Should You Buy Bitcoin With Your Credit Card?

Update: Some offers mentioned below are no longer available. View the current offers here.

No matter what corner you turn in cyberspace, you're likely to find a headline about Bitcoin. The virtual currency has been a hot topic in the financial industry in recent years, but massive swings in its valuation over the past two months have placed Bitcoin squarely in the spotlight. JPMorgan Chase CEO Jamie Dimon questioned the intelligence of people buying Bitcoin, while Peter Thiel's VC firm has reportedly purchased loads of the currency. The conversation is even extending from computer screens to fried chicken: KFC Canada recently offered a Bitcoin Bucket, available to, you guessed it, people who pay with Bitcoin.

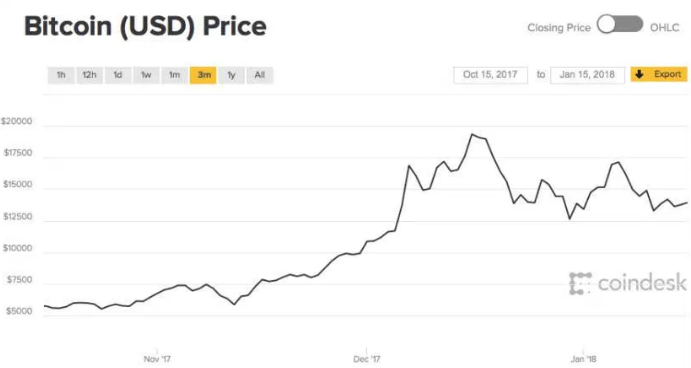

As I started writing this post, one Bitcoin was worth $14,275. That's a massive jump from the valuation in mid-November when Bitcoin clocked in under $6,000. However, it's significantly lower than its high of $19,175 on December 16. All these big numbers are leading many — including me — to ask one question: Should I use my credit card to buy Bitcoin?

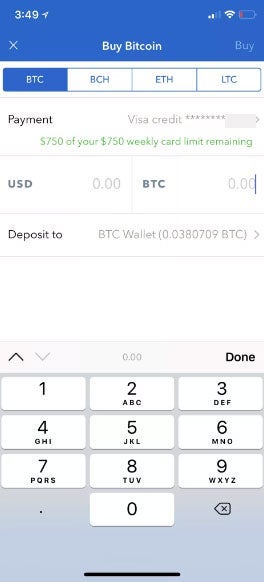

As I was searching for answers, I discovered that TPG's Adam Kotkin had already explored the world of credit card-funded Bitcoin purchases. Using the Chase Freedom Unlimited, he bought $750 of the currency via Coinbase, arguably the most-recognized name among virtual currency exchanges. Adam's purchase was a test to see how the system worked, and he wanted to determine an important piece of information: Do banks treat Bitcoin like a cash advance or a standard purchase?

Luckily, Chase viewed it as a purchase (cash advances are a horrible idea with equally horrible interest rates), and he earned 1,125 Ultimate Rewards points. However, it's important to note that since his test, various reports have come out indicating that pretty much all the major banks are now treating cryptocurrency purchases as cash advances, with all the associated fees.

Even if he wanted to buy more Bitcoin, he couldn't; Coinbase assigned him a weekly limit of $750 on his credit card. According to the Coinbase website, limits for individuals "vary based on the payment method used, your account age, purchase history, and other factors."

One thing that doesn't vary is the conversion fee that Coinbase charges for credit card purchases. At 3.99%, that's quite the additional fee that eats away at the actual virtual currency amount.

Who Else Is Buying Bitcoin With Credit Cards?

Adam isn't the only one exploring the ability to buy Bitcoin with plastic. According to a recent survey of nearly 700 Bitcoin investors conducted by LendEDU, 18% of respondents had used their credit cards to acquire the virtual currency. Some of those virtual currency pioneers made a huge mistake: 22% of them failed to pay off their credit card balances after buying Bitcoin. Failing to pay your balance is foolish at any time, but with Bitcoin there's the additional risk that the currency will decrease in value.

Let's say someone buys $2,000 of Bitcoin on a credit card with an APR of 15% (the current average of all cards), and he carries $1,000 of that as a balance, paying $200 each month. But wait, some of the respondents might say, he can use the money from selling his Bitcoin eventually to pay those changes. In a perfect world, Bitcoin soars, and the small amount of interest is a blip on the earnings radar. However, the world is far from perfect. If the value of Bitcoin drops, the individual has paid $40 in interest charges and lost money from the initial purchase. That's not exactly the winning scenario you might have imagined from the "Bitcoin Hits Record High" headlines.

Where You Can Buy Bitcoin

There are loads of virtual currency exchanges to consider if you're interested in betting on Bitcoin. Warning: You may wait a while. As more people explore options for buying the currency, some of the most popular exchanges are struggling to accommodate increases in web traffic. For example, Coinmama currently greets visitors with the following disclaimer: "We're currently under heavy load. Every verification and support request will be answered, but we may need some time to get back to you."

Daily spending limits vary based on a range of factors that can include your purchase history, so your first Bitcoin purchase might be fairly small. Fees for credit card purchases are spelled out clearly. Here are five sites where credit card purchases are regularly processed and the additional fees you'll pay for using plastic.

bitcoin.com — The site charges a 2.5% fee, and the credit card processing tacks on another 5% by Simplex.

coinmama.com — The site charges a 5.5% fee for all transactions, and credit card users are subject to an additional 5% fee. Users cannot purchase more than $5,000 of Bitcoin per day. It's important to note that 11.5% of fees seems like an insane proposition to me.

coinbase.com — At 3.99%, this site's credit card fee seems like the most reasonable of the exchanges I browsed.

bitstamp.net — The site charges 5% for all credit card purchases.

coinhouse.io — Based in Paris, Coinhouse charges credit card fees on a tiered system. All purchases under 5,000 Euros are slapped with a 10% fee. If you're willing to buy more than 20,000 Euros worth of Bitcoin, the fee drops to 8%.

Which Cards to Use

With all those hefty fees, interested cardholders will need to focus on cards that hand out generous rewards for everyday purchases. For example, the Bank of America® Premium Rewards® credit card pays 2.625x points for spenders who hold more than $100,000 in BofA accounts. That won't cover the fees, but if Bitcoin soars while you're holding it, you would find yourself in a win-win scenario: loads of rewards and the chance to sell that Bitcoin for a big profit.

You might also consider a card that earns exceptionally high-value rewards, such as the Starwood Preferred Guest® Credit Card from American Express. Based on TPG's valuations, the 1 Starpoint per dollar you'll earn from a Bitcoin purchase equals a return of 2.7% — not enough to cancel out even the lowest credit card fee, but certainly better than a card that earns you just a 1% return on spending.

Taxes Bite Into Bitcoin Earnings

Credit card interest rates aren't the only concern that should be on the minds of Bitcoin buyers. I caught up with TPG's own JT Genter, a CPA who spent 10 years in tax accounting before focusing on writing about points and miles, and he highlighted that the IRS treats Bitcoin like property. So, for example, if someone buys $10,000 worth of Bitcoin and the value of that soars to $20,000, the additional earnings will be reported as additional personal income or a capital gain — depending on how long you hold the currency in your own possession. If you're burned by Bitcoin and you actually lose money, your capital loss deduction is limited to $3,000 per year.

Bitcoin's Role in Rewards: Minimum Spend

Okay, I've highlighted overpriced conversion fees, the dangers of potential interest charges and the Internal Revenue Service's focus on virtual currency, but JT mentioned one potential area where Bitcoin's risk can pay off with serious rewards: hitting hefty minimum spend requirements. For example, consider the British Airways Visa Signature Card. Once a cardholder crosses the $30,000 threshold, he or she will earn a Travel Together ticket good for a companion to travel for free. For certain TPG readers, it could theoretically make sense to cross that threshold with a big chunk of Bitcoin. Even for JT, though, the anxiety of watching the swings of Bitcoin value in order to maximize the perks of a credit card sounded like a very, very turbulent ride.

And if you're one of the super-savvy credit card users who isn't afraid of the risks of Bitcoin, you'll want to pay attention to every turn on that ride to know when to buy and sell. As I put the finishing touches on this post, Bitcoin's value sat at $13,907. And less than a hour after publishing, its value was down to less than $12,000, its lowest level in more than a month.

Photo by @incomecenterr via Twenty20