This Quick Trick Can Help You Save Money on International Flights

Update: Some offers mentioned below are no longer available. View the current offers here.

"Airfare pricing is simple, easy, and understandable." Said no one. Ever. As TPG's travel analyst, part of my role is to maximize how we use our miles and minimize how much money we spend on flights. I practice what I preach, and when a personal trip took me to Thailand last year, I employed one of the best tricks in the book to save some money on my intra-Thailand flights.

On a recent episode of Miles Away, I mentioned that I saved about $100 by switching my browser cookies from being US-based to Thai-based. In this post, I'm going to demonstrate what I did, and how this trick could quickly save you tens to hundreds of dollars on any of your international flights.

Background

Airlines sell tickets to many countries and in many currencies. They recognize that sometimes a US-based traveler may be willing to pay more than a traveler based elsewhere and therefore may charge different amounts for the exact same ticket. Who doesn't hate the feeling of sitting next to someone on a plane only to find out that they paid less than you for their ticket?

This presents the savvy traveler with the ability to capitalize on an arbitrage opportunity. Due to how airlines convert their prices into foreign currencies coupled with currency fluctuations, a traveler can often pay less for a ticket by choosing to pay in a foreign currency.

I'll take you through some examples of these opportunities and then explain how you can do this on your own.

(Note: All exchange rates are accurate at the time of writing. While fluctuations could make this more (or less) lucrative, the overall strategy still holds.)

Some Examples

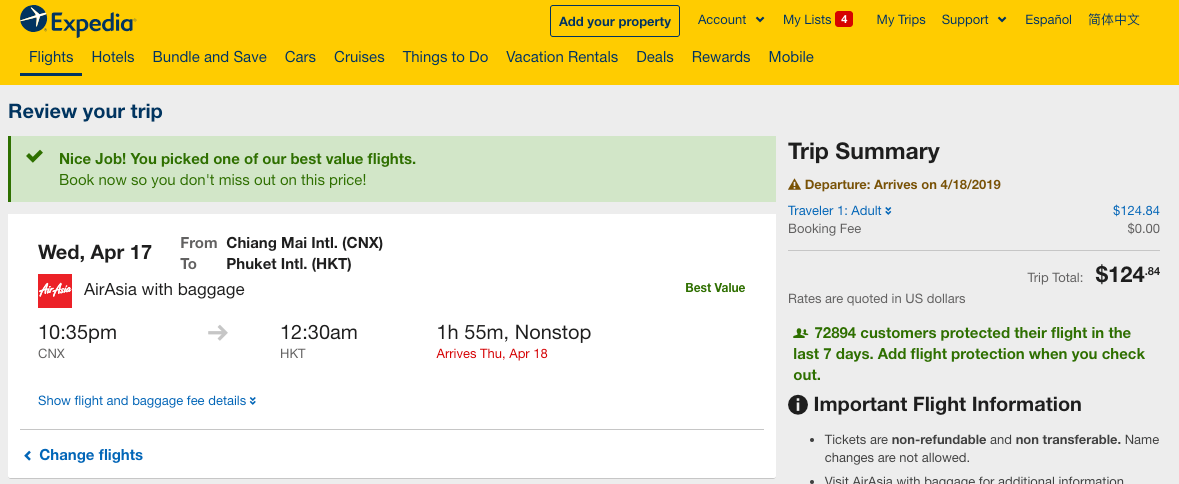

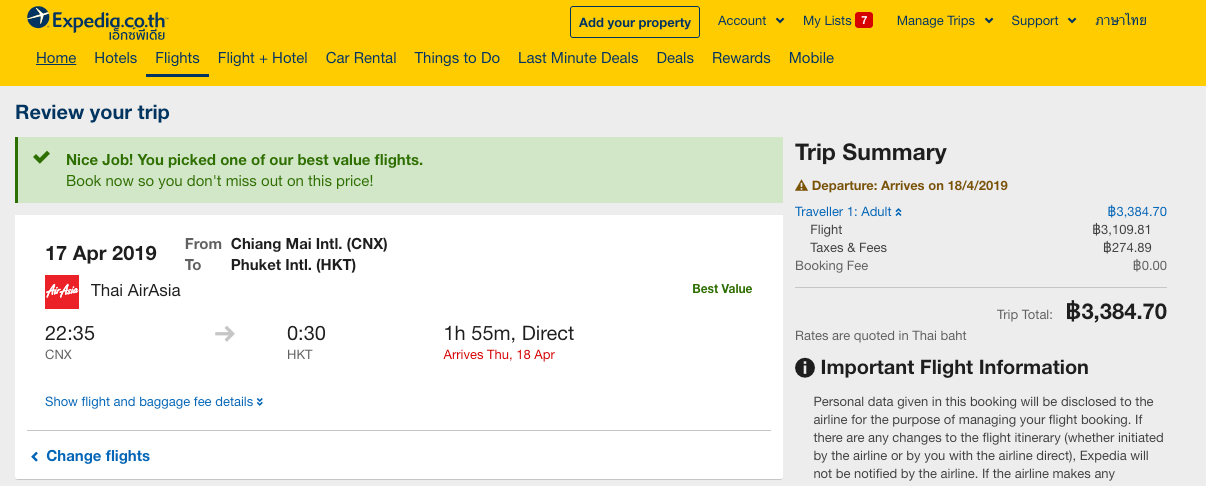

Say you're flying from Chiang Mai (CNX) to Phuket (HKT). Most people will go to Google Flights or Orbitz to start their research, and then see that the flight they want only costs $124.84.

Some people may assume this is a good deal — after all, domestic flights in the US are often more expensive. However, that doesn't hold up when you look at the same flight in Thai Baht.

When you compare the price that AirAsia charges in US Dollars (USD) vs. Thai Baht (THB) (3,384.70 THB = $106.04 USD), you would be out an additional ~$20 by paying in USD. Multiply $20 saved by a family of travelers, and you're looking at a lot more curry during your trip to Thailand.

Take a look at this next example on a route from Bangkok (BKK) to Phuket (HKT) flying on Bangkok Airways. By booking and paying in USD, you'd be out $70 per ticket.

In Thai Baht, the exact same flight prices at 1,458 THB or $45.69.

You can thank me later for the additional massage(s) you get in Thailand by saving ~$25 when buying your ticket in THB.

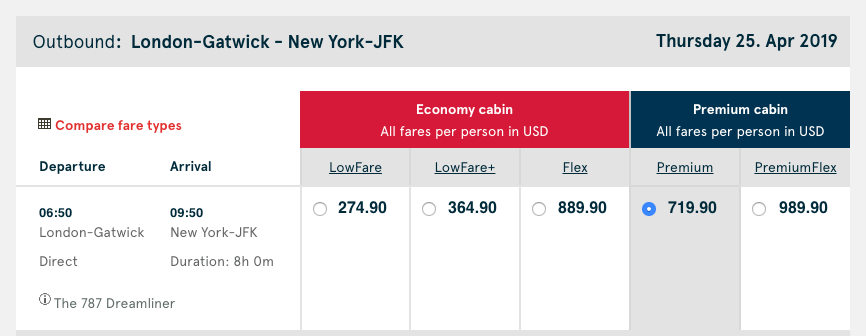

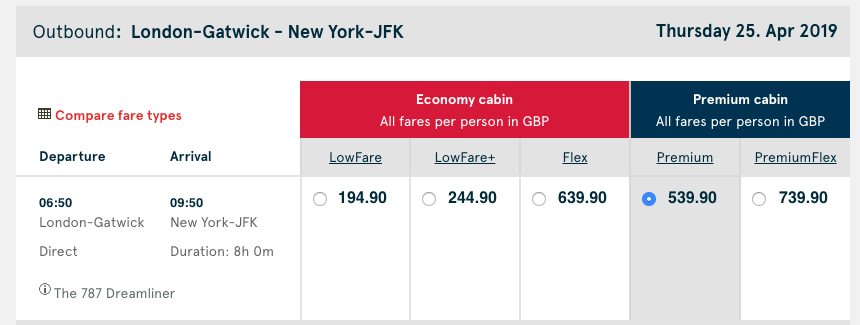

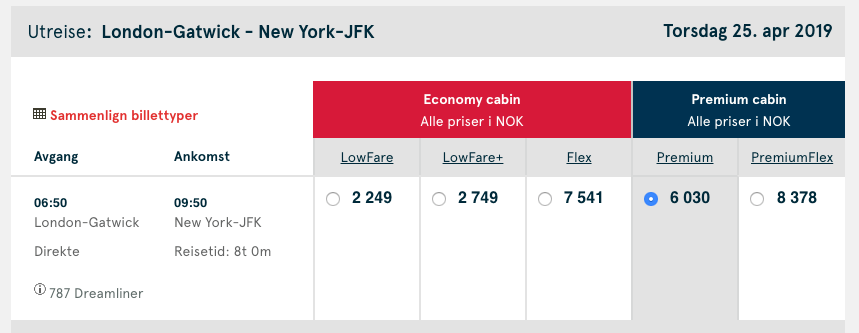

This isn't a phenomenon exclusive to Thailand. Take for example a Norwegian flight from London-Gatwick (LGW) to New York-JFK. Look at these three screenshots, and we'll compare the prices below.

What you're seeing above is the same flight from LGW to JFK priced in US Dollars (USD), British Pounds (GBP), and Norwegian Kroner (NOK).

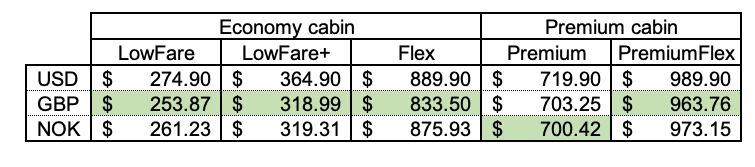

In the chart below, I've adjusted each of the prices into USD and highlighted which fare is cheapest comparing across the 3 currencies. As you'll see, it never makes sense to pay for your Norwegian ticket in USD.

How to Do It

Instead of calculating all the money you've wasted by not booking your international flights in a foreign currency, let's take a look at how you can do this on your own.

When I purchased my intra-Thailand flights, I changed my browser cookies to Thailand to get the fares to display in Thai Baht, but there is an easier way.

To get prices displayed in local currency, navigate to Expedia.com and scroll all the way down to where it says "Global Sites." Click the flag for the country in which you're trying to price the ticket, and you'll then be redirected to that country's Expedia site. You can then plug in all your travel details and compare prices with the traditional Expedia.com US-based site.

Note that you'll be transferred to an international site that may not necessarily be in a language you speak. While most of the buttons are laid out in the same way between the US and foreign based sites, you can easily use Google Translate if you're lost.

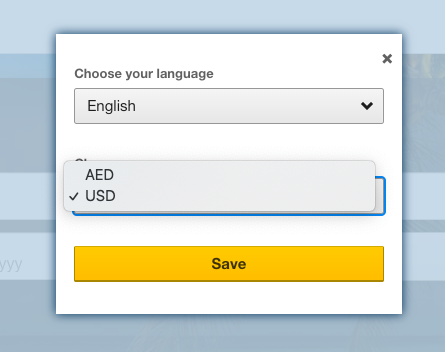

Sometimes, you'll also need to further specify that you'd like to see prices in local currency. Navigate to the top right-hand corner of the international Expedia website and click on the language icon. A dialog box should pop up asking you for your preferred currency.

Aside from Expedia.com, many airlines also have international websites that will display prices in local currencies. In the Norwegian example above, I navigated to Norwegian.com and clicked on the countries that I wanted to use to price my flights. If you're lost, you can simply Google search "Your Airline's [Insert Country Here] Website" and you should be good to go.

Just note that this doesn't always work on all airlines and all flights. Sometimes paying in USD will be your cheapest option, but it never hurts to compare.

And finally, a disclaimer: This method is not illegal or even against the terms and conditions of airlines' policies. I'm not lying or providing any inaccurate information. I am simply choosing to purchase my ticket through an alternate website in a foreign currency. To me, it's akin to Dynamic Currency Conversion. A savvy shopper knows that you should never choose to pay in US Dollars when you have the choice to do so in the local currency. The same thing holds true here.

Which card to use?

When purchasing airfare in a currency other than USD, you'll want to make sure you use a credit card that offers no foreign transaction fees. Otherwise, whatever you save by booking in a foreign currency will be negated by the surcharges imposed by your credit card company. Ideally, you'll also choose to purchase the tickets on a card that has good travel protection benefits and earns bonus points on flights.

Three of my favorites are:

- Chase Sapphire Reserve: This card earns 3x points on all travel spend (excluding $300 travel credit), has no foreign transaction fees, and offers top tier trip interruption and cancellation insurance.

- Citi Prestige Card: This card earns 5x points on all airfare purchases directly with the airline, has no foreign transaction fees, and also offers great trip insurance included for no additional cost.

- The Platinum Card® from American Express: While the Amex Platinum offers 5x points on all airfare purchased directly with the airline and incurs no foreign transaction fees (see rates & fees), it doesn't offer the same level of travel protections as the Chase Sapphire Reserve and Citi Prestige card.

Bottom Line

Everyone wants to save money on airfare. In my experience, it is often worthwhile to strategically choose the currency in which you pay for international travel. By purchasing airline tickets in foreign currencies, you can sometimes save money on the tickets, leaving more money to spend elsewhere — like sending me a thank you gift.

For rates and fees of the Amex Platinum Card, click here.