report matters. Your credit reports, after all, are the basis for your credit scores. Credit scores affect your ability to qualify for financing and influence the price you pay for credit when a lender approves you.

According to a survey by Consumer Reports, 34% of consumers found at least one error on their credit reports. In some cases, credit errors can unfairly drive your credit score downward. So, if you find a credit mistake, it's important to address it.

The FCRA works to your advantage in this situation. The federal law lets you dispute any credit report error with the credit bureau that's displaying the incorrect data on your report. When you send a dispute, the credit bureau has 30 days to investigate your claim (sometimes 45 days) and either delete, update or verify the disputed information.

Related: 6 things to do to improve your credit in 2022

Pay down outstanding credit card balances

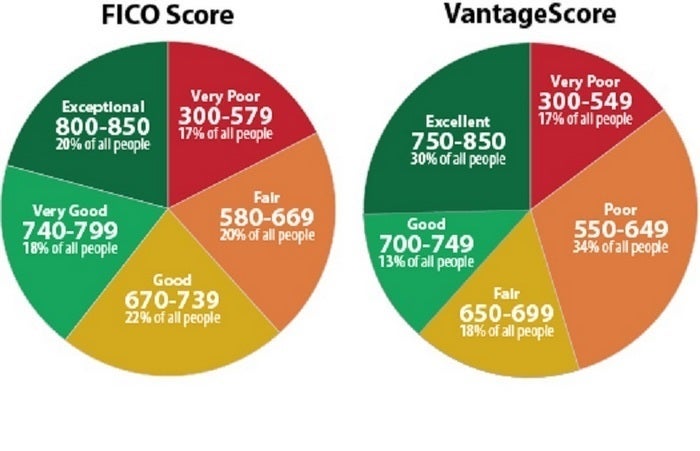

Your FICO® Score can range from 300 to 850, with higher scores indicating that you're a better credit risk. If your credit rating isn't what you want it to be, there are moves you can make to try to improve your credit score.

Some credit score improvement strategies take time. Other approaches, however, have the potential to boost your score faster. Paying down credit card debt is one such strategy.

When you pay down a credit card balance, your credit utilization ratio should decrease. Credit card utilization — the connection between your credit card balances and limits — has a big influence over 30% of your FICO Score. As a rule of thumb, lower credit utilization tends to lead to higher credit scores. And don't forget the biggest benefit of paying off credit card debt — it helps you avoid expensive interest charges.

Related: TPG's 10 commandments of credit card rewards

Use caution when closing credit cards

There are valid reasons why you might want to close a credit card account from time to time — but trying to improve your credit score isn't one of them. In fact, if you don't cancel a credit card the right way, your credit score could drop.

When you close a credit card account, a credit scoring model will no longer consider the account's credit limit in your credit utilization ratio. Without that extra available credit limit, your utilization rate may rise, even if your overall credit card debt stays the same.

The good news is that it's possible to close a credit card without experiencing credit score damage. If all of your credit card balances are $0 according to your credit report when you close an account, no utilization increase should happen.

Related: What to do before you close a credit card

Make on-time payments every time

Not only is it important to pay your credit card bills in full each month, but you also have to pay on time. That rule of thumb applies to every credit obligation you have — credit cards, loans and more. Late payments could damage your credit score in a hurry, even if you're just 30 days past your due date.

If you're worried about forgetting a due date, you might consider scheduling automatic payment drafts for at least the minimum amount due. Setting reminders on your smartphone or computer could also help.

As for any late payments already on your credit report, the negative impact they have on your score has a time limit. The FCRA makes the credit bureaus take late payments off your report once they are seven years old. Furthermore, the older a late payment becomes, the less it affects you. A brand new late payment might have a big impact on your credit score. A late payment that's five or six years old, on the other hand, is less significant from a credit score standpoint.

Bottom line

Keeping your credit score in great shape requires consistent effort. But once you get used to reviewing your credit reports frequently, making on-time payments and paying your credit card balances off each month, these habits become easier to maintain. Best of all, the benefits you can enjoy when you have good credit can pay off over and over again.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.