How Small Businesses Can Start Accepting Credit Cards

It probably goes without saying that all businesses — no matter how small or large — need to accept credit cards. Besides enabling customers to earn valuable points and miles, credit cards can boost sales, improve cash flow and simplify accounting.

Fortunately, it's becoming easier and cheaper for small businesses to take credit cards. Let's take a look at what's involved.

Merchant Accounts vs. All-In-One Solutions

The first step toward accepting credit cards is deciding whether you want to open your own merchant account or enlist an all-in-one solution like PayPal or Square which aggregates all of its accounts into a shared merchant account. In short, merchant accounts are the intermediary between you and the credit issuers — after a payment is processed, the funds first go into a merchant account before eventually being transferred to your bank.

All-in-one solutions simplify things in the short term, but are more costly down the line — including for consumers. If you have an all-in-one solution, you'll pay a flat rate for transactions, meanwhile if you have your own merchant account you'll pay different fees (which are usually lower than the flat-rate fees) based on the type of transaction and credit card network. Opening a merchant account is a lengthier process and often requires you to lock in a multi-year contract, but is typically the smarter choice long-term.

Setting Up a Merchant Account

Unless you take the easy route and go with an all-in-one solution, you'll be shopping around for a payment processor that best suits your business. There are many companies out there, with the biggest difference between them being the markups (which are often negotiable) they charge on top of the transaction fees set by credit card networks.

Historically, merchant accounts automatically bundled Visa, Mastercard and Discover together, leaving American Express as an add-on with a separate contract. That's because Amex is set up differently from the major networks — unlike Visa and Mastercard, Amex both issues credit cards and owns the network that processes transactions. Additionally, Amex was known for having much higher pricing than its competitors. However, that doesn't really hold true anymore. On average, there's little difference today between the cost to accept American Express in the US and the cost to accept other major credit cards.

OptBlue

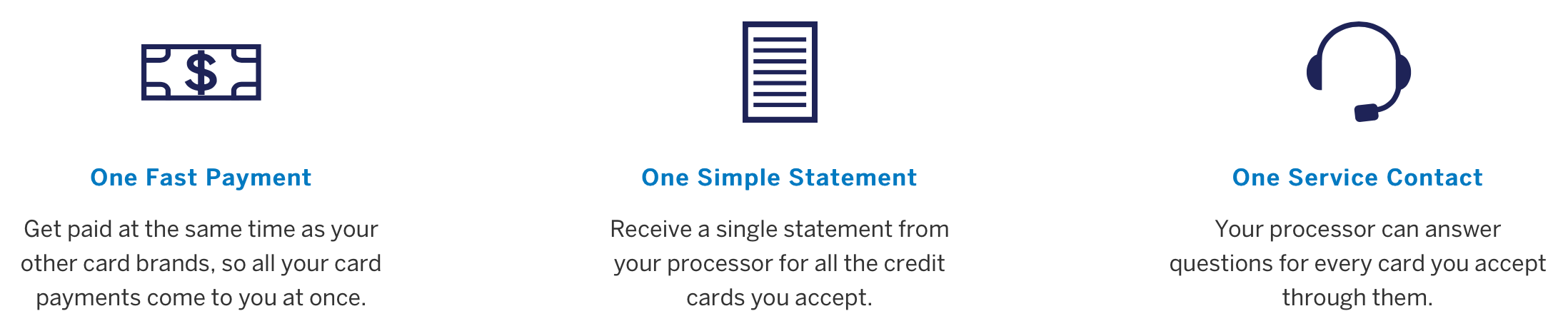

Thanks to Amex's program OptBlue, small businesses can now accept Amex the same way they accept other major card networks without needing to enter into a separate contract with American Express. And according to Amex, the OptBlue program has drastically increased the number of US small businesses that now accept its cards.

Through the program, Amex gives payment processors wholesale rates and lets them set their own merchant fees depending on the transactions, the same way they do with other networks. Accepting Amex through OptBlue means you, the business owner, can find the best rates for your company, and combine your statements and payments across all cards you're accepting into one.

Other Considerations

Once you have your merchant account set up, there are a few other factors you'll need to consider before you can start accepting credit cards. For instance, if your business accepts payments online, you'll need to set up a payment gateway, and if your business accepts payments in person you'll need hardware.

When picking hardware, you'll have to choose between point-of-sale (POS) systems and terminals. Payment terminals are the smaller, often hand-held, machines you see in most stores today. They're cost-effective and get the job done — to accept or decline credit/debits cards, as well as processing mobile payments. POS systems, on the other hand, have additional features, such as the ability to track inventory and record employee clock-in/clock-out times.

Bottom Line

There are many benefits to accepting credit cards as a form of payment, and fortunately, doing so isn't too difficult — no matter the type of card.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.