How Small Businesses Can Start Accepting Credit Cards

It probably goes without saying that all businesses — no matter how small or large — need to accept credit cards. Besides enabling customers to earn valuable points and miles, credit cards can boost sales, improve cash flow and simplify accounting.

Fortunately, it's becoming easier and cheaper for small businesses to take credit cards. Let's take a look at what's involved.

Merchant Accounts vs. All-In-One Solutions

The first step toward accepting credit cards is deciding whether you want to open your own merchant account or enlist an all-in-one solution like PayPal or Square which aggregates all of its accounts into a shared merchant account. In short, merchant accounts are the intermediary between you and the credit issuers — after a payment is processed, the funds first go into a merchant account before eventually being transferred to your bank.

All-in-one solutions simplify things in the short term, but are more costly down the line — including for consumers. If you have an all-in-one solution, you'll pay a flat rate for transactions, meanwhile if you have your own merchant account you'll pay different fees (which are usually lower than the flat-rate fees) based on the type of transaction and credit card network. Opening a merchant account is a lengthier process and often requires you to lock in a multi-year contract, but is typically the smarter choice long-term.

Setting Up a Merchant Account

Unless you take the easy route and go with an all-in-one solution, you'll be shopping around for a payment processor that best suits your business. There are many companies out there, with the biggest difference between them being the markups (which are often negotiable) they charge on top of the transaction fees set by credit card networks.

Historically, merchant accounts automatically bundled Visa, Mastercard and Discover together, leaving American Express as an add-on with a separate contract. That's because Amex is set up differently from the major networks — unlike Visa and Mastercard, Amex both issues credit cards and owns the network that processes transactions. Additionally, Amex was known for having much higher pricing than its competitors. However, that doesn't really hold true anymore. On average, there's little difference today between the cost to accept American Express in the US and the cost to accept other major credit cards.

OptBlue

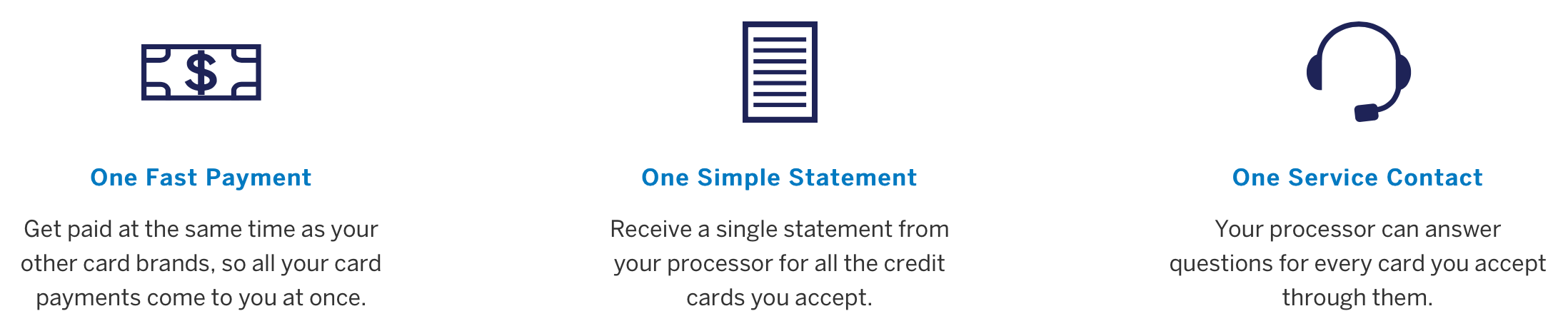

Thanks to Amex's program OptBlue, small businesses can now accept Amex the same way they accept other major card networks without needing to enter into a separate contract with American Express. And according to Amex, the OptBlue program has drastically increased the number of US small businesses that now accept its cards.

Through the program, Amex gives payment processors wholesale rates and lets them set their own merchant fees depending on the transactions, the same way they do with other networks. Accepting Amex through OptBlue means you, the business owner, can find the best rates for your company, and combine your statements and payments across all cards you're accepting into one.

Other Considerations

Once you have your merchant account set up, there are a few other factors you'll need to consider before you can start accepting credit cards. For instance, if your business accepts payments online, you'll need to set up a payment gateway, and if your business accepts payments in person you'll need hardware.

When picking hardware, you'll have to choose between point-of-sale (POS) systems and terminals. Payment terminals are the smaller, often hand-held, machines you see in most stores today. They're cost-effective and get the job done — to accept or decline credit/debits cards, as well as processing mobile payments. POS systems, on the other hand, have additional features, such as the ability to track inventory and record employee clock-in/clock-out times.

Bottom Line

There are many benefits to accepting credit cards as a form of payment, and fortunately, doing so isn't too difficult — no matter the type of card.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 3X | Earn 3X Miles on Delta purchases. |

| 1X | Earn 1X Miles on all other eligible purchases. |

Pros

- Delta SkyClub access when flying Delta

- Annual companion ticket for travel on Delta (upon renewal)

- Ability to earn MQDs through spending

- Various statement credits for eligible purchases

Cons

- Steep annual fee of $650

- Other Delta cobranded cards offer superior earning categories

- Earn 100,000 Bonus Miles after you spend $6,000 or more in purchases with your new Card within the first 6 months of Card Membership and an additional 25,000 bonus miles after you make an additional $3,000 in purchases on the Card within your first 6 months, starting from the date that your account is opened. Offer Ends 04/01/2026.

- Delta SkyMiles® Reserve American Express Card Members receive 15 Visits per Medallion® Year to the Delta Sky Club® when flying Delta and can unlock an unlimited number of Visits after spending $75,000 in purchases on your Card in a calendar year. Plus, you’ll receive four One-Time Guest Passes each Medallion Year so you can share the experience with family and friends when traveling Delta together.

- Enjoy complimentary access to The Centurion® Lounge in the U.S. and select international locations (as set forth on the Centurion Lounge Website), Sidecar by The Centurion® Lounge in the U.S. (see the Centurion Lounge Website for more information on Sidecar by The Centurion® Lounge availability), and Escape Lounges when flying on a Delta flight booked with the Delta SkyMiles® Reserve American Express Card. § To access Sidecar by The Centurion® Lounge, Card Members must arrive within 90 minutes of their departing flight (including layovers). To access The Centurion® Lounge, Card Members must arrive within 3 hours of their departing flight. Effective July 8, 2026, during a layover, Card Members must arrive within 5 hours of the connecting flight.

- Receive $2,500 Medallion® Qualification Dollars with MQD Headstart each Medallion Qualification Year and earn $1 MQD for each $10 in purchases on your Delta SkyMiles® Reserve American Express Card with MQD Boost to get closer to Status next Medallion Year.

- Enjoy a Companion Certificate on a Delta First, Delta Comfort, or Delta Main round-trip flight to select destinations each year after renewal of your Card. The Companion Certificate requires payment of government-imposed taxes and fees of between $22 and $250 (for itineraries with up to four flight segments). Baggage charges and other restrictions apply. Delta Basic experiences are not eligible for this benefit.

- $240 Resy Credit: When you use your Delta SkyMiles® Reserve American Express Card for eligible purchases with U.S. Resy restaurants, you can earn up to $20 each month in statement credits. Enrollment required.

- $120 Rideshare Credit: Earn up to $10 back in statement credits each month after you use your Delta SkyMiles® Reserve American Express Card to pay for U.S. rideshare purchases with select providers. Enrollment required.

- Delta SkyMiles® Reserve American Express Card Members get 15% off when using miles to book Award Travel on Delta flights through delta.com and the Fly Delta app. Discount not applicable to partner-operated flights or to taxes and fees.

- With your Delta SkyMiles® Reserve American Express Card, receive upgrade priority over others with the same Medallion tier, product and fare experience purchased, and Million Miler milestone when you fly with Delta.

- Earn 3X Miles on Delta purchases and earn 1X Miles on all other eligible purchases.

- No Foreign Transaction Fees. Enjoy international travel without additional fees on purchases made abroad.

- $650 Annual Fee.

- Apply with confidence. Know if you're approved for a Card with no impact to your credit score. If you're approved and you choose to accept this Card, your credit score may be impacted.

- Terms Apply.

- See Rates & Fees