How Your Utility Bills Might Improve Your Credit Score With Experian Boost

In the world of credit scores, things don't generally change at a fast pace. Yet every once in a while, a big announcement will be made that causes lenders and consumers alike to sit up and pay attention. Most recently, that announcement came in the form of a new service called Experian Boost.

Why Experian Boost is a Big Deal

New credit reporting policies and new credit scores are introduced from time to time. In truth, they aren't always that exciting.

Despite updates and changes, the basic credit reporting and scoring process has worked the same for around three decades, since the FICO score was introduced at Equifax in 1989.

- Step One: Creditors report your account history to the credit bureaus.

- Step Two: The bureaus use the information to create credit reports.

- Step Three: Lenders buy those reports (and a credit score add-on) to evaluate your creditworthiness when you apply for new loans, credit cards and services.

Experian Boost is a big deal because it makes groundbreaking changes to step one of this 30-year-old process. For the first time in credit-reporting history, you have the option to add account information to your own credit report.

How Experian Boost Works

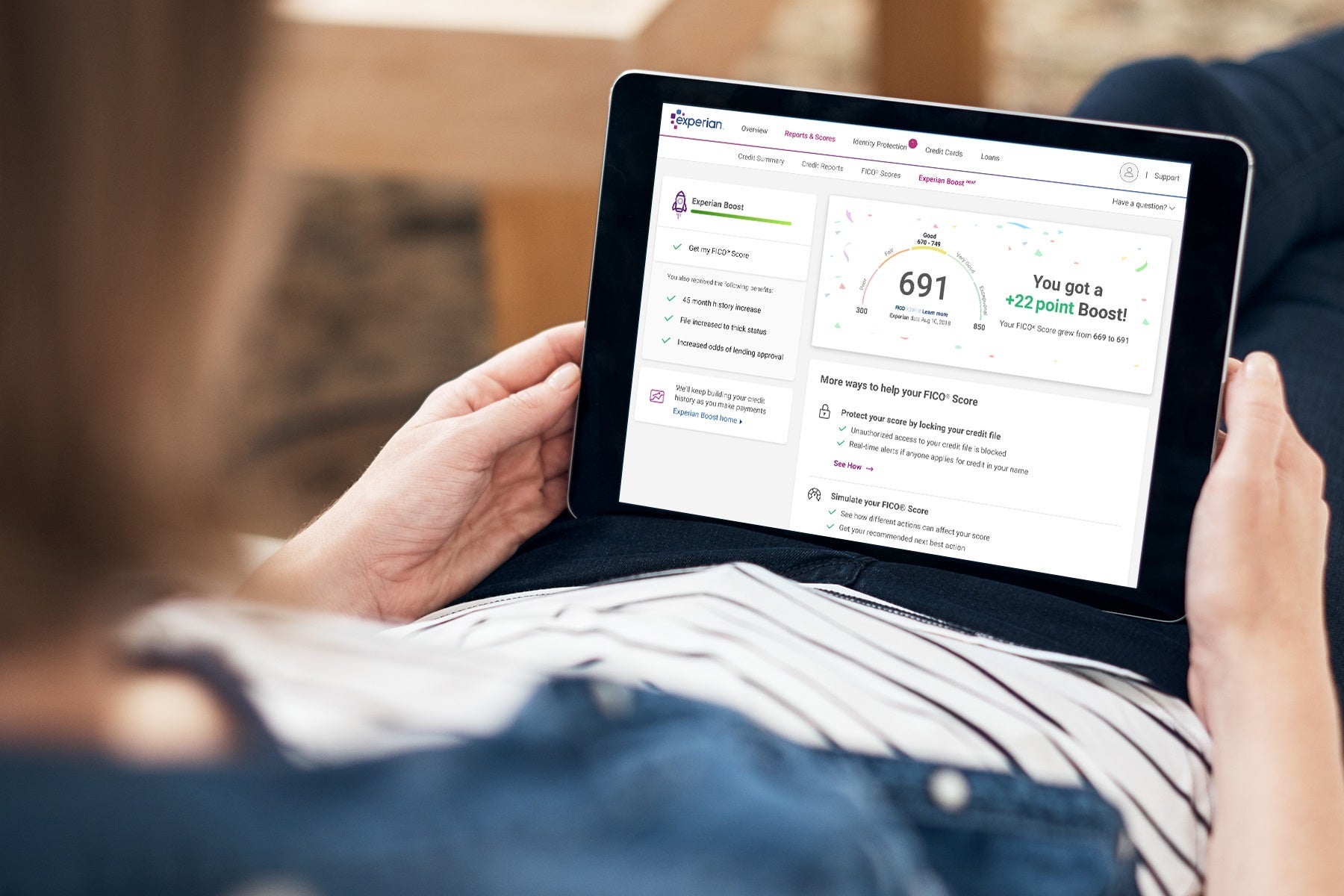

Experian Boost is an opt-in service that allows you to voluntarily add utility and mobile phone payment history to your own credit report.

This is a big departure from the credit-reporting status quo. Historically, the credit bureaus only allowed companies approved as data providers (e.g., lenders, creditors, collection agencies, etc.) to submit information to be included on your credit report.

To add utility and mobile phone history to your Experian credit report, you will need to follow these three steps.

- Visit the Experian website to connect the bank account (or accounts) you use to pay your utility and mobile phone bills. You'll have to supply your bank account username(s) and password(s) and other personal information as part of the sign up process.

- Pick the accounts you want to add to your report and skip over any you don't want included. Boost will scrape your bank account(s) for payment data and show you which accounts are available to add to your report.

- See immediately whether or not Boost improves your score.

Pros and Cons

Opting in to use the service is simple enough, but you probably need a little more information to decide whether it's right for you. Here's a look at some of Boost's pros and cons to help you decide.

The Pros

- Experian Boost is free.

- There's a chance the service could increase your Experian credit score, especially if you have a thin credit file (aka not a lot of credit history).

- Boost works with both FICO (FICO 8 and 9) and VantageScore (3.0 and 4.0) credit-scoring models.

- Boost will only add positive utility payment history to your credit report. The service bypasses any derogatory data.

- If you change your mind, you can remove the utility data added to your report via Boost at any time.

The Cons

- You must consent (and provide your login credentials) for Boost to access your bank account. While there's nothing to suggest that the service lacks top-notch security, handing over sensitive data in an age where data breaches and fraud are so prevalent can't be taken lightly.

- Even if you opt in and positive information is added to your credit report via Boost, there's no guarantee of a score increase.

- Positive utility data is only added to your Experian credit report.

- If a lender pulls an Equifax or TransUnion report (or a score based on this data), Experian Boost won't help you.

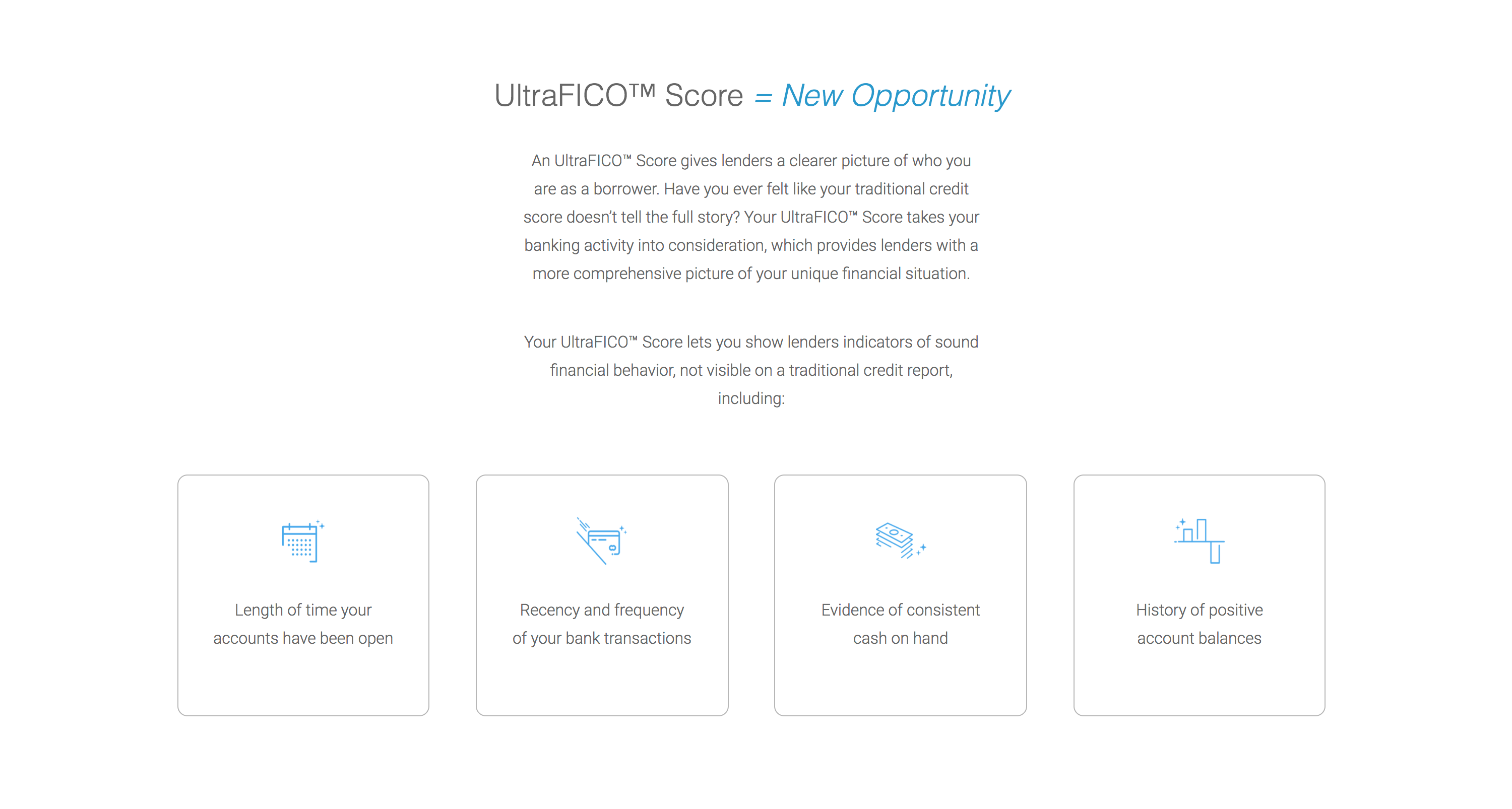

Experian Boost vs. UltraFICO

If you've been paying attention to the news lately, you may recall another new credit score announcement: UltraFICO.

UltraFICO is another type of credit score enhancement service which launched in 2019 (though only as a small pilot program until mid year). UltraFICO is also an opt-in style service that lets you give permission for data from your bank account to be considered in your credit score.

In the case of UltraFICO, it's your banking data itself (e.g., account history, historical balances, etc.) that could have an influence on your credit score. However, UltraFICO falls short of actually adding positive data to your credit report.

Additionally, UltraFICO only works with FICO 8 and FICO 9 credit scores at Experian. Boost, by comparison, could benefit any credit score (based on an Experian report) that considers utility accounts.

Focus on What Matters Most

Remember, good credit scores could easily save you thousands of dollars per year. It's well worth the effort it will take you to achieve and maintain a good credit rating.

Experian Boost and UltraFICO do show some encouraging signs of more consumer control over credit scores. Yet that doesn't change the fact that the traditional information on your credit reports remains the most important. If your credit reports have late payments, Boost isn't going to erase them. If your reports show high credit card balances month after month, Boost isn't going to offset those high credit utilization ratios.

Experian Boost might help your score some, but it isn't a magic wand. You'll still need to follow sound credit management habits. That's the only way to earn and keep the good credit scores you need to get loans, credit cards and even insurance premiums at affordable prices.

Of course, if Experian Boost can give you a little bit of an edge on one of your credit scores, it might be a good idea to throw that into the mix as well. If you get lucky and improve your score with Boost, it certainly couldn't hurt.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.