Can you close a credit card with a balance?

Editor's Note

Applying for and opening a new credit card can be exciting because new cards usually offer a welcome bonus after you meet a minimum spend requirement in a specific period of time.

At the end of every billing cycle, you receive a statement — the money owed to the issuer — which we recommend paying off in full whenever possible. But what happens when you close a credit card with a balance? Does it hurt your credit score and affect future borrowing needs?

Here's what you need to know about closing a credit card with a balance.

Pay off a credit card or maintain a balance?

To avoid interest charges, it's best practice to pay off the credit card balance each month. When carrying a balance month to month, interest charges begin to accrue; this diminishes the value you receive from a card, such as points, miles or cash back rewards.

That said, you may maintain a balance on your credit card as long as you pay off the minimum statement balance (which we strongly advise against; if you're unable to pay off a balance in full, do your best to send in a payment for more than the minimum required amount).

The current balance on a credit card is not subject to interest charges until that month's billing cycle ends.

Can you close a credit card with a balance?

Closing a credit card with a balance is possible. However, there are some things to keep in mind.

When you close a credit card, you can no longer make purchases on the credit card and also forfeit transferable rewards points. Upon closing a credit card with a balance, you remain responsible for the balance and will continue to accrue interest on it while receiving billing statements.

If you are determined to close a credit card, it's better to pay off any current balance before doing so to avoid late fees, interest charges and the possibility of the debt being sent to collections if left unresolved. If the card has no annual fee, you're better off leaving the account open and leaving it for emergency use; if it does have an annual fee, you can consider downgrading to a card with no annual fee.

Another alternative to closing a card with a balance is to transfer the balance to an existing or new credit card. By transferring the balance on the card you wish to close, you can avoid paying a lump sum of the balance and avoid interest fees for a promotional period.

Check out TPG's best balance transfer credit cards to see how to take advantage of great offers.

Related: The best way to pay credit card bills

Impact of closing a credit card with a balance

Closing a credit card with a balance can hurt you in several ways, including negatively affecting your credit score and overall credit report.

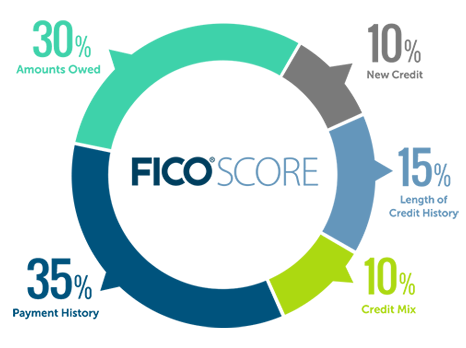

When closing a credit card, you reduce the length of your credit history and the average age of your accounts. Length of credit history makes up 15% of your FICO score, so expect a dip when you close a credit card.

If you close a credit card with a balance, you also increase your credit utilization, as this reduces your overall credit across all accounts. If the closing of a credit card pushes your utilization over 30% of the total available credit, you risk negatively affecting your credit score.

If you close a card due to a history of late payments, know that such incidents remain on your credit report for about seven years.

Closing a credit card with a balance can also affect you long term if you do not pay off the balance promptly. You'll continue to receive billing statements for any balances owed to the issuer.

If the balance remains unresolved for some time, the issuer can send it to a collections agency, and it will be reported to the three credit bureaus. This will negatively affect your creditworthiness in a big way.

Bottom line

It is possible to close a credit card with a balance. However, despite closing the account, you are still responsible for paying the balance and any associated late or interest fees. A better move is to pay off the entire balance of a credit card before closing the account.

If you can avoid closing a card by downgrading it to a no-annual-fee card or shifting its line of credit to another card with the same issuer, you may be able to protect your credit score and avoid dealing with future interest charges or negative marks on your credit report.

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 3X | Earn 3X Miles on Delta purchases. |

| 1X | Earn 1X Miles on all other eligible purchases. |

Pros

- Delta SkyClub access when flying Delta

- Annual companion ticket for travel on Delta (upon renewal)

- Ability to earn MQDs through spending

- Various statement credits for eligible purchases

Cons

- Steep annual fee of $650

- Other Delta cobranded cards offer superior earning categories

- Earn 100,000 Bonus Miles after you spend $6,000 or more in purchases with your new Card within the first 6 months of Card Membership and an additional 25,000 bonus miles after you make an additional $3,000 in purchases on the Card within your first 6 months, starting from the date that your account is opened. Offer Ends 04/01/2026.

- Delta SkyMiles® Reserve American Express Card Members receive 15 Visits per Medallion® Year to the Delta Sky Club® when flying Delta and can unlock an unlimited number of Visits after spending $75,000 in purchases on your Card in a calendar year. Plus, you’ll receive four One-Time Guest Passes each Medallion Year so you can share the experience with family and friends when traveling Delta together.

- Enjoy complimentary access to The Centurion® Lounge in the U.S. and select international locations (as set forth on the Centurion Lounge Website), Sidecar by The Centurion® Lounge in the U.S. (see the Centurion Lounge Website for more information on Sidecar by The Centurion® Lounge availability), and Escape Lounges when flying on a Delta flight booked with the Delta SkyMiles® Reserve American Express Card. § To access Sidecar by The Centurion® Lounge, Card Members must arrive within 90 minutes of their departing flight (including layovers). To access The Centurion® Lounge, Card Members must arrive within 3 hours of their departing flight. Effective July 8, 2026, during a layover, Card Members must arrive within 5 hours of the connecting flight.

- Receive $2,500 Medallion® Qualification Dollars with MQD Headstart each Medallion Qualification Year and earn $1 MQD for each $10 in purchases on your Delta SkyMiles® Reserve American Express Card with MQD Boost to get closer to Status next Medallion Year.

- Enjoy a Companion Certificate on a Delta First, Delta Comfort, or Delta Main round-trip flight to select destinations each year after renewal of your Card. The Companion Certificate requires payment of government-imposed taxes and fees of between $22 and $250 (for itineraries with up to four flight segments). Baggage charges and other restrictions apply. Delta Basic experiences are not eligible for this benefit.

- $240 Resy Credit: When you use your Delta SkyMiles® Reserve American Express Card for eligible purchases with U.S. Resy restaurants, you can earn up to $20 each month in statement credits. Enrollment required.

- $120 Rideshare Credit: Earn up to $10 back in statement credits each month after you use your Delta SkyMiles® Reserve American Express Card to pay for U.S. rideshare purchases with select providers. Enrollment required.

- Delta SkyMiles® Reserve American Express Card Members get 15% off when using miles to book Award Travel on Delta flights through delta.com and the Fly Delta app. Discount not applicable to partner-operated flights or to taxes and fees.

- With your Delta SkyMiles® Reserve American Express Card, receive upgrade priority over others with the same Medallion tier, product and fare experience purchased, and Million Miler milestone when you fly with Delta.

- Earn 3X Miles on Delta purchases and earn 1X Miles on all other eligible purchases.

- No Foreign Transaction Fees. Enjoy international travel without additional fees on purchases made abroad.

- $650 Annual Fee.

- Apply with confidence. Know if you're approved for a Card with no impact to your credit score. If you're approved and you choose to accept this Card, your credit score may be impacted.

- Terms Apply.

- See Rates & Fees