What Is A Bitcoin and Might They Be Useful For Travelers?

Update: Some offers mentioned below are no longer available. View the current offers here.

TPG Assistant Editor Melanie Wynne takes us through a quick history of the bitcoin and analyzes the future of this digital currency and whether travelers could take advantage of it in the future.

In the four-year history of the digital currency known as bitcoin, I've referred to it as the "LaserDisc of money" more than once, regarding it as a interesting technology that has never managed to resonate with a broad audience. However, after two recent security breaches of my Chase Sapphire Preferred Card (thanks, Target) and in light of recent mileage program devaluations at American, US Airways, United and Delta, I'm finally beginning to see some advantages to this digital currency, especially for travel.

Whether or not bitcoin will stabilize in value and become widely accepted remains to be seen, but since trust in global banking systems and fear of credit card theft and fraud could continue to be hot button topics for the foreseeable future, the bitcoin and digital currency landscape is certainly worthy of exploration here on TPG.

What is bitcoin?

A reaction to the financial implosion of 2008, bitcoin was created in 2009 as an open, global peer-to-peer payment system by a then-unknown person named Satoshi Nakamoto. (Nakamoto has since been identified as Dorian Nakamoto of Temple City, California, but theories about a bitcoin ghostwriter still persist.)

The following video breaks down the basics of bitcoin:

Bitcoin differs from dollars and cents in that it has no physical shape, and requires no banks or real names to make transactions. It's simply digital information that's collected andtransmitted viadigital walletsstored on smartphone apps (like Bitcoin Wallet) or computer desktops (such as Hive or MultiBit).

Getting set up with a digital wallet is a simple process. As a Mac user, I chose to set up a digital wallet for myself via Mac-friendly computer desktop program Hive, and it took less than 2 minutes.

The home page for Hive.com asks you to download its desktop program for Mac OS X. Once you click the yellow button, it downloads a .zip file to your desktop. Once you open the zip.file, it downloads as an application on your desktop.

Clicking the application opens a web page that asks you to click a blue tab that says, "Create a new wallet."

This leads to a page that asks that you choose and set a password.

Once you've done so, you're asked to choose a form of backup, just in case your laptop is ever lost or stolen. I chose Dropbox as my backup, but the backup application Time Machine is presented as another option.

I then was given the go-ahead to get started with Hive by clicking "Start Here." I did so, and was asked to enter my password.

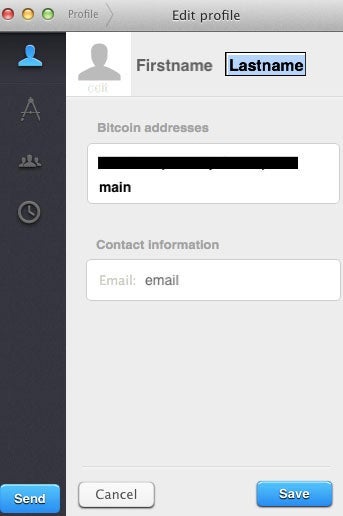

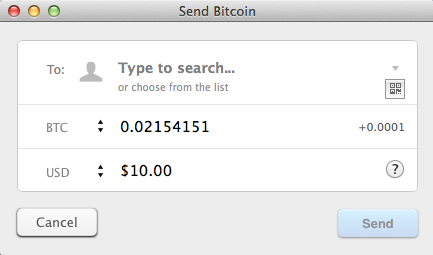

Once inside your digital wallet, you can choose to use your real name or create a username, access your own randomly generated bitcoin address (e.g., transaction signature), and input an email address for notifications. Your wallet also allows you to directly access a handful of smartphone apps and add other bitcoin users' names and bitcoin addresses. Clicking the "Send" button takes you to a screen that allows you to make actual transactions.

Entering a dollar amount in the USD section automatically produces a BTC (bitcoin) amount based on that day's market value. At this writing, the market value of bitcoin is pretty volatile (more on that below), so merchants who accept bitcoin charge for their goods and services in USD rather than BTC.

Making a purchase or paying a bill with bitcoin is similar to the process of paying a bill via online banking or charging something on PayPal. To make bitcoin transactions, both a purchaser and a merchant must have digital wallets - and the purchaser needs to have bitcoins to spend.

How is bitcoin obtained?

Bitcoin can be obtained in three main ways:

You can buy it on an exchange. In a big blow to bitcoin, the largest exchange, Mt. Vox, just filed for bankruptcy on February 25, 2014 amidst a flurry of financial scandal. However, many smaller exchanges remain, including CoinCafe and OKPay, portals which allow you to both purchase and bank bitcoin via PayPal and credit card. Brand new on the scene is Tinkercoin, a Canadian company that began selling bitcoin in limited release in March 2014, allowing individuals to make a one-time-only credit card purchase of $20 worth of bitcoin for $25, charging a $5 processing fee.

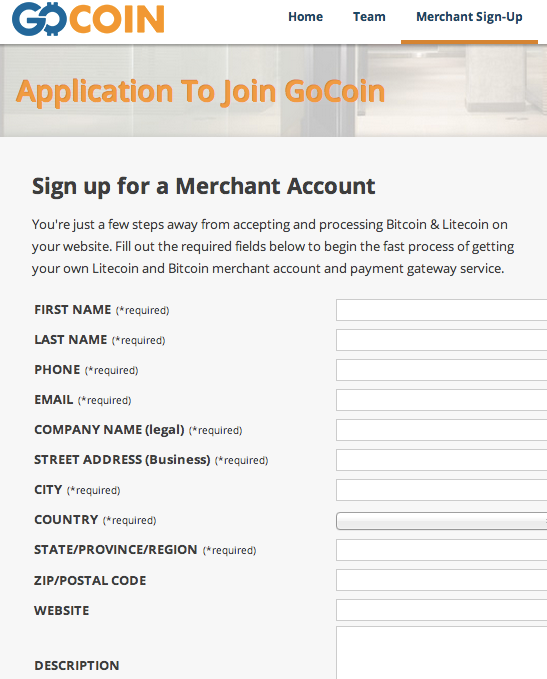

You can earn them through the exchange of goods and services. Bitcoin hasn't yet cracked the shopping mainstream, but all it takes to become a bitcoin-handling merchant is to sign up for a free account with a portal like GoCoin, set up a digital wallet and await approval within 48 hours; you receive an email to confirm your application, and are given an email address to contact if you haven't heard from them within that time. Once you're approved, you simply let potential customers know you accept bitcoin - and you're off to the races.

You can mine them. Each bitcoin deposit to/withdrawal from a digital wallet is assigned an encryption code which must be verified via "mining," a decentralized version of banking. Miners run specialized hardware and software (like GUIMiner or Bitcoin Core) that together attempt to solve complex equations and find keys that unlock encrypted bitcoins mid-transaction; miners who successfully verify these transactions are rewarded with a direct deposit of up to 25 bitcoins into their digital wallets. According to Blockchain.info—a top site for the latest real-time bitcoin transactions - it currently takes almost 1,800,000,000 attempts for this software to find a correct key, and yet, a miner still wins a bitcoin reward about every 10 minutes.

Where can you spend bitcoin?

At present, there are only a few large companies and small businesses accepting bitcoin in exchange for things you'd normally buy with money, from Subway sandwiches to gambling at Las Vegas casinos, as well as the purchase of flights and hotel rooms. Travel-booking portals like Cheapair, BTCTrip and Pointshound now accept bitcoin in exchange for flight and hotel booking, as well as travel agencies like SimplyTravelOnline.com and online vacation rental sites like 9flats.com.

The (travel) pros of bitcoin

Aside from needing nothing more than a smartphone and an app in order to carry it, bitcoin has a couple of key advantages over paper money and credit cards:

Travel currency without conversion or ATM fees. Imagine that you've just landed in a foreign country and can breeze right by the currency conversion desk at the airport, as well as ATM machines all across a destination - saving yourself a bevy of fees in the process. Increased adoption of bitcoin within the travel industry could mean a large reduction in booking fees, as well as eliminating travel wait times for foreign credit card transactions, making it easier for travel-related businesses to manage their revenue stream. At present there aren't enough bitcoin-accepting companies and merchants to justify leaving your cash and credit cards at home, but frequent travelers (and travel companies) seeking a fee-free global currency option could well lead the charge for a wider acceptance of bitcoin.

The (potential) avoidance of payment fraud. A problem both at home and abroad, credit cards that use swipe-strip rather than imbedded chip technology are increasingly at risk for fraud. (The safer chip technology is becoming more common overseas, but North America is still way behind the curve.) Bitcoin requires neither, only a relatively (see below) secure, nameless and wireless connection between encrypted digital wallets.

Instead of earning points and miles, you could earn bitcoins. At present, PointsHound.com is one of the few travel-related companies that allows you to earn bitcoins for hotel stays - instead of points. An option available for bookings at more than 150,000 hotels worldwide, the amount of bitcoin received will vary depending on the status of different hotel rooms and users, but at current exchange rates a frequent PointsHound user could earn as much as 1/4 bitcoin for a three-night stay at a high-end hotel. With the current devaulation of so many frequent flyer programs, earning bitcoins rather than miles or points could eventually be a more valuable loyalty option.

The cons of bitcoin

This form of currency also has some serious drawbacks and challenges:

Its anonymous nature makes it the currency of choice for illicit trade. Had the TV show Breaking Bad lasted another season, it was only a matter of time before bitcoin became a plot point. In most cases, the purchase of bitcoin requires neither a real name nor a credit card, and as mentioned above, transactions are assigned encryption codes that must be verified by miners. While this transaction system is largely secure from hackers and fraud, it also means that anyone can buy anything from anyone. Just recently, for instance, Ross Ulbricht, the alleged owner of online black-market drug portal the Silk Road, was busted by the FBI to the tune of $28.5 million worth of bitcoin. Cases like these don't do much to raise the profile of digital currency.

The IRS just got its hands on it. Until recently, bitcoin wasn't subject to any taxes or government regulations, but big news has arrived just in time for the 2013 tax season: the IRS recently classified bitcoin as property rather than currency, requiring bitcoin payments made to contractors and service providers to be reported via 1099 and making it subject to capital gains tax.

Transactions are in fact susceptible to hackers. Though they're encrypted, bitcoin transactions have historically proven to be less than airtight: if a skilled hacker can find a way into your digital wallet, they can take your bitcoins. The same sort of fraud happens with regular banks and credit card companies, but they are generally better insured, meaning you're less likely to be permanently parted from your money.

It might just be the new dot.com bubble. Just like other currencies, the worth of bitcoin can fluctuate wildly in relation to world events and financial news. Just last week at the Inside Bitcoins conference in New York, reps from Bloomberg's World Stock Index expressed confidence in the potential value of bitcoin and may soon choose to quote it, but in the meantime, the trading value has seen huge spikes and drops. For instance, between October and November 2013, the trading price rocketed from $100 to what Bank of America analysts determined was a fair market value of $1,300 per bitcoin. However, by April 2014 this value had fallen to below $400, in response to the announcement that China's two largest bitcoin exchanges would be shut down on April 15 due to fear of dangerous speculation.

The future of bitcoin and digital currency

Bitcoin isn't the only player on the field of digital currencies (or cryptocurrencies in popular parlance): it shares its space with Litecoin, Dogecoin, Mastercoin and many more. Several factors continue to stoke consumer interest in alternative financial systems, including a post-2008 lack of trust in banking institutions and credit card data breaches like those at Target in late 2013, so it seems that digital currencies - even if not ultimately bitcoin itself - are here to stay.

The cryptocurrency landscape will surely see increased regulation, as the public adoption of any one form on a large scale could threaten the control and earning potential of our current financial institutions. However, if bitcoin or one of its contenders manages to gain a serious foothold in the global marketplace, almost every financial aspect of travel could become easier, from booking and dining to making overseas purchases and securing local transportation. It'll be interesting to see what happens in the wake of this year's IRS ruling that bitcoin is property rather than currency, and how the digital currency landscape responds to public perceptions of its usefulness and security.

Have any of you used bitcoin to book travel or other purchases? Please share your experiences in the comments below - we'd love to hear about the pros and cons straight from our readers.

[card card-name='Ink Plus® Business Credit Card' card-id='22129636' type='javascript' bullet-id='1']