Debunking Credit Card Myths: Does It Matter If I Don't Pay My Balance In Full?

It's no surprise that travel rewards credit cards are a common topic of conversation here at TPG. Taking advantage of top sign-up bonuses and utilizing bonus categories and other maximization strategies, you can unlock fantastic redemptions like premium-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll continue our new series that debunks these myths and allows you to begin planning for your next vacation. I started with having too many cards, closing a card you don't use and how permanent of an impact an application has on your score. Today I'll move on to another hot topic.

Myth #4: Not paying my balance in full isn't a big deal.

There are times I have to be very careful when it comes to who I tell about The Points Guy. Credit cards can be a gateway to terrific travel rewards, but if you aren't disciplined, you can easily fall victim to treating your accounts as "free money." I have some friends who are still climbing out of credit card debt they racked up during college or shortly after graduation. They'd be the first to give you a simple bit of advice, one that also earned the top spot on my list of Ten Commandments for Travel Rewards Credit Cards: Pay your balance in full.

There are two main reasons why this is critical. The first (and most important) one involves interest rates. Most popular travel credit cards like the Chase Sapphire Preferred Card impose a relatively high Annual Percentage Rate (APR) that is charged when you don't pay your balance in full, typically ranging from 15-25%. Without getting too far into the weeds, most issuers will actually impose interest on all credit card purchases. This happens on a daily basis according to the average daily balance of your card. However, these charges will then be waived when you pay your statement in full on (or before) the due date. If you don't, you'll be subject to interest for the remaining unpaid amount across the entire billing period, and this can easily cancel out any points or miles that you have earned.

For simplicity's sake, let's say you make a $1,000 purchase on the first day of your billing cycle on a card that has an APR of 20%. However, you then only pay $500 of it off when your statement closes. At a 20% APR, your daily rate is roughly 0.0548%. This is charged on the remaining $500 for every day of that billing period. Assuming it's 30 days, you're now responsible for paying approximately $8.22 in interest, and this interest will continue to accrue as long as you carry that balance. This isn't an earth-shattering amount, but paying an extra $8.22 to earn travel rewards on a $1,000 purchase may not be the smartest decision.

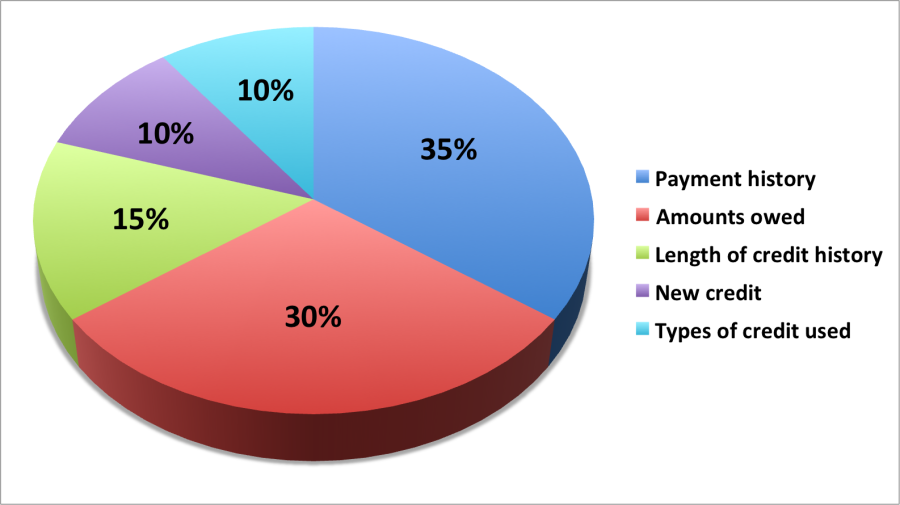

The second reason it's essential to pay your balance in full involves your credit score. As I mentioned in previous entries in the series, there are five factors that contribute to your FICO score:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

Remember that not all factors are created equal, and these five are weighted based on how important they are to your score:

When you don't pay your credit card in full each month, it could wind up impacting the second most important aspect of your credit score: your amounts owed, commonly referred to as your credit utilization rate. This looks at how much of your credit you are actually using and is typically expressed as a percentage. Here's the calculation:

Total balance on your account(s) / Total limit of accounts = Utilization

Keeping this number low shows issuers that you can effectively manage your credit lines and aren't at risk of overextending yourself. When you regularly carry a balance from month to month, it can indicate that you may have trouble making payments in the future. Keep in mind that even if you do pay your balance in full, your credit utilization won't automatically be zero (since most card issuers will report your statement balances to the major credit bureaus). However, not paying your full statement balance each month will ensure that the remaining amount will definitely appear on your credit report and over time could impact your score.

For some additional tips on how to successfully manage your credit cards, be sure to check out my post on Ten Commandments for Travel Rewards Credit Cards.

Bottom Line

There are a lot of myths when it comes to using and then paying off credit cards, especially as it relates to paying your balance in full. Many may think that it isn't a big deal to carry a balance from month-to-month, but when you factor in the interest charges as well as the potential long-term impact on your score, it generally always makes financial sense to pay your full statement balance every month. The general rule of thumb for credit card usage applies here: always spend within your means.

For additional information on your credit score and credit cards, check out the following posts:

- How Credit Card Applications Affect Your Credit Score

- 5 Things To Understand About Credit Before Applying For Cards

- Should I Be Concerned About A Credit Card Denial?

- Credit Card Application Restrictions for the Major Issuers

- 5 Lesser-Known Things That Affect Your Credit Score

- Will My Credit Score Drop If I Don't Use My Credit Cards?

What are your thoughts on paying your full statement balance every month?

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app