Sunday Reader Question: Cash Back Versus Travel Credit Cards?

Update: Some offers mentioned below are no longer available. View the current offers here.

This question comes from TPG reader Jason who asks:

"Can you discuss the major differences between cash back credit cards and travel points credit cards? Obviously travel cards are best for people who like to travel, but do you ever find that it makes more sense to use a cash back card rather than a points earning card?"

As usual, the decision between getting a cash back card like the Discover More card or the Capital One Venture Rewards Credit Card and a travel points credit card like the Chase Sapphire Preferred Card comes down to what exactly you want out of your card.

Cash back cards like the Discover More offer you 1% cash back on most purchases, 5% on certain spending categories that change periodically, and between 5-20% on purchases made through the Discover online shopping mall. This cash back comes in the form of gift cards, merchandise or statement credits. The great thing about cash back like this is you know exactly the amount of return you're getting on each and every dollar that you spend, and if you're just looking for a way to get some credit back on your monthly statement, this is a good card for you.

The Capital One Venture Rewards Credit Card is kind of like a cash back and points hybrid card that allots cardholders fixed-value points based on the money that they spend. Cardholders earn 2 points for every dollar that they spend on this card, which can be redeemed for travel at a rate of 1 cent per point. So essentially you're getting 2% cash back to be used on travel booked through Capital One. The good thing about these points is that there is no blackout dates and you still earn elite status on flights purchased with these points since it's just like paying for them. However, you can only get 1 cent per point in value, which doesn't change, so it's extremely expensive to use them for premium travel. These points are great for travelers who want to travel in economy and need the flexibility of purchasing any seat on any flight on the exact dates that they need.

Where travel credit cards like the Sapphire Preferred excel is in the ability to reap a huge amount of value per point by using these points to book premium awards that would simply be too expensive to purchase using fixed-value points. Cards like this one, or the Premier Rewards Gold Card from American Express or Platinum cards, which bank points to American Express Membership Rewards, have the added bonus of having multiple airline and hotel partners, so you can use them on a variety of airlines or at your hotel chain of choice as long as it's a partner of the program. These cards present their cardholders with a huge amount of flexibility in terms of the number of rewards and the the number of partners that their points can be used to book.

Two Examples

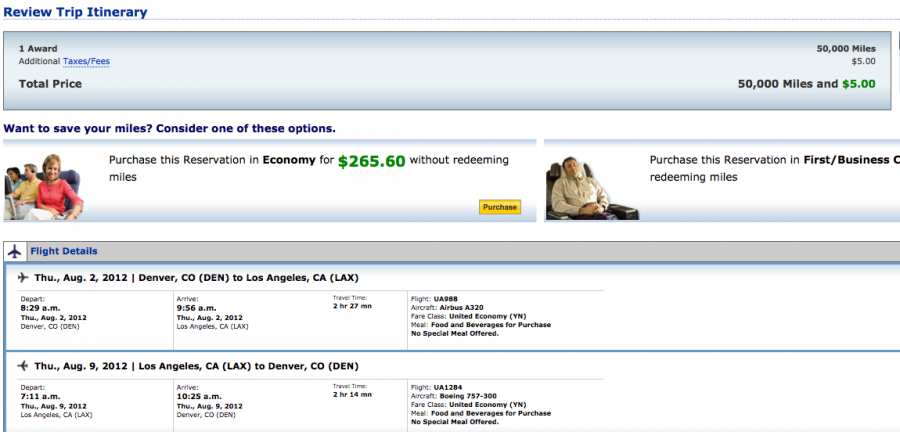

As I mentioned, a fixed-value card like the Capital One Venture excels when you have exact flights, dates and destinations you need to get to and you want to fly economy. So, for instance, this roundtrip United itinerary from Denver to LAX in August would cost you 25,650 points at 1 cent per point for the $256.50 fare.

Using Chase Ultimate Rewards points converted to United miles, that same itinerary would cost you 50,000 miles and $5 in taxes because there isn't low-level award availability for these flights.

Just to look at the opposite scenario. If you remember, I gave myself a birthday present of a one-way business class ticket from Newark to Singapore aboard Singapore Airlines by converting 60,000 Chase points to United miles and redeeming them for their partner airline plus $2.50 in taxes. That same ticket would have cost $4,556, so I got 7.6 cents per point in value. If I were to use Capital One Venture Rewards points, I'd have to spend 455,600 points to get that same ticket - nearly 8 times as many points!

The two examples are stark contrasts. If you like having a fixed value on your points that you can then use for the exact flights you want on the exact dates you want, then you should consider a cash back card like the Capital One Venture. However, if your primary goal is to squeeze as much value as possible out of each point by redeeming for premium awards, then you should consider travel points credit cards such as the Sapphire Preferred and the Premier Rewards Gold.