Debunking credit card myths: Does having many credit cards hurt your credit score?

Editor's note: This post has been updated with new information.

We talk about travel credit cards quite a bit here at TPG. Applying for and using these cards strategically can unlock incredible travel experiences such as premium class flights or luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, and these can stand in your way of not only fantastic rewards but also an excellent credit score.

Today, we're debunking an important myth that involves the number of credit cards you have.

Want more credit card news and advice? Sign up for TPG's daily newsletter

Myth: Having many credit cards will hurt your credit score

At the time of publication, I have 22 open (and active) credit cards. This number strikes many of my friends and family members as off-the-wall, and the most common comment I get is, "Aren't you worried about what all of those cards will do to your credit score?"

Related: Yes, I have 22 credit cards; here's why

In reality, I'm not worried about what they do to my score. Instead, I am enjoying the boost they have on my score.

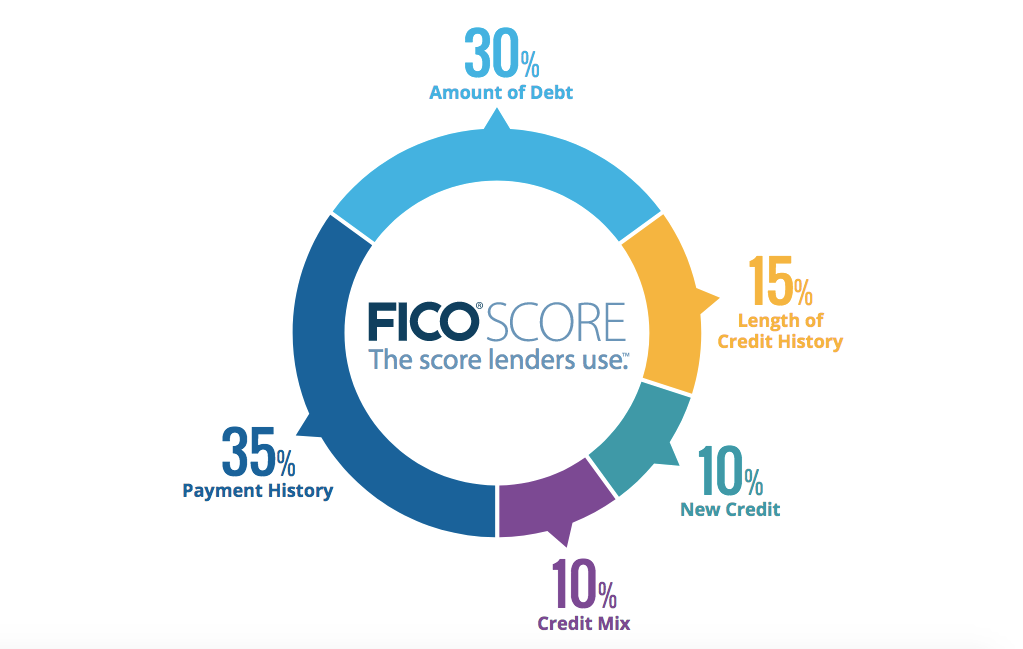

In order to debunk myths surrounding credit cards, it's essential to understand the different factors that contribute to your FICO score, the one most frequently used to determine your creditworthiness for any new line of credit:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

However, not all factors are treated equally, and these five are weighted based on how important they are to your score:

When it comes to opening a large number of credit cards, it's the two most important factors that come into play: payment history and amounts owed.

Related: How credit scores work

Payment history

The single biggest factor in your FICO score is your payment history, which covers any type of credit or installment account linked to your name. While one or two late payments won't completely ruin your score, it can have a negative impact.

So how does having multiple credit card accounts help this factor? It all comes down to painting a positive picture of your overall credit — and MyFico.com even points out that having multiple accounts with no late payments is a positive.

For example, let's say you have a single credit card and were late on two or three payments several years ago. Even though you've made up ground by paying on time ever since, you're still 0 for 1 when it comes to accounts showing a late payment. If you add new cards to your wallet and aren't late on any payments, you now have accounts with unblemished records. This may not move your score from 500 to 700, but in the long run, it's an undoubtedly positive pattern.

Amounts owed

The second most important factor in your FICO score is the amounts owed, commonly referred to as your credit utilization rate. This looks at how much of your credit you are actually using and is typically expressed as a percentage. Here's the calculation:

Total balance on your account(s) ÷ Total limit of accounts = Utilization

Keeping this number low shows issuers that you can effectively manage your credit lines and aren't at risk of over-extending yourself.

Let's say that you typically have a $2,000 balance on a credit card (paid off in full each month, of course), and your single card has a $10,000 limit. You thus have a utilization rate of 20% ($2,000 ÷ $10,000).

However, if you apply for another card and get another $10,000 of credit, you are now spreading that $2,000 balance across double the available credit. Your utilization drops to 10%.

Let's extend this math out to even more cards with that same $10,000 credit limit and the same $2,000 in monthly spending:

- Three cards: $2,000 ÷ $30,000 = 6.67%

- Four cards: $2,000 ÷ $40,000 = 5%

- Five cards: $2,000 ÷ $50,000 = 4%

My cards have a huge amount of available credit on them (over $300,000), but my utilization rate regularly hovers around 2%. I don't spend more on the cards just because I have them. What I am spending is just spread out across a broader credit line, helping my utilization rate and thus improving my credit score.

All that being said, it's important to note that there are situations where having too many credit cards can impact your credit score. Spending beyond your means (and not paying your balance in full) is a quick way to wreck your score, and adding untrustworthy authorized users can also have a negative impact. Remember too that you should do everything possible to avoid missing payments.

Related: Ten commandments for travel rewards credit cards

Bottom line

There are many myths about credit cards out there, and a common one relates to the perceived negative impact that multiple accounts can have on your credit score. In reality, the opposite is true, as almost two-thirds (65%) of your FICO score is determined by factors that can actually be enhanced with additional accounts. As always, be sure that you aren't over-extending yourself, as this myth can easily come true given the right (or wrong) environment.

Additional reporting by Benét J. Wilson

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening. Plus, a $250 Capital One Travel credit to use in your first cardholder year upon account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- LIMITED-TIME OFFER: Enjoy $250 to use on Capital One Travel in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app