Explaining Your Points and Miles Hobby to Friends and Family

Update: Some offers mentioned below are no longer available. View the current offers here.

Those of us in the points and miles hobby understand that credit card sign-up bonuses are among the fastest ways to earn points and miles, aside from actually flying. Importantly, we also understand how opening a new credit card could affect our credit scores. However, sometimes it feels like we're in the minority. Many people out there think there must be a catch when we earn rewards, or that we're being reckless with our financial health every time we collect a new sign-up bonus.

So what do you do when someone asks you about your travel; when they're curious about how you got to fly in first class, or how you take so many trips? When you explain your points and miles obsession to your partner, parents, in-laws, friends or co-workers, how do you get them to realize that you're not insane, and that you're, in fact, extremely responsible about your finances? And how do you help them get involved so that they can enjoy award travel with you?

Understanding Credit Scores

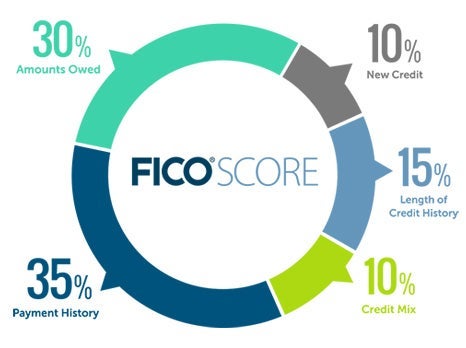

First, let's take a quick look back at how credit scores work. While a few different companies calculate credit scores using their own respective models, the one that's most commonly used by lenders is FICO. Your FICO score is a number between 300 and 850, with higher being better. While anything above 720-740 is generally considered to be excellent, even if your score is lower you can still get approved for new accounts and/or get good interest rates on loans.

A few different factors make up your FICO score. Each of those factors is examined and given a numerical value that weighs into your final score (see the chart above).

If you pay your accounts off in full and on time, only utilize a fraction of your available credit at any one time, have a few different types of accounts — revolving credit, like credit cards, and installment loans, like mortgages or student loans — and don't have too many new accounts, you'll generally have a great score.

When you apply for and open a new card, your score may dip temporarily as the average age of all of your accounts decreases and the request for new credit appears on your report. However, your score typically recovers quickly, and the drop is rarely significant unless you have a very limited credit history. Furthermore, the drop is typically canceled out by the positive aspects of opening a new account — adding to your total available credit means that your utilization decreases, and while the account ages decreases in the short term, it eventually builds the total age of all of your accounts.

Credit Card Misunderstandings

At TPG, we work to share the best opportunities to use credit card spending and sign-up bonuses to score free or heavily discounted travel. We love using points and miles to experience some of the best air travel products and best hotels in the world. At the same time, it's important to remember to practice financial discipline when using credit cards. It's only worth earning credit card rewards if you can pay your balance in full each month — interest charges will likely negate any value you earn from rewards. Furthermore, points and miles might not be for you if you have trouble controlling spending; otherwise you risk running into debt.

What many people don't realize is that you can pay off credit cards in full each month to avoid interest. In other cases, maybe they don't understand the perks of certain cards well enough to see how you can get value that outweighs the annual fee. Because Americans currently carry a record amount of credit card debt, that isn't surprising.

That explains why our friends and family might worry when they hear that we're opening new cards and avoiding using cash so that we can earn rewards. The best way to explain what you're doing with points is to address their concerns, and help spread your knowledge of how the credit system works.

Let's look at a few of the most common reactions you might hear to your points and miles hobby, and some suggestions on how to address them.

1. "You'll ruin your credit score."

As we saw above, any negative impact that opening a new credit card has on your credit score is temporary. Eventually, it may even improve your score, by adding to your history of accounts with on-time payments and decreasing your utilization. Explaining the concept of utilization in your FICO score, along with showing that you have a well-rounded understanding of how credit scores work, can go a long way toward reassuring others.

2. "You'll end up in debt."

Not true — as long as you're disciplined with your spending and finances. When you get your credit card statement each month, there's a minimum payment listed. That's the very least you have to pay on that statement — however, it doesn't imply that there's a maximum. By paying off your balance in full each month as if your credit card were a charge card — such as The Platinum Card from American Express — you'll never have to worry about debt. Just spend within your means and avoid spending money that you don't have, just like you'd do if you were using cash or a debit card. Explaining this is helpful, and may even inspire someone you know to get started with credit card rewards or avoid debt.

3. "What if you want to buy a house? You'll have trouble getting a mortgage."

Opening a credit card online is easy. You submit a form, and a computer program pulls your credit report and looks at your score and then gives you a decision (automatically, most of the time). Mortgages, however, are an entirely different process.

When you apply for a mortgage, rather than having a computer program analyze your credit score, a loan officer delves deep into the finer details of your credit report. If he or she sees a burst of credit card applications, you'll likely be asked to explain the reason, to make sure it doesn't indicate financial trouble. Explaining that you opened a few new cards to try and maximize rewards, or to experiment with different travel perks, is usually all you need to do.

That said, it's wise to take a bit of a break from new card applications if you're planning on applying for a major loan soon, like a mortgage or a car loan. You should especially put the brakes on opening new credit cards once you start the mortgage application; applying for more cards during that process may make it look like you need the credit or are concerned about income, which can raise red flags.

4. "How can you be sure you aren't hurting your credit?"

The best way to protect your financial health is to be proactive — and part of that means monitoring your credit score. By keeping an eye on it, you'll avoid any surprises, and can see for yourself the effects of any new cards or applications.

There are a few ways to check your score for free. Some cards come with features which let you check your FICO score periodically — Discover's tool is even available to people who aren't cardholders. American Express, Barclaycard, Chase and Citi all offer a version of your FICO score. While Capital One shows your score through its credit tracker tool, it uses a different model than FICO.

There are also other tools available, too. Credit Karma offers free access to your credit score — it uses a model called VantageScore 4.0, rather than the FICO model, but it can still be useful for tracking any changes. You can also access your complete credit report from all three credit bureaus — though you have to pay for a numerical credit score — by visiting AnnualCreditReport.com. This is a good practice anyway, to avoid falling victim to fraudulent activity.

5. "There has to be a catch…right?"

This is a question I get a lot. The short answer is — no, there's no catch.

For the slightly longer answer, we need to take a quick look into how credit card rewards are funded, and who pays for them. Each card processor — think American Express, Mastercard and Visa, rather than the banks that issue the cards — charge merchants a fee, known as an interchange fee, in exchange for the convenience of being able to process credit card transactions. The cost of that fee is built into a merchant's prices. That's part of why credit card companies offer incentives such as spending category bonuses.

In combination with interchange fees, credit card rewards are funded by the same things that help card issuers make money — fees and interest charges (the latter of which can be avoided). So as long as you're paying your balances in full and assessing your card portfolio to make sure that the benefits you get are worth the annual fee — like TPG does every six months or so — then no, there's no catch to earning points and miles to help fund your travel.

Bottom Line

It's unsurprising that friends and family worry when they hear about us using credit card rewards to help fund travel, especially when you consider the misinformation that's out there and the amount of overall credit card debt in the United States. However, doing your research and understanding where your rewards come from can help keep your finances in order and reassure your loved ones. You might even convince them to start collecting points and miles by leveraging credit cards!

What are your most successful tips for explaining your points and miles hobby to friends and family?

TPG featured card

at American Express's secure site

Terms & restrictions apply. See rates & fees.

| 4X | Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 4X | Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year. |

| 5X | New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App. |

| 3X | Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines. |

| 2X | Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com. |

| 1X | Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases. |

Pros

- Valuable dining and food-related credits

- Flexible rewards with airline and hotel transfer partners

- Multiple travel and purchase protections

- No foreign transaction fees

- Access to Amex Offers for additional savings (enrollment required)

Cons

- Not as useful for those living outside the U.S.

- Some may have trouble using Uber and other dining credits

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You’ll know upfront exactly how much you’ll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That’s up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin’ locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind – backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.