My Experience Filing a Consumer Financial Protection Bureau Complaint

USAA Federal Savings Bank has repeatedly provided outstanding customer service experiences for the 10 years I've done business with them. However, over the last few weeks as I was in the process of buying a house, I found a mistake on my Comprehensive Loss Underwriting Exchange (CLUE) report that had been made by USAA. The CLUE report is not compiled by USAA, but rather by LexisNexis based on information from public records, banks and other third-party sources, and it's reviewed by most insurance companies when they're considering writing a policy.

Despite multiple attempts, I couldn't get USAA to remove its errant entry from my CLUE report, nor would the issuer give me any direction on how to fix it myself or even offer an apology or conversation on how to move forward. Therefore, I had little recourse except to file a complaint with the Consumer Financial Protection Bureau (CFPB) with the intention of escalating the issue higher within USAA to get the right eyes on my problem. Today, I'll share my experience going through the process.

The Mistake

In May 2016, I was commuting to work on a rather nice Cannondale bicycle. One day when I returned home from work, I left the bike in front of the house instead of putting it in the garage as I usually did. When I came outside the next morning, the bike was gone, which was rather surprising as we were living on a military base and theft wasn't something we typically had to worry about.

I called USAA to inquire about the possibility of my renter's insurance covering the replacement cost of the bike. The bank said it would be possible and to call back if I wanted to file a claim. The next day, after a post on the neighborhood Facebook page, my neighbor came scrambling over, bike in hand, apologizing that because it also happened to be trash day and the bike was out front, he thought I was throwing it away. I called USAA back to let them know the bike was returned and we obviously wouldn't be filing a claim, and went on my way.

Fast forward two years to today, where I'm in the middle of closing on buying a house. During the homeowner's insurance shopping process, I didn't understand why I kept receiving rather pricey quotes back from almost any company I queried. I finally found out that USAA had filed a claim on my renter's insurance policy from May 2016 for theft, which made me ineligible for a claims-free discount from any insurance agency.

After a week of back and forth with USAA, the bank admitted its mistake and removed the claim from its internal reporting. However, the front-line phone reps didn't know how to fix the negative mark on my CLUE report, which was what all the other insurance companies were seeing that caused my quotes to be so high. USAA gave me no direction, never apologized, made me repeat my story five times over several hours on the phone and ended every call with no resolution or direction towards resolution. Twice I was promised a supervisor would call back before the close of business, but after never receiving a return call and not wanting to spend additional time diving into the LexisNexis correction process, I had little knowledge of what else to do except file a CFPB complaint.

Filing a Complaint

The CFPB is a government regulatory body which exists in its own words to...

"...make consumer financial markets work for consumers, responsible providers, and the economy as a whole. We protect consumers from unfair, deceptive, or abusive practices and take action against companies that break the law. We arm people with the information, steps, and tools that they need to make smart financial decisions."

There's been plenty of talk in today's political world that the CFPB has little power and serves little purpose. But as far as filling out a complaint and getting a response from a financial institution, it's still very effective in my experience.

The process to file a complaint really couldn't be easier, which is a bit surprising for a government regulatory organization. The website is user-friendly and walks you through a very simple process. Head to the CFPB complaint website and make sure you have all your information and any documentation that helps to tell your entire story in digital form.

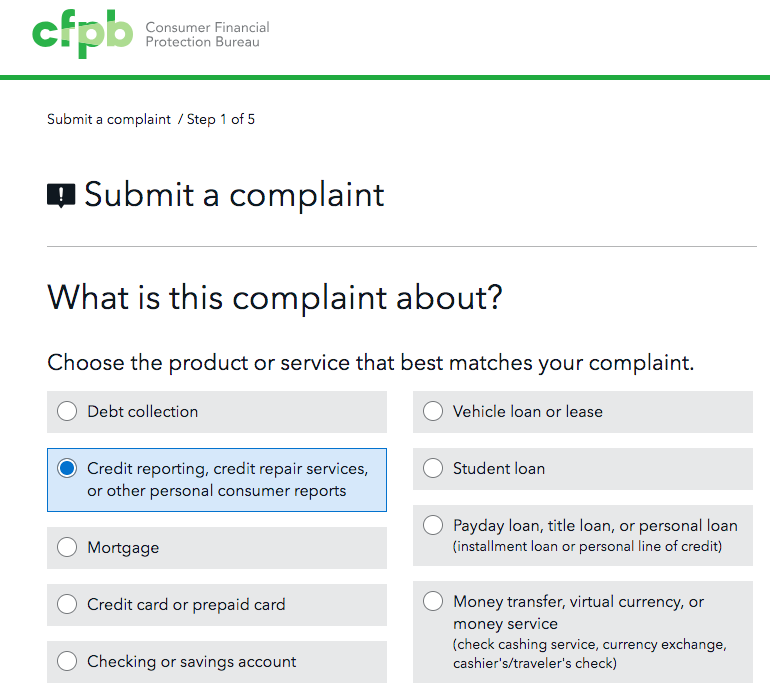

The website will first ask what your complaint is about...

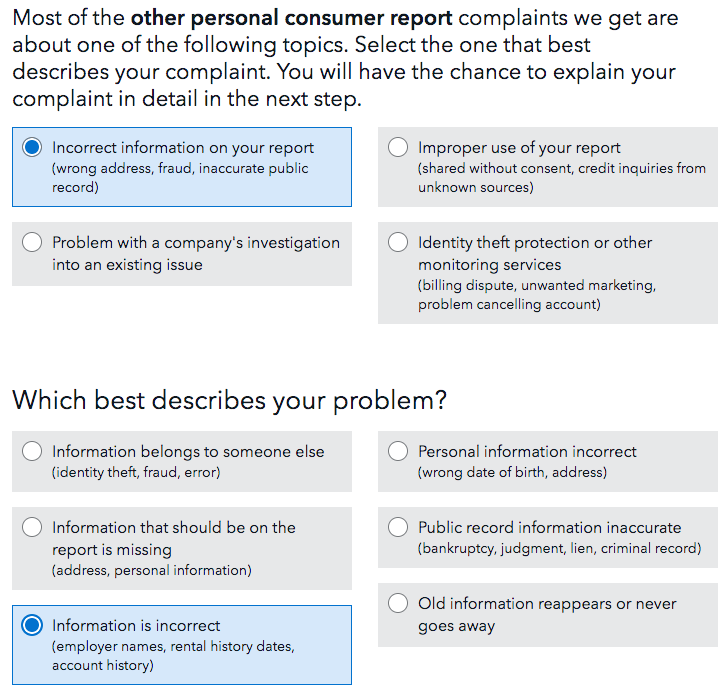

In this case, the "other personal consumer reports" option seemed to best fit my complaint. The next screen gets a bit more specific as to the exact nature of your problem. I selected what seemed to best fit my circumstance with the LexisNexis-generated report:

After selecting your general issue, it's time for the narrative. The best thing you can do here is to stick to purely factual statements. Be as specific as possible, including timeframes and names of people you dealt with, leaving all emotion out of the narrative and uploading any documentation you have which supports your complaint. You then also have the option to write what a favorable outcome would be.

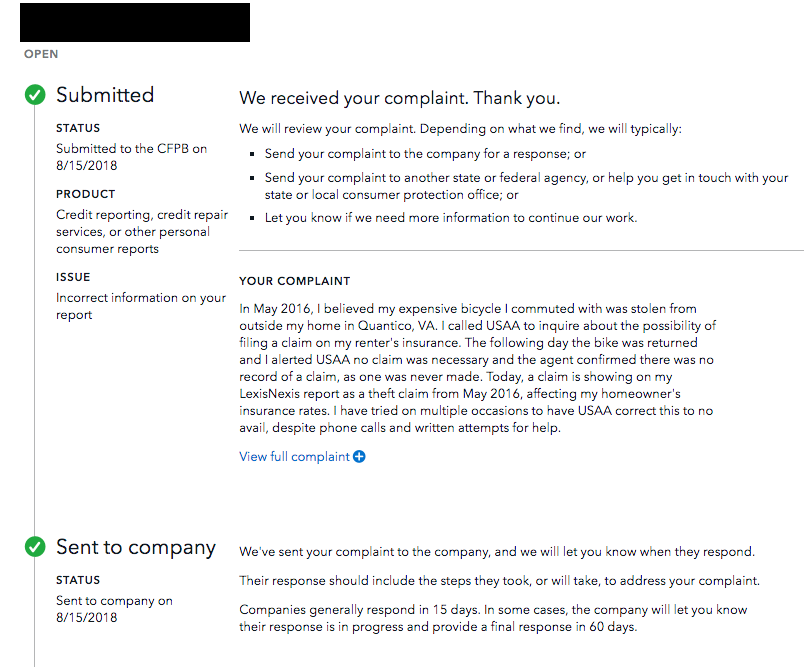

The last step is to select the financial institution that should receive the report, and then you're done. The CFPB says companies typically respond within 15 days of receiving a complaint. In my experience, it was much quicker for an initial outreach, but they do ask for time to investigate the case.

You can review your complaint and its status anytime under your CFPB log-in. The company's response will also appear there once it's been submitted.

A reminder that CFPB complaints are not customer service complaints. There needs to be a regulatory, criminal or discriminatory act in order to file a complaint.

The Resolution

Only two hours after I submitted my complaint, someone from the USAA CEO's office reached out to me via a phone call. The person told me the bank had received my complaint, assigned a case manager and requested I give them 48 business hours to review and investigate it.

A few days later, I received a call from the assigned case manager, who laid out the situation. Unfortunately, I find myself in a type of loophole where USAA cannot fix its mistake. Because of privacy issues, USAA cannot contact LexisNexis to fix the report on my behalf. In fact, USAA cannot even see any record of the bogus claim because it was removed from their own internal claims experience report. In the end, I had to reach out to LexisNexis, wait on hold for 30 more minutes and begin the 30 day process to have them reconcile the report with USAA.

Bottom Line

The truly frustrating part of all of this — besides all of my past and future time wasted — is that right now I can only afford to buy homeowner's insurance from USAA because USAA is the only one who will give me a claims-free discount since their own systems cleared the error. USAA's mistake and inability to fix it has in fact locked me into doing more business with them. The investigative agent from USAA had no avenue to give me compensation of any kind for my wasted time, and as far as I could tell, based on the tone of the call and because the company had no further record of the bogus claim once it had been removed from their internal system, the agent may have not believed me in the first place.

The CFPB complaint did elevate my issue to someone empowered to take as much action as possible, and it's very easy to complete, so I highly recommend taking advantage of the process if your attempts at rectifying a situation directly with a bank have failed. It's unfortunate such a situation exists where a bank cannot fix its own mistake and the burden falls on the consumer. I hope to have my CLUE report cleared in the next month, at which point I'll be shopping for other insurance providers.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.