How to complete a Chase business credit card application

Editor's Note

Chase issues some of the best business credit cards on the market for freelancers and small-business owners. These cards offer strong reward-earning potential and travel perks. Before applying, understand a few key rules and requirements.

The biggest factor to consider is Chase's 5/24 rule: If you've opened five or more credit cards (from any issuer) in the past 24 months, approval for any new Chase card is unlikely. The good news is that most business cards (including Chase's) don't show up on your personal credit report, and therefore don't count against your 5/24 limit.

Whether you're a full-time entrepreneur or earn a little extra from freelance work, here's everything you need to know to complete an application for a Chase business card.

Selection of Chase business cards

Chase's lineup of non-cobranded business cards includes:

- Chase Sapphire Reserve for Business℠ (see rates and fees)

- Ink Business Cash® Credit Card (see rates and fees)

- Ink Business Preferred® Credit Card (see rates and fees)

- Ink Business Premier® Credit Card (see rates and fees)

- Ink Business Unlimited® Credit Card (see rates and fees)

Some of Chase's cobranded business cards include:

- IHG One Rewards Premier Business Credit Card (see rates and fees)

- Southwest® Rapid Rewards® Performance Business Credit Card (see rates and fees)

- Southwest® Rapid Rewards® Premier Business Credit Card (see rates and fees)

- World of Hyatt Business Credit Card (see rates and fees)

Who qualifies for a Chase business card?

A Chase business card application is similar to a Chase consumer card application. The main difference is that you need a business or sole proprietorship that earns revenue. It can be a side hustle or freelance work, and it doesn't need to be full-time or earn six figures to qualify.

A business card provides extra rewards and is essential for keeping business and personal expenses separate. Examples of qualifying businesses include:

- A freelance artist, consultant or writer

- A gig worker for a ride-hailing company or a food delivery driver

TPG senior editorial director Nick Ewen recently applied for the Sapphire Reserve for Business and documented a relatively painless process from start to finish.

Related: Who qualifies for a business credit card?

How to complete a Chase business card application

Most Chase business card applications look the same. If you're applying for a cobranded business card like the United℠ Business Card (see rates and fees), you'll notice the option to include an existing loyalty number for that program if you already have one. Otherwise, a new number will be assigned to you.

If you're already a Chase customer, log in first — some fields will prefill for a faster application experience.

Here's the information you'll need to add to the application:

- Annual business revenue/sales: This is the total annual income of your business before you deduct any expenses or taxes. This doesn't need to be a huge number — some new businesses get approved with little or no income, but if you do have business revenue, it'll certainly improve the likelihood of getting an approval.

- Business establishment date: Provide the date the business was formed.

- Business mailing address: If you work at home or don't have a business address, entering your home address is fine.

- Business name on card: This doesn't have to be your legal business name because it's the business name printed onto your card. You might need to abbreviate the name here because longer names might not fit.

- Business phone: This can be a home or mobile phone.

- Business structure: If you're the only owner, select "sole proprietor." If your business has two or more owners, choose "partnership." If your business is registered as any of the other options (LLC, nonprofit or etc.), select the appropriate option.

- General industry/category/specific type: Choose the best option for your business.

- Legal name of business: If you're a sole proprietor, you can use your name as the "legal business name." However, if you've filed with your local or state government for a DBA (doing business as) name, you'll enter that name here also. If you've set up any legal business structure, like an LLC, your "legal business name" will be the name of the LLC or other entity*.

- Number of employees: Enter the number of all additional employees, not including yourself. Enter "0" if you're the only employee.

- Tax ID type: If you're a sole proprietor, you can use your Social Security number as your tax ID. Otherwise, you'll need a federal Employer Identification Number, which you can easily apply for with the IRS.

*Note: Do not make up a business name if you don't have a DBA. Chase may ask for proof of your business, and if you don't have a DBA under the business name you entered in this field (aside from your own personal name), you'll likely be denied for a card.

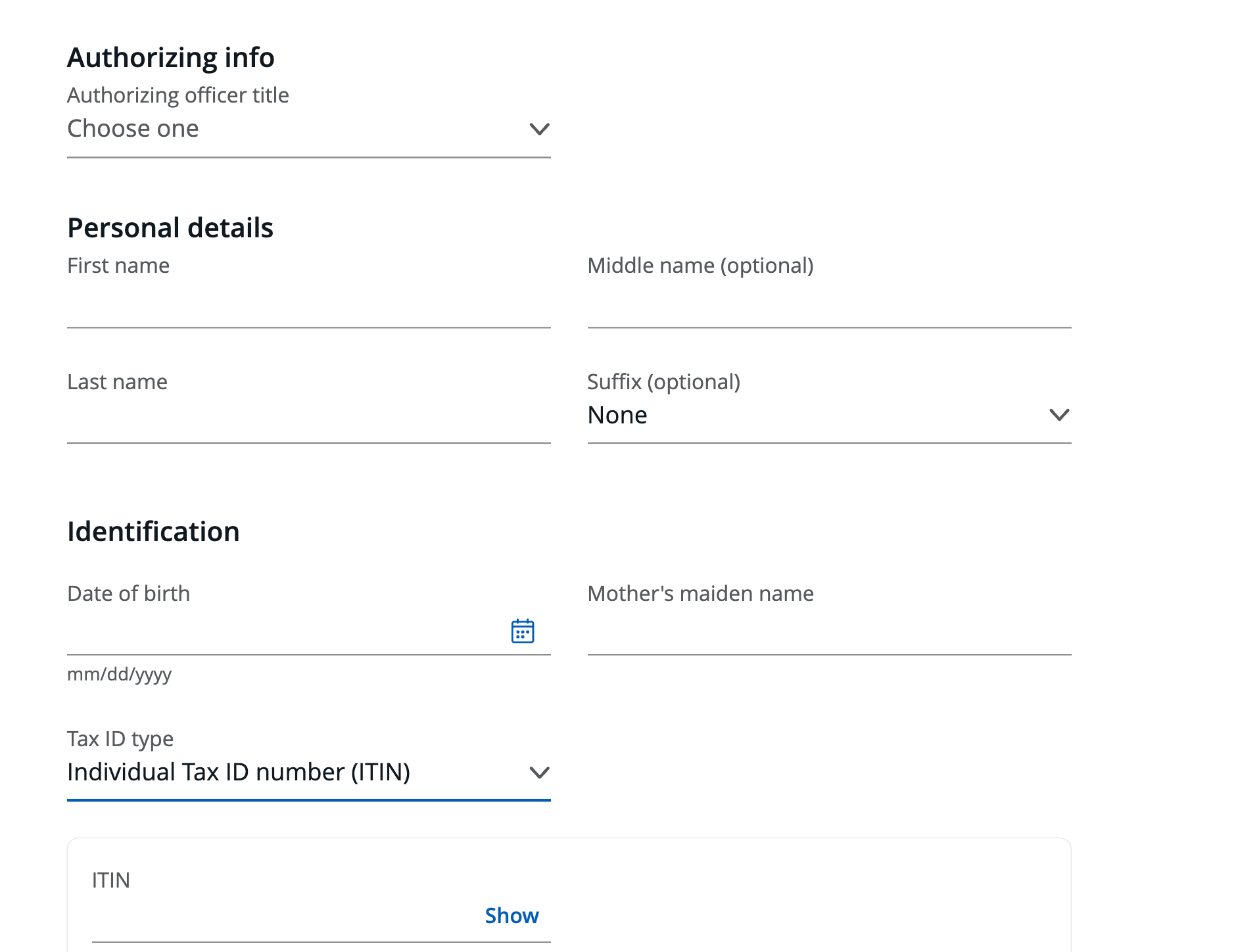

Step 1: Authorizing information, personal details and identification

Here's a look at the first part of the Chase business credit card application page:

Authorizing info refers to your role in the company, such as owner, partner, president or treasurer; if you're a sole proprietorship, select "owner."

Under Tax ID, you can apply with your SSN or Tax ID number. If you choose to use your SSN, you will see a disclosure that you must read and accept the terms.

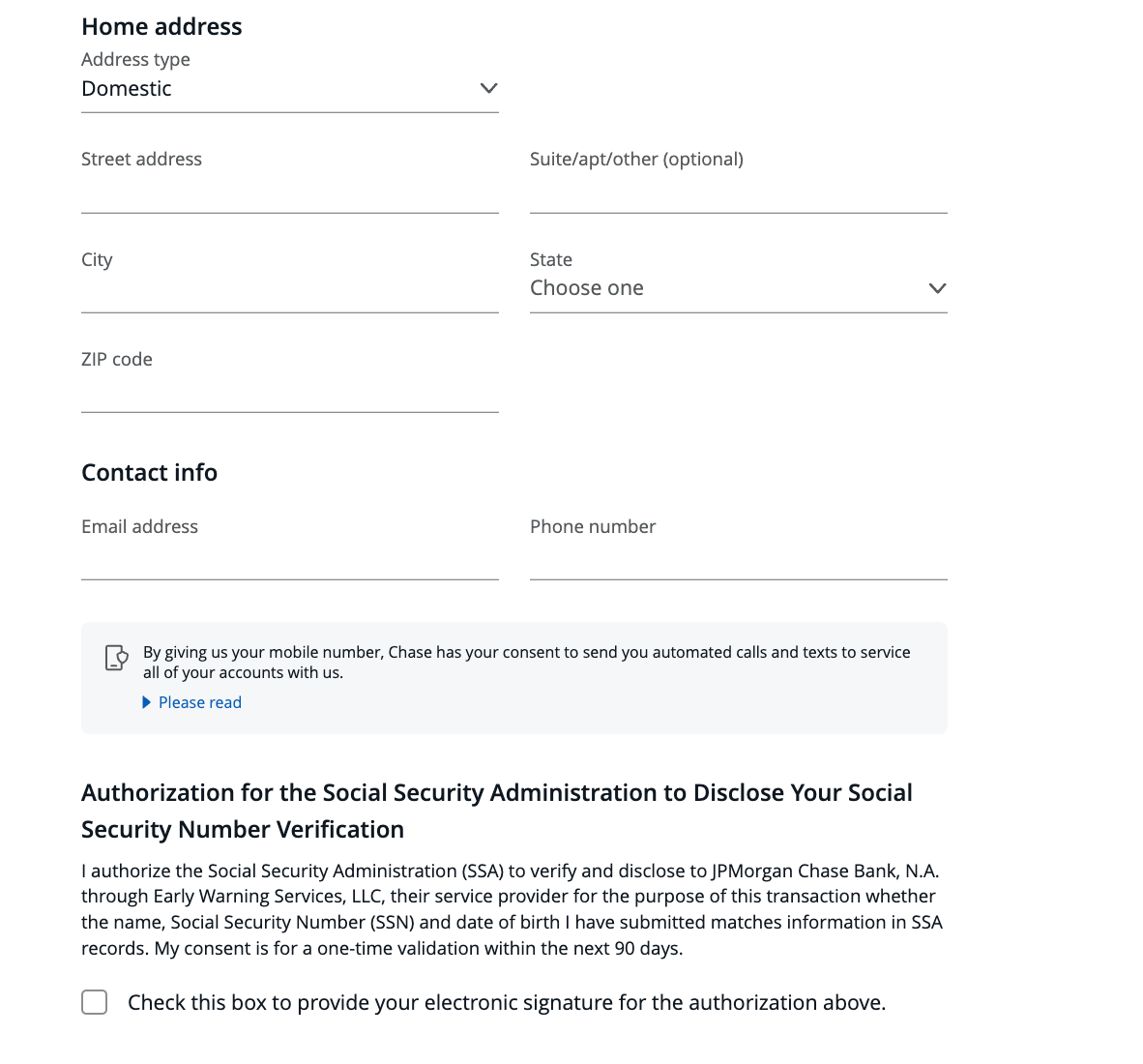

Step 2: Home address and contact information

Now you'll scroll down to the second part of the Chase business credit card application page:

Most of the personal information you have to fill out is fairly straightforward.

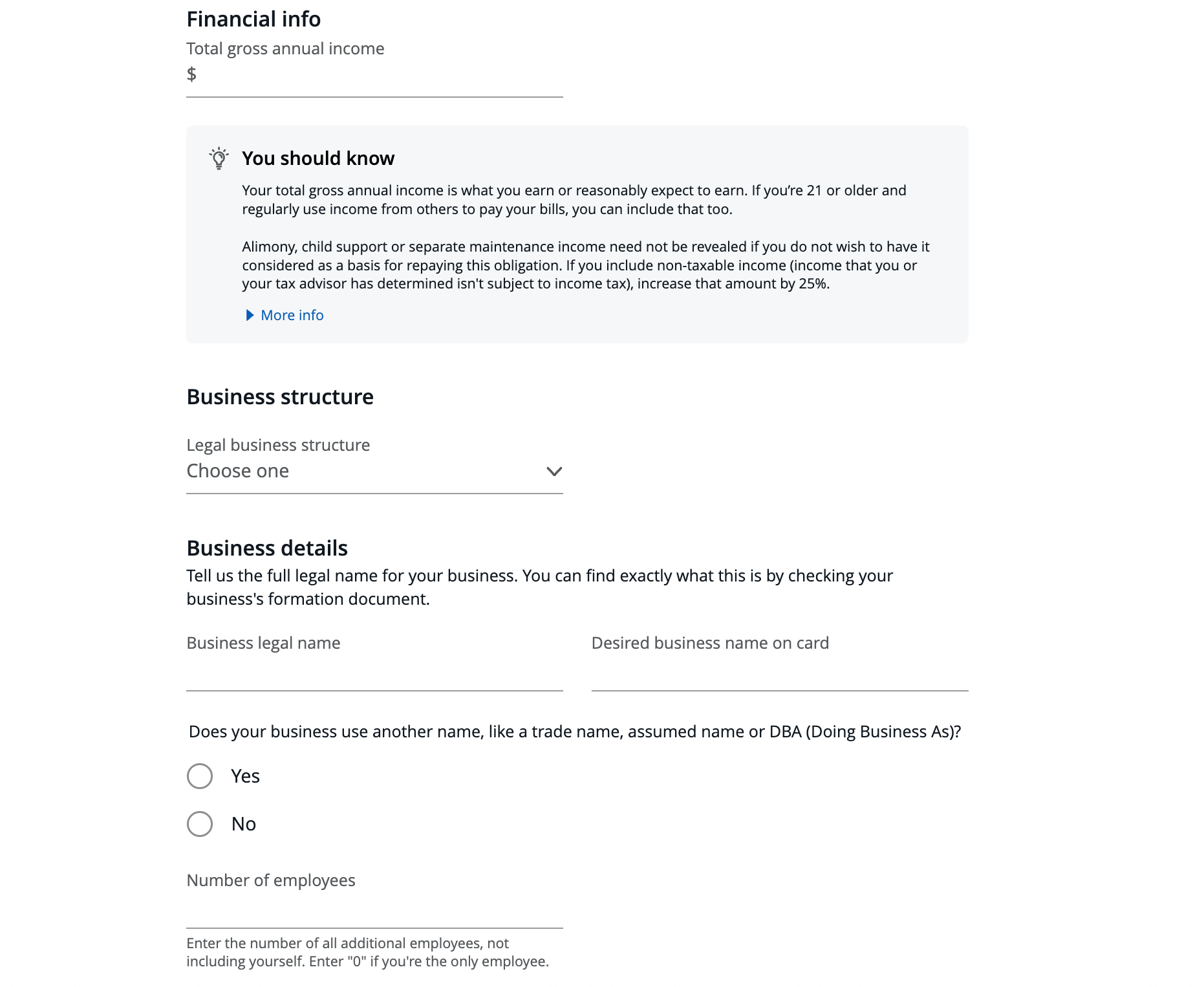

Step 3: Financial information, business structure and details

Now you'll scroll down to the third part Chase business credit card application page:

When it comes to your "total gross annual income," you want to be sure to include any eligible income, which, according to Chase, includes:

- Dividends

- Full-time or part-time jobs

- Internships

- Interest

- Investments

- Public assistance

- Seasonal jobs

- Self-employment

- Social Security benefits

- Retirement

You can also include "money that someone else deposits regularly into your account," and if you're 21 or older, you can include any income from others that you regularly use to pay your bills. If you have a partner or spouse you split the bills with, including their yearly salary with yours, is OK.

Under "Business details," enter your business name — or your legal name if you're a sole proprietor — along with the name you'd like printed on the card. After that, enter the number of employees.

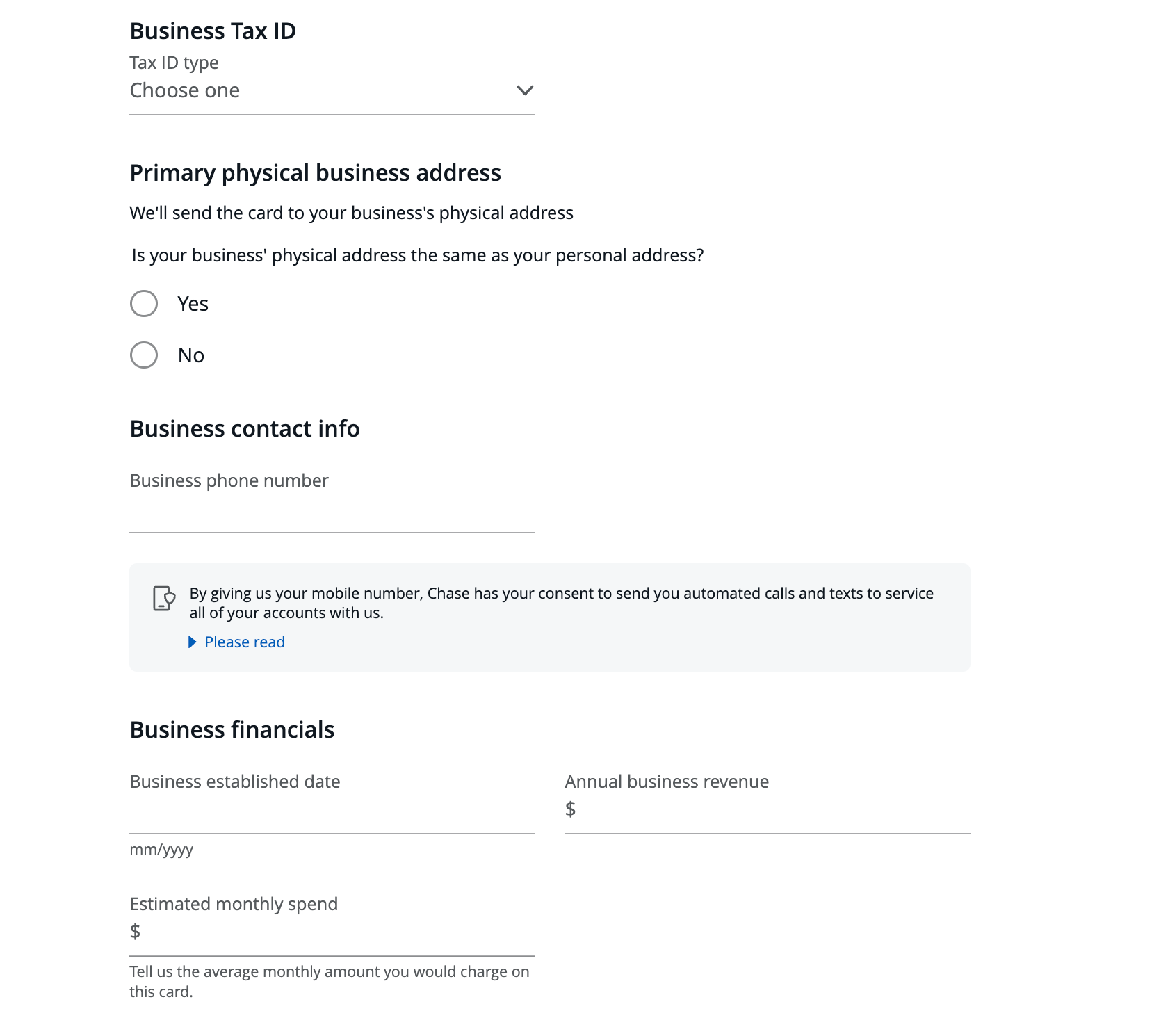

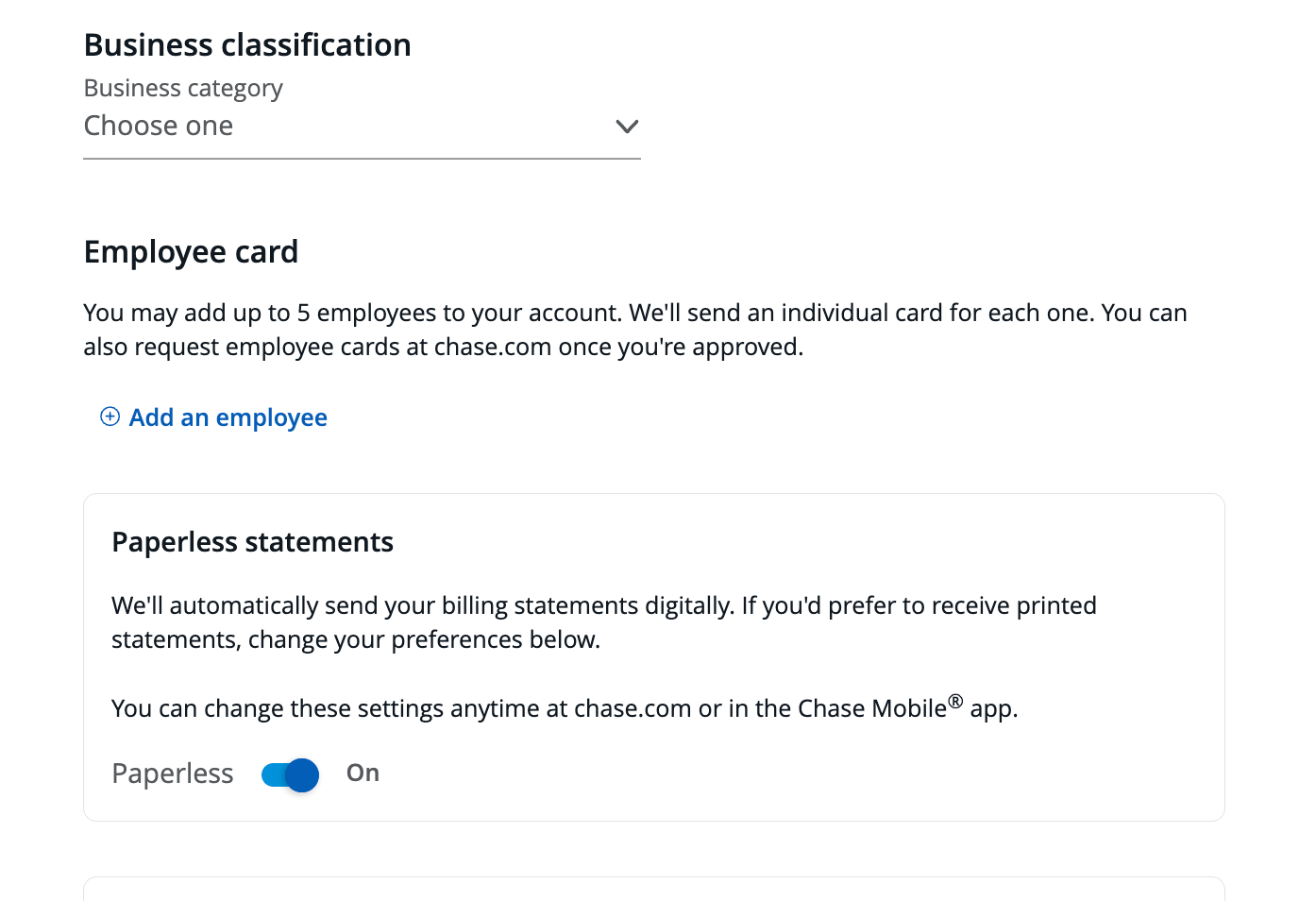

Steps 4 and 5: Business Tax ID, business address, contact info, financials, business classification and employee cards

Next, scroll down to answer the following additional questions about your business:

Next, include the applicable business tax ID and primary address. Your address can be the same as your home address if you don't have a physical location. Your business number can be your personal number if you don't have a business number.

For the business financials section, enter the date your business was formed. Then enter the annual business revenue, which is the amount the business makes before deducting any expenses or taxes.

Then enter your estimated monthly spending.

Lastly, under "business classification," select the appropriate field your business is in. You can add employee cards and select if you would like to receive paperless statements.

After filling out the required information, review the terms before submitting. At the very bottom, just above the "Submit" button, there's a box you'll need to check to show you've read and agreed to the terms.

Related: How to get a business credit card

Bottom line

Applying for a Chase business credit card is more straightforward than many realize. You may qualify if you earn any business income — even part-time freelance or gig work. Be sure that the information you provide is honest and consistent, especially regarding your business name, structure and revenue, as Chase can request verification.

A business credit card isn't just a way to earn rewards — it separates business and personal finances, simplifies your bookkeeping and strategically manages your 5/24 count. If you're eligible, applying could be a smart next step in your points and miles strategy.

Related: How to pick a strategy for your small-business credit cards

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.