How an Expat Went From 0 Credit to 7 Cards and 1 Million Miles

Update: Some offers mentioned below are no longer available. View the current offers here.

If you're a newcomer to the US or are just starting to build credit with the goal of opening travel rewards cards, the road ahead of you can deem daunting. But, as TPG Contributor Mike Toledo explains, it's entirely possible to grow your credit score from scratch and eventually get incredible value out of the most lucrative credit cards on the market.

I've traveled quite a bit in the last 10 years, but I only recently learned how to travel for free. Normally, it would take me two years of traveling at a good pace to have enough miles to get me somewhere I really wanted to go, but now I know there's a shortcut to that.

I moved to the US a few years back to seek an MBA, and at that time I didn't know much about miles but the basics: You fly, you earn miles (not enough miles), fly more and struggle to find availability. After years of casual traveling, you'll hopefully have enough miles to book an award flight.

Houston has been home for me over the last three years, and during that time I've been flying exclusively with United. At the beginning, while traveling almost every weekend out of George Bush Intercontinental (IAH), I didn't get the hype around the United MileagePlus Explorer Card, which was advertised all over the place. I'd always been skeptical about credit cards, so it took me a few trips before I took a look at the card's brochure on board a United flight. Upon viewing the card's benefits, though, I knew right away that it was made to be in my wallet.

My First Credit Card

One of the first things I did when moving to the US was open a checking account with Bank of America as suggested by my school. Back in Mexico, I was taught to be very careful about credit cards and to avoid them completely if possible. Therefore, I wasn't interested in any of them at all, until a year later when I read that brochure and realized how nice it would be to enjoy benefits like priority boarding and a free checked bag at practically no additional cost.

Even though I had zero credit history, I took the chance and applied for the United MileagePlus Explorer Card. As expected, my application was declined. Right away, I began working on a strategy to build my credit and get that card in my wallet. As a first move, I went to my Chase branch and talked to an account executive about my goal, though I quickly learned that they don't have anything to do with the approval process. I even asked if there was an option for me to get it as a secured card, but this wasn't possible. For information on another strategy for building credit, see Akash Gupta's post, How to Start Building Credit with an Authorized User Account.

Instead of getting discouraged, I tried to understand how they would think about an applicant like me. So I said, why would they want to issue me a credit card if they don't even know me, a total stranger who could run away to Mexico at any time?

This was now my plan of action:

1. I went to Bank of America where they actually "knew" me and applied for a basic credit card. I got approved on the spot for my very first credit card in the US! I got the Bank of America® Travel Rewards credit card with only a $1,000 line of credit — enough to start building my credit score.

2. I went to Chase and opened a savings account. Nobody specifically recommended this or guaranteed it would make any difference in whether I got approved for a card, but I did this as a way to build some rapport with the institution. Instead of being a total stranger, I could be an acquaintance.

I made every single purchase with this card, and since the line of credit was very low, almost every month I had to pay off my balance multiple times before the end of the cycle. To be honest, I didn't focus on this card's rewards, but at the end of the year I got about $500 in statement credits!

Just Like Magic

About a year into this strategy, with an upcoming trip to Australia and an increased sign-up bonus currently available for the United MileagePlus Explorer Card, I decided to give it another shot. I applied again and... voila — I was approved! I was super excited; it's not like I won the lottery, but for me it was like a dream coming true and the beginning of new adventures overseas. The card's benefits kicked in right away on my Australian trip. Without a doubt, the biggest perk has been boosting my United MileagePlus account balance. I've accrued about half a million miles in two years of having this card in my wallet.

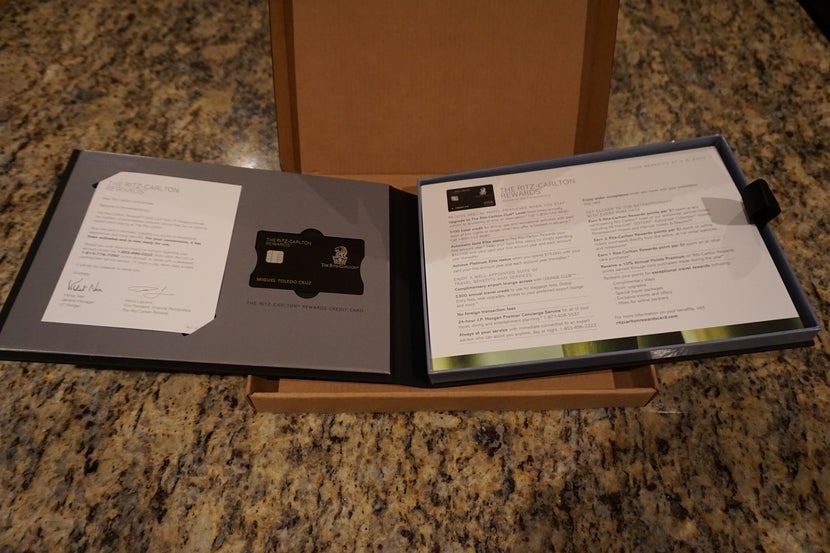

Once I was into the points and miles game, I couldn't stop reading about how to maximize my spending to get free stuff out of it. For business travel, I stay at Marriott properties and have held Silver Elite status. About six months after getting my United card, I saw a great offer (now expired) for The Ritz Carlton Rewards Credit Card: 140,000 points — not half bad!

Considering that this is a premium card with a $450 annual fee — not to mention the fact that I'm not exactly a frequent customer at Ritz properties — I wasn't convinced that this was a good choice for me. While I do stay at Ritz-Carlton hotels occasionally, I spend most of my nights abroad at Marriott properties. Still, since Ritz-Carlton Rewards and Marriott Rewards programs pretty much operate as a consolidated program (even though they appear to be separate), I could still use some of the perks offered by the Ritz-Carlton Card.

Since Chase now "knew" me a little better, I took the chance and applied for it. To my surprise, I was approved right away with a significantly greater line of credit. Today, I can say I'm squeezing all the juice out of The Ritz Carlton Rewards Credit Card with these perks:

- Gold status for the first year of account opening.

- Three complimentary upgrades to Ritz-Carlton Club Level per year. I normally don't get to use all of these, but that's worth at least $500-$1,000 per stay for me.

- A $300 annual travel credit, which helps subsidize the annual fee.

- Lounge Club membership to access hundreds of airport lounges around the world (Trust me, I use them!)

- Everybody has something to say about this metal card. Waiters ask, "Is this metal?" I've also heard, "This is heavy! Must have a bunch of money on it!"

There are still more benefits with this card, but these alone make the $395 annual fee worth it for me. In a couple of weeks I'm taking a trip to Seoul paid for entirely with the 600,000 points I've accrued with this card in just over a year. I redeemed 420,000 Marriott Rewards points for a Hotel + Air package with seven nights at a Tier 1-3 Ritz-Carlton property (in this case, the Ritz-Carlton Seoul) and 120,000 AAdvantage miles, just short of the 125,000 (pre-devaluation) I needed to book American Airlines first class round-trip to Seoul.

What's Next for Me?

With some research into how credit scores work, I've been able to build a credit score of 750+, which is not bad at all. At this time, a couple of credit factors are negatively impacting my score: age of credit history and total accounts. Fortunately, neither is hurting me too badly, though. As long as I keep paying off my cards in full by my due date, my credit score should keep improving little by little.

I've become more serious about the points and miles hobby, and luckily I haven't been declined for any more credit card applications. Now, I'm focusing on diversifying my spending to accrue points in other programs with valuable currencies. I'm also planning a round-the-world honeymoon on points and miles — in premium cabins and with stays at nice hotels, but most importantly without breaking the bank.

Today, my wallet is considerably heavier than it used to be, and that's because I'm carrying these awesome products with me:

- Bank of America® Travel Rewards credit card

- United MileagePlus Explorer Card

- The Ritz-Carlton Rewards Credit Card

- Chase Sapphire Preferred

- Platinum Delta SkyMiles® Credit Card from American Express

- Starwood Preferred Guest® Credit Card from American Express

I'm also looking for ways to generate points in Mexico as well — Mexican credit cards aren't as lucrative and the benefits aren't as valuable, but I still hold the Mexican versions of these cards:

- American Express Gold Card

- American Express Gold Card Aeromexico

- Citi Premier® Card

Finally, by the end of the year I'm planning to sign up for the Citi Prestige Card. I've been looking into this card for a while now, and I'm sure its 4th Night Free benefit and other perks like the annual $250 air travel credit will more than cover the $450 annual fee.

Bottom Line

Do I still think credit cards are bad? Not at all. Do I think we need to take care and watch them closely? Absolutely! A credit card is a double-edged sword; it might bring you a ton of benefits and travel protection, but at the same time your interest may increase exponentially if you don't pay your balance on time. One of the most important things I've learned since I moved to the US is that everything is based on your credit, so you need to watch yours carefully.

Still, through responsible credit card spending, I've been able to go from zero credit to a solid score and millions of travel rewards points, allowing me to redeem for amazing trips along the way. If you're starting out in a similar position, hopefully this post inspires you to get started with a smart credit-building strategy.

What are your favorite tips for building credit and starting to earn travel rewards as a newcomer to the US?

TPG featured card

Rewards

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 3X | Earn 3X Membership Rewards® points per dollar spent on flights booked directly with airlines or on AmexTravel.com. |

| 2X | Earn 2X Membership Rewards® points per dollar spent on prepaid hotels and other eligible purchases booked on AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Intro offer

Annual Fee

Recommended Credit

Why We Chose It

There’s a lot to love about the Amex Gold. It’s a fan favorite thanks to its fantastic bonus-earning rates at restaurants worldwide and at U.S. supermarkets. If you’re hitting the skies soon, you’ll also earn bonus Membership Rewards points on travel. Paired with up to $120 in Uber Cash annually (for U.S. Uber rides or Uber Eats orders, card must be added to Uber app and you can redeem with any Amex card), up to $120 in annual dining statement credits to be used with eligible partners, an up to $84 Dunkin’ credit each year at U.S. Dunkin Donuts and an up to $100 Resy credit annually, there’s no reason that foodies shouldn’t add the Amex Gold to their wallet. These benefits alone are worth more than $400, which offsets the $325 annual fee on the Amex Gold card. Enrollment is required for select benefits. (Partner offer)Pros

- 4 points per dollar spent on dining at restaurants worldwide and U.S. supermarkets (on the first $50,000 in purchases per calendar year; then 1 point per dollar spent thereafter and $25,000 in purchases per calendar year; then 1 point per dollar spent thereafter, respectively)

- 3 points per dollar spent on flights booked directly with the airline or with amextravel.com

- Packed with credits foodies will enjoy

- Solid welcome bonus

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $6,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 3X Membership Rewards® points per dollar spent on flights booked directly with airlines or on AmexTravel.com.

- Earn 2X Membership Rewards® points per dollar spent on prepaid hotels and other eligible purchases booked on AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- $120 Uber Cash on Gold: Add your Gold Card to your Uber account and get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an American Express Card for your transaction. That’s up to $120 Uber Cash annually. Plus, after using your Uber Cash, use your Card to earn 4X Membership Rewards® points for Uber Eats purchases made with restaurants or U.S. supermarkets. Point caps and terms apply.

- $84 Dunkin' Credit: With the $84 Dunkin' Credit, you can earn up to $7 in monthly statement credits after you enroll and pay with the American Express® Gold Card at U.S. Dunkin' locations. Enrollment is required to receive this benefit.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year after you pay with the American Express® Gold Card to dine at U.S. Resy restaurants or make other eligible Resy purchases. That's up to $50 in statement credits semi-annually. Enrollment required.

- $120 Dining Credit: Satisfy your cravings, sweet or savory, with the $120 Dining Credit. Earn up to $10 in statement credits monthly when you pay with the American Express® Gold Card at Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, and Five Guys. Enrollment required.

- Explore over 1,000 upscale hotels worldwide with The Hotel Collection and receive a $100 credit towards eligible charges* with every booking of two nights or more through AmexTravel.com. *Eligible charges vary by property.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.

Rewards Rate

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 3X | Earn 3X Membership Rewards® points per dollar spent on flights booked directly with airlines or on AmexTravel.com. |

| 2X | Earn 2X Membership Rewards® points per dollar spent on prepaid hotels and other eligible purchases booked on AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Intro Offer

You may be eligible for as high as 100,000 Membership Rewards® Points after spending $6,000 in eligible purchases on your new Card in your first 6 months of Membership. Welcome offers vary and you may not be eligible for an offer.As High As 100,000 points. Find Out Your Offer.Annual Fee

$325Recommended Credit

Credit ranges are a variation of FICO® Score 8, one of many types of credit scores lenders may use when considering your credit card application.Excellent to Good

Why We Chose It

There’s a lot to love about the Amex Gold. It’s a fan favorite thanks to its fantastic bonus-earning rates at restaurants worldwide and at U.S. supermarkets. If you’re hitting the skies soon, you’ll also earn bonus Membership Rewards points on travel. Paired with up to $120 in Uber Cash annually (for U.S. Uber rides or Uber Eats orders, card must be added to Uber app and you can redeem with any Amex card), up to $120 in annual dining statement credits to be used with eligible partners, an up to $84 Dunkin’ credit each year at U.S. Dunkin Donuts and an up to $100 Resy credit annually, there’s no reason that foodies shouldn’t add the Amex Gold to their wallet. These benefits alone are worth more than $400, which offsets the $325 annual fee on the Amex Gold card. Enrollment is required for select benefits. (Partner offer)Pros

- 4 points per dollar spent on dining at restaurants worldwide and U.S. supermarkets (on the first $50,000 in purchases per calendar year; then 1 point per dollar spent thereafter and $25,000 in purchases per calendar year; then 1 point per dollar spent thereafter, respectively)

- 3 points per dollar spent on flights booked directly with the airline or with amextravel.com

- Packed with credits foodies will enjoy

- Solid welcome bonus

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $6,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 3X Membership Rewards® points per dollar spent on flights booked directly with airlines or on AmexTravel.com.

- Earn 2X Membership Rewards® points per dollar spent on prepaid hotels and other eligible purchases booked on AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- $120 Uber Cash on Gold: Add your Gold Card to your Uber account and get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an American Express Card for your transaction. That’s up to $120 Uber Cash annually. Plus, after using your Uber Cash, use your Card to earn 4X Membership Rewards® points for Uber Eats purchases made with restaurants or U.S. supermarkets. Point caps and terms apply.

- $84 Dunkin' Credit: With the $84 Dunkin' Credit, you can earn up to $7 in monthly statement credits after you enroll and pay with the American Express® Gold Card at U.S. Dunkin' locations. Enrollment is required to receive this benefit.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year after you pay with the American Express® Gold Card to dine at U.S. Resy restaurants or make other eligible Resy purchases. That's up to $50 in statement credits semi-annually. Enrollment required.

- $120 Dining Credit: Satisfy your cravings, sweet or savory, with the $120 Dining Credit. Earn up to $10 in statement credits monthly when you pay with the American Express® Gold Card at Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, and Five Guys. Enrollment required.

- Explore over 1,000 upscale hotels worldwide with The Hotel Collection and receive a $100 credit towards eligible charges* with every booking of two nights or more through AmexTravel.com. *Eligible charges vary by property.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.