The Fidelity Amex Card: Is 2% Cash Back Good Enough?

Update: Some offers mentioned below are no longer available. View the current offers here.

Cash-back rewards are often passed over by award travel enthusiasts for more glamorous airline and hotel points, but they can play an important role in your overall earning strategy. Today TPG Contributor Nick Ewen looks at one of the stronger cash-back credit card options, and discusses whether it should have a place in your wallet.

When it comes to earning points, whether through credit cards, bonuses, or actual travel, TPG and I agree on one basic strategy: diversification! Building up your account balances in a variety of programs is the key to protecting against devaluation, which can happen with little (or no) notice at all.

Cash-back credit cards are an important part of the diversification strategy, as you (hopefully) shouldn't have to worry about the Department of the Treasury suddenly announcing that $1 is worth 50 cents.

Today I'll discuss a credit card that has at times been the measuring stick for all other cash-back cards, but has recently become less impressive thanks to tougher competition: the Fidelity Investment Rewards American Express.

For starters, it's important to realize that while cash-back cards are popular and an important component of a diversified rewards portfolio, they're not an efficient way to fly in first class on the Emirates A380 or snag a room at the Conrad Maldives. Instead, they usually offer a standard rate of return on purchases in the form of statement credits or cash deposited into your bank account.

TPG did a detailed review of the top cash-back credit cards in September, in which he highlighted the benefits of these cards:

- Flexibility: When you make purchases on a cash-back card, you aren't earning points or miles in a specific program. Your rewards can be applied to any purchase, and you aren't locked into redeeming them with a certain airline or hotel.

- Simplicity: While some cash-back cards offer rotating bonus categories (like the Chase Freedom and Discover It Cash Back), many others offer a standard earning rate, generally between 1-2%. This can make it easier to decide which card to use for a specific purpose (though remember that the new TPG To Go app can help with this as well!). Cash-back cards are a good place to start if you're new to the points & miles game. (The Chase Freedom is no longer open to new applicants)

- Inexpensive: Many cash-back credit cards don't have an annual fee; the only one in the September post with a fee is the Blue Cash Preferred® Card from American Express ($95). This is another appealing attribute if you're new to the game, as you can get started without an initial expense.

However, no two cards are created equal, and TPG's September analysis highlights the differences among these products. So how does the Fidelity Amex stack up? Here are the key benefits of the card:

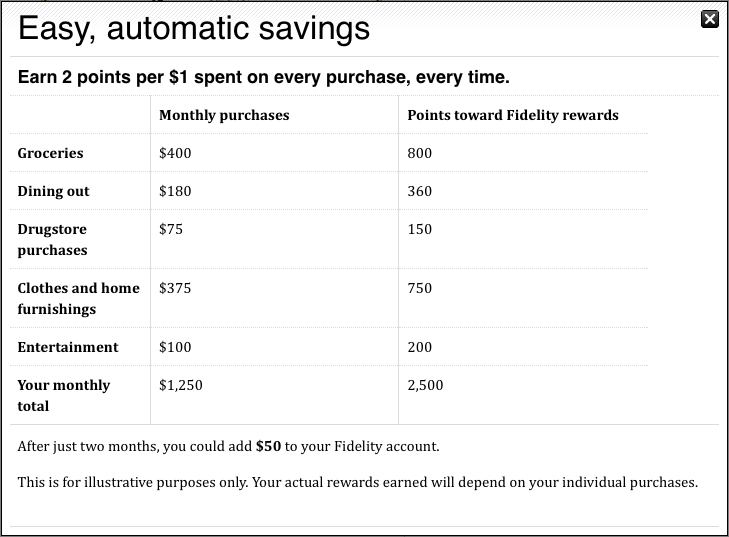

- Earn 2% cash back on all purchases

- Zero liability fraud protection

- Identify theft recovery services

- Purchase protection

- Car rental loss/damage protection

- Travel & emergency assistance

- No annual fee

Though the new Citi Double Cash Card offers a similar effective rate of return (with 1% earned on every purchase and 1% earned as you pay off your balance). Since TPG always recommends paying your balance off in-full every month, the cards are tied, but still ahead of numerous other cash-back cards that only offer 1 - 1.5% back on purchases.

Some cash-back cards may do better than 2% if you can take advantage of a banking relationship that improves your return, but since those programs have additional requirements, it's not an apples to apples comparison.

The big downside of the Fidelity Amex is how you receive the 2% cash-back: it must be deposited into an eligible Fidelity account. This includes cash management accounts, IRA's, or 529 plans. If you aren't a current Fidelity customer, the cash management account has no minimum requirement and no monthly maintenance fees. However, you may not want to go through the hassle of opening a new account just to earn cash-back, especially when there are other options out there.

The card also comes up short in a few other ways, as follows.

No sign-up bonus The Fidelity American Express has previously offered a sign-up bonus, but right now it doesn't. While cash-back cards tend to have lower sign-up bonuses than other rewards cards, those that do offer them can bump up your earning potential. Here's a quick run-down of current offers, along with how much you would need to spend on the Fidelity Amex to make up for the lack of a sign-up bonus.

- Bank of America Cash Rewards Credit Card: $100 after spending $500 in the first 90 days. Since the card offers a standard 1% back on purchases, you would need to spend $10,000 or more on the Fidelity Amex in your first year to equal the cash-back you would get on this card.

- Capital One Quicksilver Cash Rewards Credit Card: $150 after spending $500 in the first three months of account opening. Since the card offers a standard 1.5% back on purchases, you would need to spend $20,000 or more on the Fidelity Amex in year one to equal the cash-back you would get on the Quicksilver.

- Chase Freedom: $150 sign-up bonus after spending $500 in first three months. Since the card offers standard 1% back on purchases, you would need to spend $12,500 or more on the Fidelity Amex in year one to equal the cash-back you would get on the Freedom.

Category Bonuses As I mentioned above, some cash-back cards offer category bonuses that can make them more lucrative than the Fidelity Amex, depending on your typical purchase patterns in a given year. Here's an overview of cards that offer such bonuses, and how much you would need to spend on the Fidelity Amex to break even when it comes to cash-back.

- Bank Americard Cash Rewards: 3% back on gas and 2% back at grocery stores (up to $1500 per quarter). This card will offer better bang for your buck than the Fidelity Amex if you, 1) Typically spend more at gas stations than you do on purchases outside of gas stations and grocery stores, and 2) Typically spend less than $1500 at gas stations and grocery stores every 3 months.

- Chase Freedom and Discover It: 5% back on rotating categories every quarter (up to $1500 per quarter). The analysis here is a bit dicier, as future bonus categories are unpredictable (though the Discover It card does have the 2015 calendar up already). As a result, you can't be sure that you'll be able to fully maximize each bonus. However, if you assume that you can spend the full $1500 each quarter (or $6,000 per year), you'll earn $180 of additional cash back in those categories ($300 on the Freedom - $120 on the Fidelity Amex). Thus, in order to break even, you would need to spend $18,000 in non-bonus categories every year. If you spend more than that, the Fidelity Amex comes out ahead. Anything less than that pushes the Freedom and/or Discover It in front.

Foreign Transaction Fees The Fidelity Amex only charges 1% for transactions made outside the U.S. This puts it ahead of Chase Freedom, Bank Americard Cash Rewards, and Citi Double Cash. However, both the Capital One Quicksilver and Discover It cards waive foreign transaction fees entirely. As a result, if you travel internationally and plan on using your card, you'll need to make sure that the additional rewards on the Fidelity Amex covers the fees incurred abroad.

For the Capital One Quicksilver, this calculation is straightforward. You earn 1.5% on all purchases, both within and outside the U.S. The Fidelity Amex offers 2% cash-back in the U.S., but only 1% internationally (factoring in the foreign transaction fee). As a result, your break even point is when your U.S. purchases equal international purchases. If you spend more money in the U.S., the Fidelity Amex comes out ahead. If you spend more abroad, the Capital One Quicksilver comes out ahead.

The Discover It is a little more challenging. Since you earn a standard 1% cash-back on purchases at non-bonus categories, this is equal to the cash-back earned when using the Fidelity Amex abroad. As a result, if you spend even $1 in the U.S., the Fidelity American Express offers the better return. However, this ignores the rotating quarterly bonus categories on Discover It, so be sure to factor those in.

OVERALL CONCLUSION The Fidelity American Express is a solid product, and as an existing Fidelity account holder, I have been eyeing the card for a while. However, there are a few changes that would make this card much more attractive:

- A sign-up bonus that at least matches other top cash-back cards;

- Some type of earning bonus (like an extra 1% for purchases beyond $10,000, bonuses on travel purchases, etc.);

- The ability to receive cash as a check or as a statement credit.

The third point is somewhat moot for me (and others out there who currently have an eligible Fidelity account), but it would definitely bump the Fidelity Amex to the front of the pack when it comes to cash-back credit cards. Given the new Citi Double Cash card, it's an option that Fidelity and American Express should consider!

What are your thoughts on the Fidelity American Express?