How do credit scores work?

Update: Some offers mentioned below are no longer available. View the current offers here.

Credit scores are three-digit numbers and usually fall anywhere between 300 and 850 — for financial institutions, they represent the theoretical likelihood you'll repay a loan on time. They're also a little mysterious, and that's no accident. The major credit-scoring companies, FICO and VantageScore, keep their formulas secret. While there are things we do know, only a handful of people know the exact recipe that's used to generate a credit score.

Nevertheless, credit-scoring companies release enough information that experts can largely determine how these numbers are calculated.

Here's what you need to know about how credit scores work.

Credit score basics

Credit-scoring models use a person's credit history from one of the three major consumer credit bureaus: Experian, Equifax or TransUnion. Before credit scores existed, a lender would have to pull a copy of your entire credit report and then analyze it to determine your creditworthiness. But now, they can go off a single number.

Related: Clearing up confusion: Why your credit score may be different depending where you look

What makes up your credit score

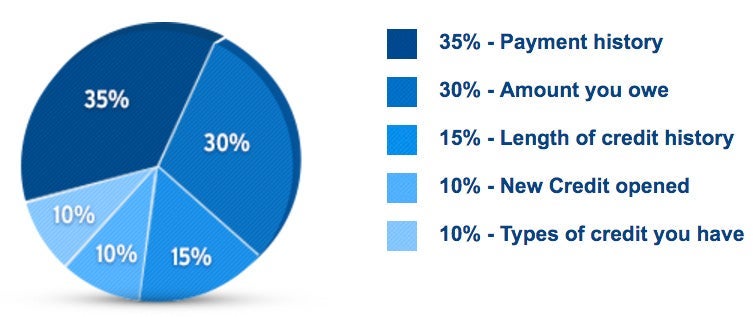

FICO is relatively forthcoming about the overall factors that make up its credit-scoring models:

Payment history: Your payment history comprises 35% of your FICO score. If you get behind in making loan or credit account payments, the longer and more recent the delinquency, the greater the negative impact on your credit score.

Amounts owed: 30% is based on the relative scale of your current debt. In particular, your debt-to-credit ratio is the total of your debts divided by the total amount of credit you've been extended across all accounts. Lenders generally like to see a debt-to-credit ratio below 30%, but the lower, the better.

Length of credit history: 15% is based on the average age of all accounts on your credit history. This becomes a significant factor for those with very little credit history, such as young adults, recent immigrants and anyone who has largely avoided credit. It can also be a factor for people who open and close accounts within a very short period.

New credit: 10% is determined by your most recent accounts. Opening too many accounts within a short time frame might have a negative impact on your score, as the scoring models will interpret this as a sign of possible financial distress.

Credit mix: 10% is related to how many different types of credit accounts you have, such as mortgages, car loans, credit loans and store charge cards. While having a larger mix of credit accounts is better than having fewer, no one recommends taking out unnecessary loans to diversify your credit and boost your score.

Related: How to check your credit score for free

How to boost your credit score the traditional way

Pay your bills on time consistently

Consistently paying your bills on time is the most important way to improve your credit score. Thankfully, most lenders won't report delinquencies less than 30 days old, and many won't even report payments that are 30 to 60 days late. But once you get beyond 60 days, each late payment will dramatically affect your credit score.

Most of your accounts allow you to take extra steps to ensure you'll pay your bills on time, like setting up alerts, reminders and automatic payments. Take advantage of these options to help ensure you'll never miss a payment.

Related: 6 things to do to improve your credit

Lower your debt-to-credit ratio

Your debt-to-credit ratio is the total amount of debt you have divided by the total amount of credit you've been extended across all accounts. There are two ways to decrease your debt-to-credit ratio: by decreasing your debt and increasing your credit.

This is why applying for a new credit card can actually help your credit score. Increasing your available credit, either through existing accounts or by opening a new account, should decrease your debt-to-credit ratio — if you don't take on more debt. This is also why, if you plan on canceling a credit card, you'll want to move the line of credit on that card to another card to keep your overall line of credit as high as possible.

Related: Credit utilization ratio: What is it and how it affects your credit score

Avoid opening new credit lines too quickly

After making on-time payments and reducing your debt-to-credit ratio, the next important thing you need to remember is not opening many new credit card accounts or other loans in a short amount of time. Card issuers don't want to loan money to someone who appears to be seeking a lot of new loans, as that could be a sign of financial instability.

Related: How does applying for a new credit card affect my score?

Correct errors

Another way you can improve your credit score is to correct any errors you find in your credit history.

You can request credit reports for free from the three major credit bureaus and check for errors. If you find any mistakes, request corrections, as those errors could significantly impact your credit score.

Related: How to correct errors on your credit report

Ask for forbearance

When you've made a mistake that's affected your credit report and score, you can ask the lender to remove the negative information. Simply call or write the lender, explain the mistake and politely request that they amend your credit history to remove the record.

In our experience, this works best for minor mistakes on an account with an otherwise spotless payment record. And before asking for forbearance, ensure your account is no longer delinquent.

Common misconceptions about credit scores

There's a quick fix for bad credit

Like ads for magical pills that supposedly allow you to lose weight without diet and exercise, plenty of people claim to have discovered (and will try to sell you) a quick fix for bad credit.

The truth is that you have to pay your bills on time and carry very little debt. If you do those two things and have a significant credit history, you'll have a great credit score. But if you have a record of late payments and a high level of debt, it will take some time and consistent good credit habits to pull your score up.

Related: 3 real ways to boost your credit score in 30 days

Fewer credit cards are better

Many of us at TPG have numerous credit card accounts. In response to hearing that, some conclude that our credit must be terrible and are surprised to learn that we have excellent credit not despite our numerous accounts — but because of them.

When managed responsibly, each account adds positive information to your credit history and helps you maintain a high credit score. So, if you have little-used accounts with no annual fee, there's really little reason to close them.

Look at it from the lender's perspective: Would you rather offer a new line of credit to someone with a very limited record of paying back loans or someone with a very extensive history of managing multiple credit lines responsibly?

Related: Yes, I have 22 credit cards; here's why

0% is the ideal credit utilization ratio

By never using your credit cards or by paying off your balances before the statement closes, it's possible to have a credit report that shows 0% utilization. But it's actually better to have a very low utilization ratio as opposed to 0% utilization.

Again, the credit-scoring models favor those who use credit responsibly over those who don't use it at all.

Bottom line

Knowing how your credit score works is incredibly important. Having a higher score is ideal, so understanding the ins and outs of how it is determined can help you make better financial decisions.

It is also never too late to try to improve your score. If you are in a position where your credit score is low, there are many things you can do to move that score up the scale. While it won't happen overnight, just a few changes can go a long way and affect whether or not you'll be approved for a new line of credit.