Why You Should Care About the Apple Card, Even If You Aren't Getting It

Yesterday, Apple unveiled a slew of new subscription services that will let you read the news, play video games and watch documentaries produced by Oprah. The company also wants you to pay for all that content using the Apple Card.

Basically, the event showed that Apple wants your eyeballs and your money. Plenty of TPG readers weighed in with less-than-excited comments about the card, which will be available this summer. "Snooze," "Hard pass" and "honestly, has no use to me" can sum up the attitudes of the savviest points-hungry readers, and I'll admit that I initially shared the level of indifference to the news. However, I think Apple will do more than get people who love Apple to applaud at its event with this product.

While I do not agree with Apple CEO Tim Cook's belief that Apple Card will be "the most significant change in the credit card experience in 50 years," my perspective has changed. There are some crucial reasons why Apple's entrance to credit cards will create positive changes for all of us.

Instant Rewards Impact

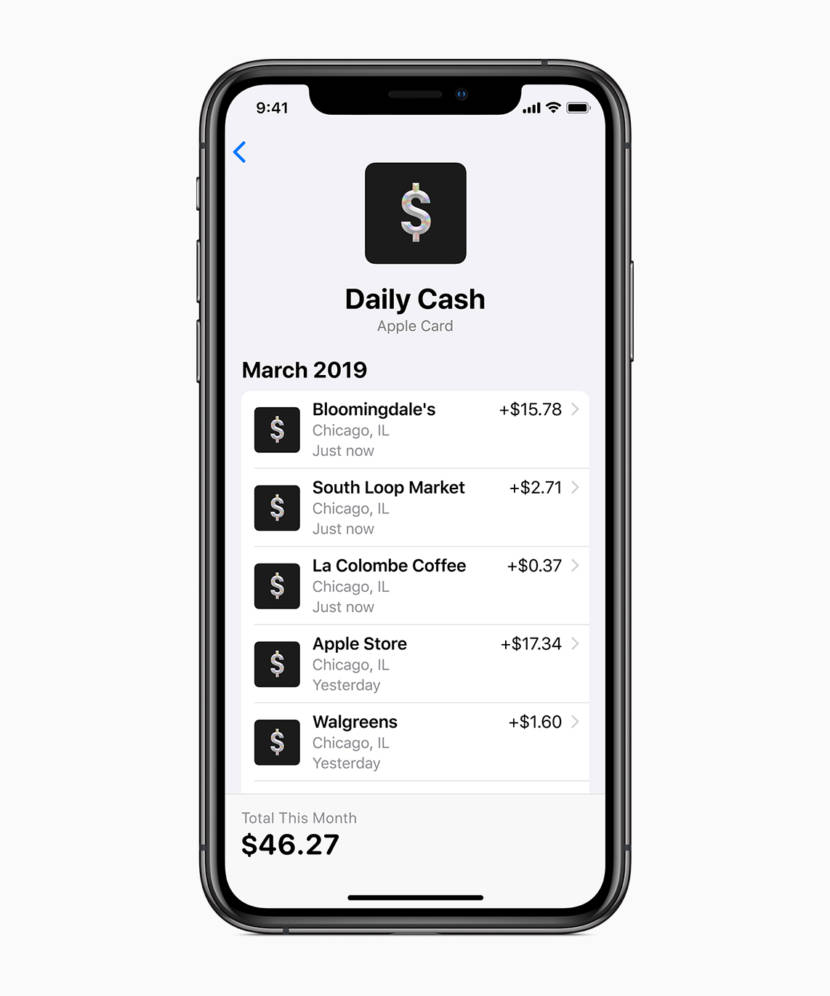

The Apple Card's Daily Cash offer is built for the era of instant gratification. Rather than waiting until the end of a billing cycle to post accrued monthly earnings, customers who use Apple Card will see cash back totals on a daily basis. Imagine if other cards decide to copy Apple's approach and issue points on a more frequent basis. For customers in need of a small amount of additional rewards points, the immediacy of posting a reward can make the difference of capturing a great deal or letting it slip away while waiting for a monthly rewards total. I would love to see Chase start posting Ultimate Rewards points on a daily basis.

Lowering the Bar for Fees

The Apple Card seems to want to occupy the most consumer-friendly position in the credit card landscape when it comes to fees. The absence of late fees and foreign-transaction fees could push more competitors to embrace a zero-fee approach to their most basic offerings and expand the list of cash-back cards with no foreign transaction fees. And Apple's aim to offer the lowest interest rates in the industry is good news for anyone who is guilty of carrying a balance on their credit cards.

Pushing Privacy

Most banks don't just make money from fees and finance charges. They profit from your personal information, too. Consider Bank of America's US consumer privacy policy, which details the many ways it puts information about a customer's creditworthiness and his or her transaction history in the hands of a wide range of other companies. Spoiler alert: Other banks such as Chase and Citi have nearly identical policies.

Apple said that Goldman Sachs, its partner for the card, will not share or sell data to third-party companies. If you're looking to limit how many companies know how much you spent at the bar last weekend, Apple seems to be setting an example for the banking industry.

Beyond keeping your information away from third parties, the Apple Card appears to set a new standard for credit card fraud protection. The physical card has no card number, no CVV, no expiration and no signature — just your name and a chip. To access those card numbers when making a purchase online, card holders will need to pull up their card in the Wallet app. Additionally, the Apple Card features a "one-time unique dynamic security code" that changes after each purchase you make, adding another layer of protection against fraud.

Apple's rewards structure won't attract interest from anyone carrying premium credit cards. The 3% on purchases made with Apple/2% on mobile purchases/1% on purchases made with the physical card deal can't compete with 5x points with airlines, lounge access, complimentary WeWork access and the other lucrative offers that swirl in the high-end credit card landscape. But the company could prove to be a difference-maker in the way that credit card companies approach entry-level card holders.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.