Debunking Credit Card Myths: Should You Accept a Credit Line Increase?

Update: Some offers mentioned below are no longer available. View the current offers here.

We frequently discuss travel rewards credit cards here at TPG. These cards allow you to earn top sign-up bonuses and provide numerous bonus categories for everyday spending, unlocking terrific redemptions like premium-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll continue our new series that debunks these myths and allows you to begin planning for your next vacation.

Previous entries includes having too many cards, closing a card you don't use, how permanent of an impact an application has on your score, not paying your balance in full, paying an annual fee, keeping your points when canceling a card, whether annual fees count toward a sign-up bonus, what to do if your application isn't immediately approved and whether cards are a surefire way to get into debt. Today I'll build on the most recent post and look at a myth related to your credit limit.

Myth #10: You should never accept a credit line increase.

One of the most important aspects of using a credit card is your credit limit. A card issuer wants to give you a high enough line of credit to encourage you to use your card but not so high that you'll default on the account. However, the initial limit you get when you open a new card isn't set in stone. As you prove your creditworthiness, an issuer may want to increase the amount of credit you have available.

This actually just happened to me on my Club Carlson Premier Rewards Visa Signature Card. I received a mailer offering me an extra $3,000 of credit on the card. I immediately followed the instructions provided and received an e-mail confirmation a few weeks later:

For some readers out there, this may seem like a recipe for disaster. Opening up additional credit can be a slippery slope if you struggle to manage your credit card accounts. However, as long as you don't use this increased credit line as "free" money, this can actually have a positive impact on your credit profile.

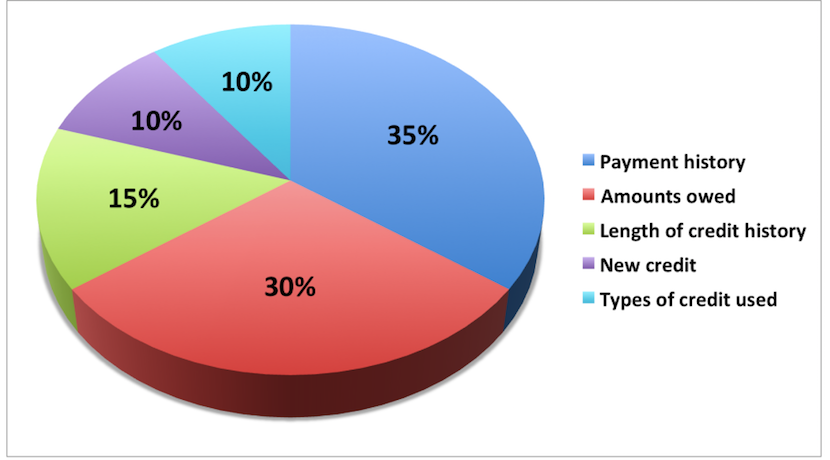

Let's quickly review the key factors that make up your FICO score, the one most frequently used to determine your creditworthiness:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

As we've discussed before, these five factors aren't created equal. Instead, they are weighted based on how important they are to your score:

When it comes to accepting a credit line increase, it's the second-most important factor (amounts owed) that comes into play. This is commonly referred to as your credit utilization rate, and it basically identifies how much of your available credit you are using. It is typically expressed as a percentage and calculated as follows:

Total balance on your account(s) / Total limit of accounts = Utilization

When this number is low, credit issuers see that you can effectively manage your credit and aren't at a significant risk for default.

Here's how a credit line increase can help this factor: Let's say that you have a single card with a $10,000 limit, and at any given time, you typically have a balance of roughly $1,500 (though you of course pay it off in full each month, my top commandment for travel rewards credit cards). Your utilization is thus 15%. This isn't particularly high but still may prevent you from adding a new card to your wallet, especially a premium one like the Chase Sapphire Reserve.

Now let's say that you're offered an increase of $5,000 and don't charge any more on the card each month. With that single change, your utilization drops to just 10%, making your credit profile more attractive to issuers. Of course, there are many other ways to improve your credit score, but as long as you don't take a credit line increase as an invitation to rack up debt, you shouldn't be afraid to accept one.

Bottom Line

Opening and utilizing a travel rewards credit card does carry some risk, and you may think that accepting a credit line increase is an easy way to enhance that risk. However, this can actually help boost your credit score, as long as you manage the higher credit limit carefully. If you're lucky enough to get targeted for one of these offers, don't just discard it! Hopefully this post has given you some insight into the benefits involved.

What are your thoughts on credit line increases?

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app