Analyzing the Barclaycard Arrival Earn Ratio of 2.27% When Redeeming for Travel

Update: Some offers mentioned below are no longer available. View the current offers here.

The Barclaycard Arrival Plus World Elite Mastercard has lowered the redemption bonus from 10% to 5%, read more about the changes here.

Update: Discover Deals is no longer available as of November 1, 2018.

The Barclaycard Arrival's minimum spending requirement to earn the 40,000-mile sign-up bonus has tripled from $1,000 in 90 days to $3,000 in 90 days, and I know that many readers are curious about the card and just why I think it's one of the top travel credit cards on the market.

In fact, when we wrote about earlier this week, there was a lively discussion in comments between a reader named Mr. Cool, who kept insisting that the card's 2.2% return on spending was nothing to write home about since it is just on travel, and other readers who were equally firm about the card being a great value specifically for travel - after all, this is a travel site!

Even if I disagree, I always appreciate a lively discussion, and it got me thinking about just what makes it one of the top travel credit cards out there right now. First, let's discuss the valuation of return on your spending, and then I'll get into the competing cards on the marketplace.

A New Valuation - 2.27% Back

Earlier this week I reposted the Top 10 Ways to Maximize Arrival Miles, but the short of it is, the card earns 2X miles per $1 on all purchases, not just certain categories like the Sapphire Preferred or Premier Rewards Gold Card from American Express. You can then redeem those miles for travel purchases - including airlines and hotels, but also other things like rental cars, train tickets, award ticket fees - at a rate of one cent per mile and get a 10% mileage refund (note, straight up cash-back or merchandise redemptions are at a significantly lower rate of about 0.5 cents per mile). In effect, you are spending 90 miles per dollar on travel purchases instead of 100 miles per dollar.

Doing the simple math, it would seem as if your per-dollar return on spending is just over 2.2% thanks to the earning rate and mileage refund (100 cents divided by 90 miles). However, the way you redeem Arrival miles (which I'll show below) is to actually make that purchase and then redeem your miles for a statement credit (within 90 days) on that purchase. The thing is, you're actually also earning Arrival miles on your travel purchase at the usual rate of 2X miles per $1 before redeeming points for it. So in effect, by subtracting the 2X miles per $1 from you redemption total, you're only using 88 miles per dollar - a redemption rate of 1.136 cents per mile. And since you're earning 2X miles per $1, you are in actually getting a return-on-spending rate of...2.27%. Now that extra .07% isn't enough to move the dial significantly, but every point counts, and it ups the rate of return on this card to be even more competitive compared to other fixed-value travel credit cards.

Because Arrival miles are fixed-value points, you can pretty much use them like cash for any travel expense, so there are no blackout dates like with regular award miles or hotel points. Plus, when you redeem Arrival miles for airfare and hotels, you generally earn airline miles and points on those flights since you are paying for them with a credit card and then getting reimbursed using points after the fact just as if you were actually purchasing them. Plus, if you have elite status you can still enjoy your elite benefits such as possibly getting upgraded.

All those are great reasons to keep a premium fixed-value card like the Arrival in your wallet as a way of diversifying your points portfolio and leveraging the different kinds of points you accrue as you maximize your travel rewards.

A Quick Comparison

But I still wanted to answer the question of whether the Arrival truly is among the best travel credit cards. Here are the other cards that I see as its competitors and their pros and cons in comparison to the Arrival.

Capital One Venture

Pros: 2X miles per $1 on all purchases, 2% return on spending including for non-travel cash back.

Cons: Sign-up bonus only currently 20,000 miles (half that of Arrival), Capital One pulls credit scores from all three bureaus

Capital One Spark Cash for Business

Pros: 2% cash back

Cons: Business credit card, so you might not qualify without a small business; sign up bonus of $500 after $4,500 spent within the first 3 months

Fidelity Investment Rewards American Express

Pros: 2% back on all purchases, $0 intro annual fee for the first year; then $59 after that

Cons: Must have a Fidelity account, no sign-up bonus

Discover It

Pros: 5-20% cash back when shopping through Discover portal, no annual fee

Cons: Presently no signup bonus, 1% cash back on most purchases

US Bank Flexperks Visa

Pros: Up to 2% cash back on airline redemptions

Cons: Sign-up bonus is 20,000 points when you spend $2,000 in first four months (might be higher with Olympics promotion), must hit certain ticket price thresholds to get full 2% value from points

Read full review here.

So not only is the Arrival's 2.27% return on travel spending better than many of its competitors under most circumstances, but its sign-up bonus is also higher, and that's hands-down a good deal since it's worth about $454 toward travel.

That said, I firmly believe that whether a credit card is right for you comes down to your personal preferences and plans to maximize it - there are a lot of factors involved, and you're the only person who can truly decide whether or not to get a credit card. However, I still stand by the Arrival as one of the top travel credit cards out there thanks not only to that sign-up bonus, but also because of other benefits like its World Mastercard perks and more.

In the meantime, you can read my post on Maximizing Cash Back Credit Cards, and here's a quick reminder on how to redeem your Arrival miles.

How to Use Arrival Miles

With the Barclaycard Arrival card, you log into your account on barclaycardus.com.

Then click on "Manage Rewards."

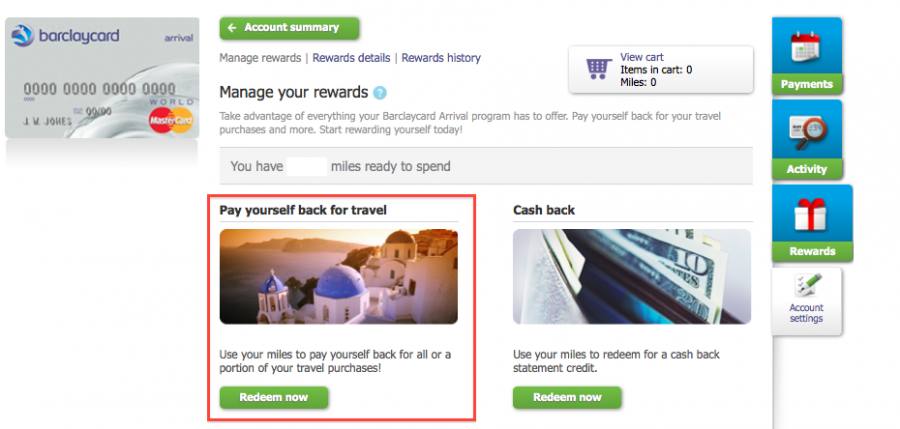

That will take you to a screen with a few different options, but the one you want is: "Redeem Now" line that says "Pay yourself back for travel."

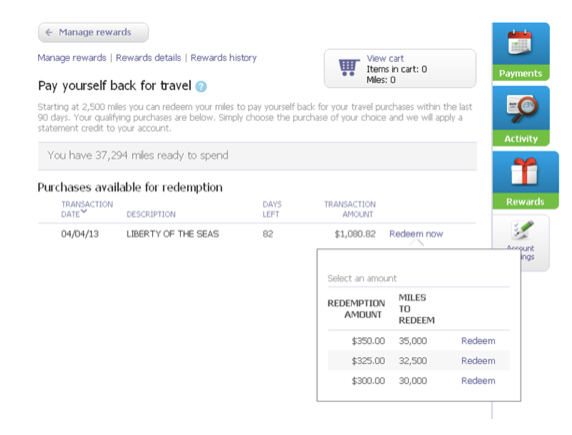

That will send you to the next step which explains that starting at 2,500 miles you can redeem your miles to pay yourself back for travel purchases from within the last 90 days. This also means that even if you don't have enough points to cover the full expense of a charge, you can still cover a portion of it in 2,500-point ($25) increments. The statement will also show you how many days you have left to redeem points for each charge.

Below that will be listed all the "Purchases Available For Redemption" from your statements within the last 90 days along with how many points each one will require. These purchases will fall under the travel merchant category code Barclaycard assigns merchants. Although whether a merchant is included in the travel category will vary depending on the specific vendor, in general, these categories include:

Airlines

Travel Agencies and Tour Operators (including online agencies such as Expedia and Priceline)

Hotels, Motels and Resorts

Cruise Lines

Passenger Railways

Car Rental Agencies

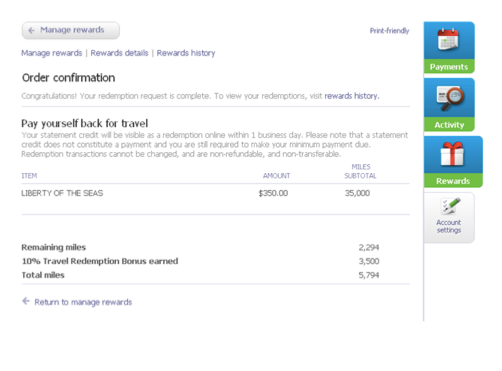

You then add the charge to your "cart," confirm your order and then the final screen will show you what your 10% points refund will be.

Credits take 1-2 weeks to post after you redeem and the 10% mileage refund on travel redemptions also takes about 1-2 weeks to post and be credited back into your account.

As I mentioned, using Arrival miles is basically just paying for a travel purchase as usual with your Arrival card and then requesting a statement credit for it - so in general, you still earn miles, hotel points, elite credit, etc., on your travel just as you would if you were paying cash, all of which increases the Arrival's value proposition even further in my estimation.

If you're thinking about making the Arrival one of several cards you get in a round of applications, here are my other picks for the top current travel credit card offers.