Major FICO changes could be bad news for your credit score

Editor's Note

Editor's note: This post has been updated with new information.

The way FICO scores are calculated is changing pretty dramatically, and it could lower your credit score.

Fair Isaac Corporation — more commonly known as FICO — announced it will score consumers more harshly based on their debt levels and loan payments starting this summer. The purpose of this change is for FICO to be able to more accurately calculate the risk of a consumer to lenders.

New to The Points Guy? Want to learn more about credit card points and miles? Sign up for our daily newsletter.

While the changes are set to take place during summer 2020, consumers likely won't see changes, if any, to their credit score until summer 2021 or later. That's because the new reporting version is released in phases. This summer, the credit bureaus will adopt the new version as a part of phase two, but it could take a year or longer before phase three — when lenders adopt the change — is initiated.

What is the new scoring system?

FICO 10 T — the new reporting version — will place a greater weight on missed payments, meaning that consumers who have fallen behind on repayments will likely see a drop in their credit score. On the plus side, consumers could see a credit score increase if a delinquency is over a year old.

The Wall Street Journal reported that "FICO updates its scoring model every few years to reflect changes in consumer borrowing behavior and performance. When it last announced such changes, in 2014, they were viewed as likely to help boost consumers' credit scores."

Related reading: How to improve your credit score

FICO will reportedly flag certain customers who sign up for personal loans. That could ding you if you transfer credit card balances and then rack up more credit card debt. They'll also continue a recent industry trend of including information from bank account balances and utility payments.

Related reading: 4 incorrect assumptions about your credit score

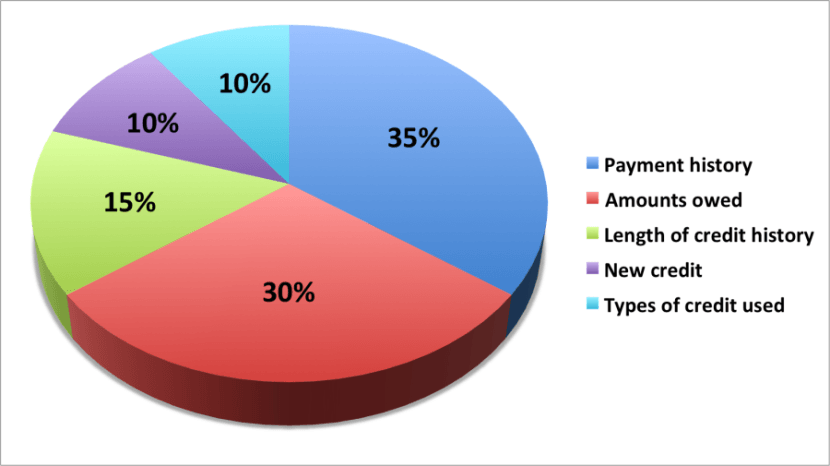

In the fourth quarter of 2019, the Federal Reserve reported that that U.S. consumers had accumulated $930 billion in debt. This may help explain why FICO made adjustments to its scoring model, although the five factors it considers will remain the same.

"Unlike previous FICO scores, 10 T will assess how consumers' debt levels have changed during the past two or so years. FICO scores so far have reflected consumers' balances during roughly the most recent month tracked. This change will place more weight on rising debt levels. Consumers who previously paid their credit-card bills in full but shift to carrying growing balances for several months will likely end up with a lower score," reported AnnaMaria Andriotis of The Wall Street Journal.

That said, not all lenders will adopt the new scoring systems.

What does this mean for you?

If you have and continue to follow the first commandment of travel rewards cards — thou shalt pay thy balance in full — then you shouldn't have too much to worry about.

Related reading: 5 ways to improve your credit score

The new version of FICO will most notably affect borrowers who have been carrying balances over the past 24 months. FICO estimates that roughly 110 million consumers will see a change to their credit score. Of those, approximately 40 million consumers should see an upward shift over 20 points, while another 40 million will see a shift downward.

However, given the current economic situation due to the coronavirus pandemic, you may be carrying more balances than you had prior.

If you find yourself in this situation, you can call your lender or credit bureau and ask that a "natural disaster code" be applied to your credit report. This is by no means a cure-all solution — nor will it protect your credit score — but it will protect your VantageScore (the complimentary credit score you can see through programs such as Chase's Credit Journey) from any delinquent reporting being added to your account.

Related reading: 5 ways the global recession is affecting credit cards and banks — and the upside for some cardholders

In the meantime, FICO is encouraging credit holders to practice credit vigilance. This is something that you should always do, but here's your reminder on how important it is.

Bottom line

If you've been a responsible borrower, then this new model will likely improve your credit score. However, if you've been carrying a balance, it's time to bring your bills up to date.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.