Debunking credit card myths: Does paying off accounts with negative marks help your credit score?

We devote a lot of coverage to travel rewards credit cards here at TPG.

When you sign up for new cards and then utilize them strategically at various types of merchants, you open up the ability to redeem your points and miles for things like first-class flights and luxurious hotel rooms. However, there are a number of misconceptions out there when it comes to credit cards, so today I'll continue our new series that debunks these myths and allows you to begin planning for your next vacation.

Let's consider an aspect of your financial profile that seems like it should have an impact on your ability to be approved for a card.

Myth: Paying off accounts with negative marks immediately helps my credit score

Statistics show that roughly four out of every 10 Americans are in credit card debt. I have several friends who admit that they didn't think too hard about swiping their cards during college or immediately after entering the workforce, and they are now paying the price. These accounts have been open for quite some time, but many of them may have missed or late payments or have even been handed over to a collections agency.

Related: A complete guide to improving your credit score

When you finally reach the point of paying off that account, you may think that you'll immediately see a huge improvement in your credit score. After all, the account is down to a zero balance and may even be closed. Unfortunately, while you may see a slight uptick in your score, the effect is not immediate.

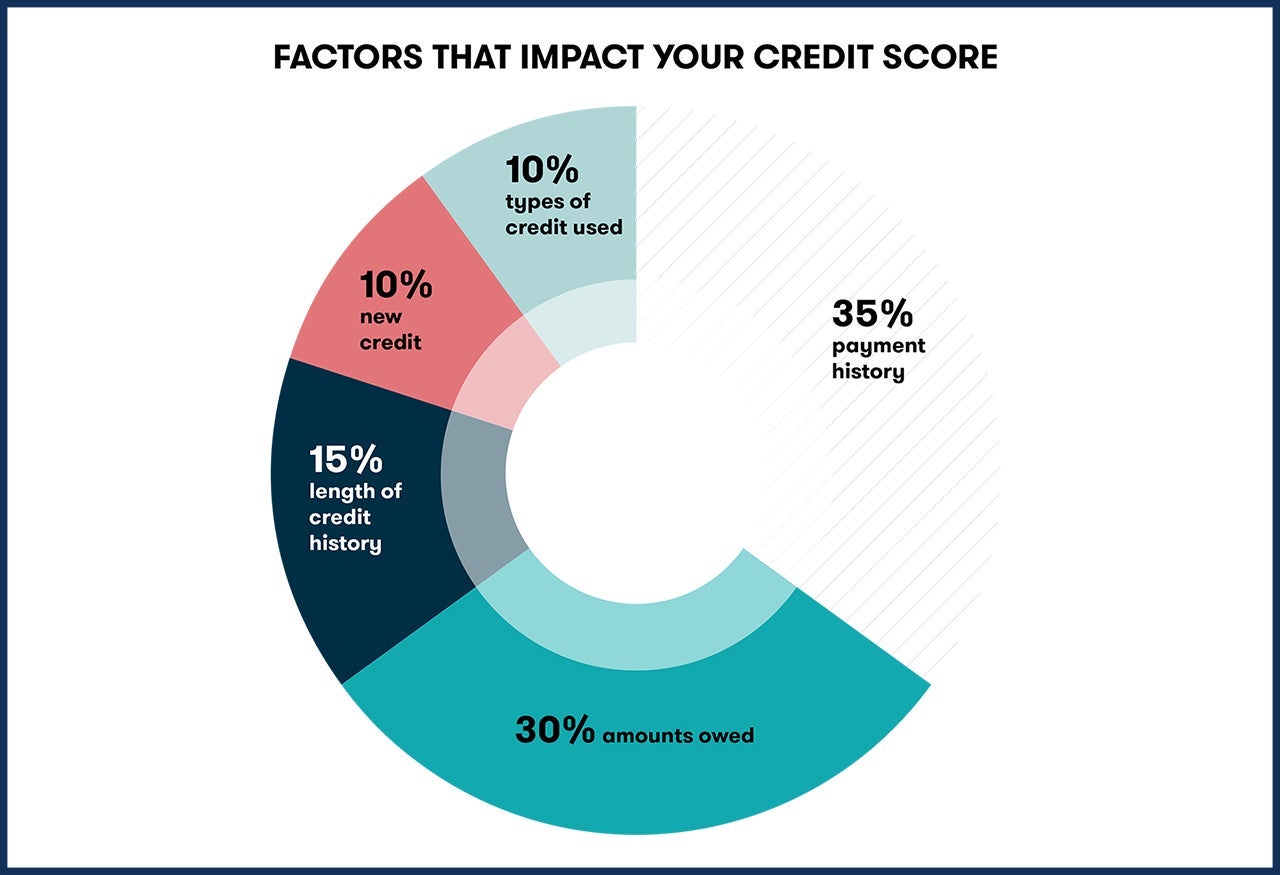

Let's once again revisit the five factors that contribute to your FICO score, the one most frequently used to determine creditworthiness:

- Payment history

- Amounts owed

- Length of credit history

- New credit

- Types of credit used

As discussed previously, these five factors are weighted differently based on how important they are to your score.

The second most important factor (amounts owed, commonly referred to as utilization) clearly improves as you are paying down the outstanding balance on a credit card debt. However, the most important one (payment history) is what can really bite you when it comes to paying down old credit card debts with negative marks like late or missed payments.

There's no way to know exactly how your credit score is calculated, as the three major credit bureaus use their own proprietary formulas (hence why your Equifax score may differ from your TransUnion score). However, all of them use past and present information to make a decision on how you're likely to behave in the future, so this means that negative marks on accounts — even those that have since been closed — can impact your score.

You may be wondering exactly how long it takes for negative information to fall off your credit report, and unfortunately, the answer isn't pretty: For many negative marks (including late payments or collection accounts), you'll need to wait seven years for them to disappear.

Fortunately, you don't just need to sit there and wait it out. The credit bureaus are continually reevaluating your credit history based on all of the five factors listed above, so the more positive actions you can show (like paying your balance in full and on time every month, keeping your utilization low, etc.), the better.

This will indicate to both the bureaus and credit card issuers that you can effectively manage the credit that has been extended to you, making you more attractive when it comes to gaining access to additional credit.

Related: Ten commandments for rewards credit cards

Bottom line

Unfortunately, even when you finally pay off and close an account with late or missed payments or other negative items, it can take up to seven years for those items to disappear and stop impacting your score.

However, even though this takes time, you should continue to manage your credit effectively and could still be approved for some of the top credit cards. Remember that issuers simply want to see positive trends so they know you aren't likely to default.

Additional reporting by Chris Dong.

TPG featured card

at Capital One's secure site

Terms & restrictions apply. See rates & fees.

| 5X miles | Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel |

| 2X miles | Earn unlimited 2X miles on every purchase, every day |

Pros

- Stellar welcome offer of 75,000 miles after spending $4,000 on purchases in the first three months from account opening.

- You'll earn 2 miles per dollar on every purchase, which means you won't have to worry about memorizing bonus categories

- Rewards are versatile and can be redeemed for a statement credit or transferred to Capital One’s transfer partners

Cons

- Highest bonus-earning categories only on travel booked via Capital One Travel

- Enjoy a one-time bonus of 75,000 miles once you spend $4,000 on purchases within 3 months from account opening, equal to $750 in travel

- Earn unlimited 2X miles on every purchase, every day

- Earn 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- Miles won't expire for the life of the account and there's no limit to how many you can earn

- Receive up to a $120 credit for Global Entry or TSA PreCheck®

- Use your miles to get reimbursed for any travel purchase—or redeem by booking a trip through Capital One Travel

- Enjoy a $50 experience credit and other premium benefits with every hotel and vacation rental booked from the Lifestyle Collection

- Transfer your miles to your choice of 15+ travel loyalty programs

- Top rated mobile app