Capital One Venture Rewards Credit Card review: Simple elevated earnings, low annual fee

Editor's Note

I added the Capital One Venture Rewards Credit Card to my wallet over 10 years ago for its simple earning rates and modest $95 annual fee.

It has remained a valuable mid-tier travel rewards card due to its straightforward earning rates and no foreign transaction fees. Plus, you have multiple ways to redeem your rewards, including covering recent travel purchases at a fixed rate and transferring your miles to any of the 15-plus Capital One airline and hotel partners. Card rating*: ⭐⭐⭐⭐½

*Card rating is based on the opinion of TPG's editors and is not influenced by the card issuer.

Capital One Venture Rewards Credit Card: The basics

The Capital One Venture Rewards offers at least 2 miles per dollar spent on every purchase, making it an excellent everyday spending card. Plus, it offers 5 miles per dollar spent on hotels, vacation rentals and rental cars booked through Capital One Travel. These earning rates make the Capital One Venture Rewards card an appealing and good option for consumers who want to use one card for all their purchases.

Unlike many of the other best everyday spending cards, the Venture Rewards card stands out by offering no foreign transaction fees. The card carries a $95 annual fee but offers a $50 experience credit on every Lifestyle Collection booking, complimentary Hertz Five Star status and up to a $120 statement credit (every four years) when you use your Venture card to apply for Global Entry or TSA PreCheck. Plus, cardholders enjoy price prediction and free price drop protection when booking flights through Capital One Travel.

The Capital One Venture Rewards earns miles that you can redeem for travel, cash back, gift cards, experiences and more. But you can also transfer your miles to 15-plus travel loyalty programs, including Air Canada Aeroplan, Air France-KLM Flying Blue and Choice Privileges.

Related: 7 reasons to get the Capital One Venture Rewards card

Capital One Venture Rewards Credit Card pros and cons

| Pros | Cons |

|---|---|

|

|

Related: Why I keep the Capital One Venture Rewards card in my wallet

Capital One Venture Rewards Credit Card benefits

The Capital One Venture Rewards offers cardholders several benefits that help offset the card's $95 annual fee.

Price prediction and free price drop protection

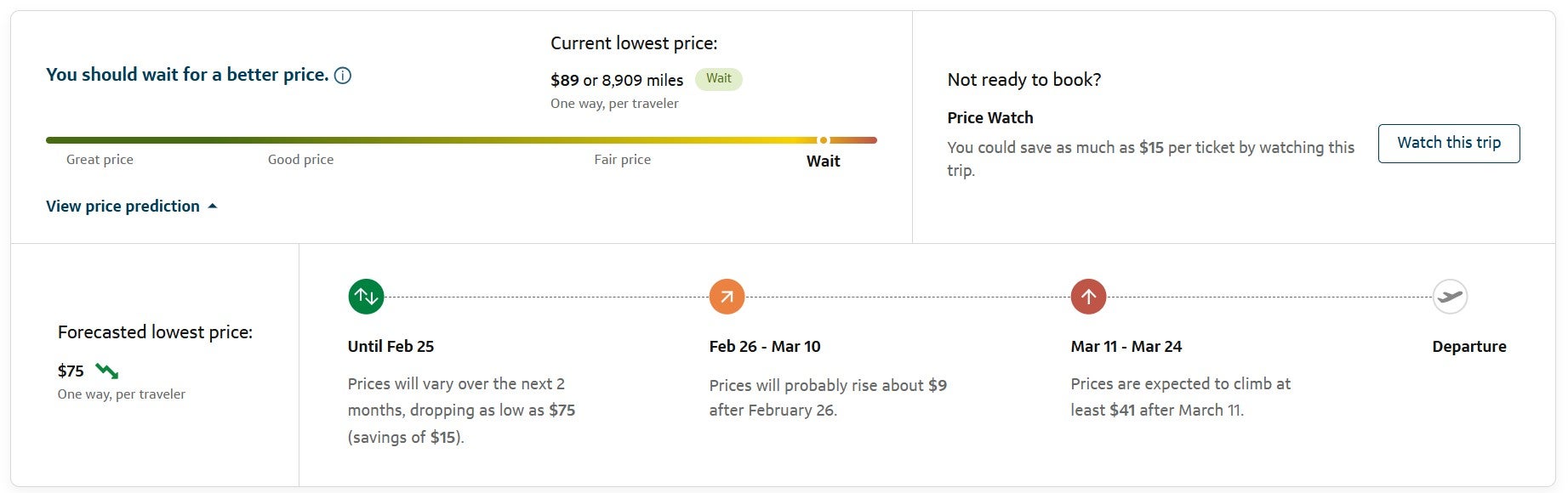

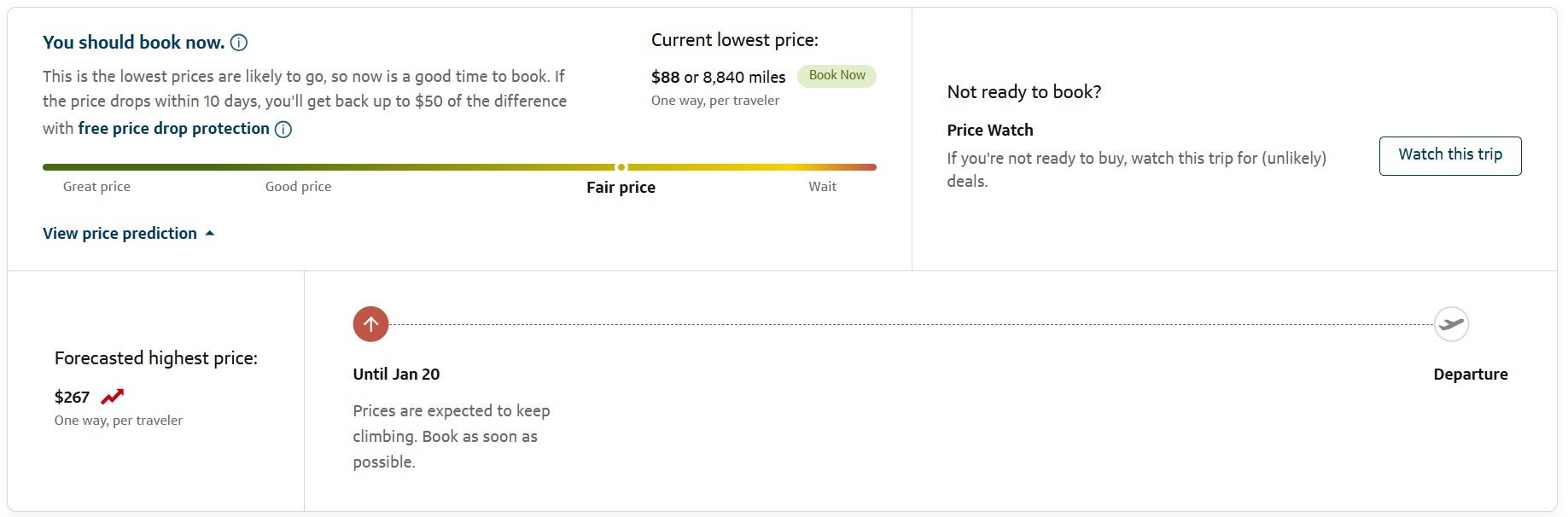

One of my favorite benefits of the Capital One Venture Rewards is the price prediction and free price drop protection that's available when I book flights through Capital One Travel.

The price prediction appears anytime you search for a flight through Capital One Travel. It provides guidance on whether to book now and also estimates how pricing is likely to change if you wait to book.

If the price prediction advises booking now, Capital One Travel will automatically apply price drop protection to that purchase at no additional charge. Then, you'll receive up to $50 of the difference back if the price drops within 10 days.

These two features often give me the confidence I need to book or continue to track prices. I've gotten money back on several flights via the automated price drop protection, which is always a nice surprise.

Price match guarantee on select travel bookings

You also have some protection if you book a flight, hotel or rental car through Capital One Travel and then find a better price for the same flight, hotel or rental car on another site within 24 hours of booking. Specifically, you can call Capital One Travel, submit a price match claim and then get a travel credit for the difference if the agent can verify the lower price.

I've successfully done price match guarantees for several flights, with the phone calls often taking under 10 minutes. Keep in mind, though, that the itinerary must be an exact match to what you booked on Capital One Travel, and you must submit your claim within 24 hours of making your reservation through Capital One Travel. The price must be in dollars and available to the general public without any coupons, promotions or member discounts.

Global Entry or TSA PreCheck statement credit

Capital One Venture Rewards cardholders receive up to a $120 statement credit every four years for the application fee for either Global Entry or TSA PreCheck. The credit will apply to whichever program is applied to first, so consider your application timing if you plan to pay for applications to both programs with your card.

I love having Global Entry, as it lets me get through U.S. immigration queues quickly, and it also gives me TSA PreCheck. I'd pay the Global Entry application fee even if my Capital One Venture Rewards card didn't offer a statement credit, so this perk effectively gives me (up to) $120 back every four years.

Complimentary Hertz Five Star status

Capital One Venture Rewards cardholders can enroll in complimentary Hertz Five Star status through the "Benefits" tab of the Capital One website or mobile app. However, it may take up to 72 hours after you register for Hertz status for the upgrade to take effect, so don't wait until you're about to pick up your rental car to register.

I like having Hertz Five Star status, as it provides upgrades when available, 25% more points and a wider choice of vehicles at Ultimate Choice locations.

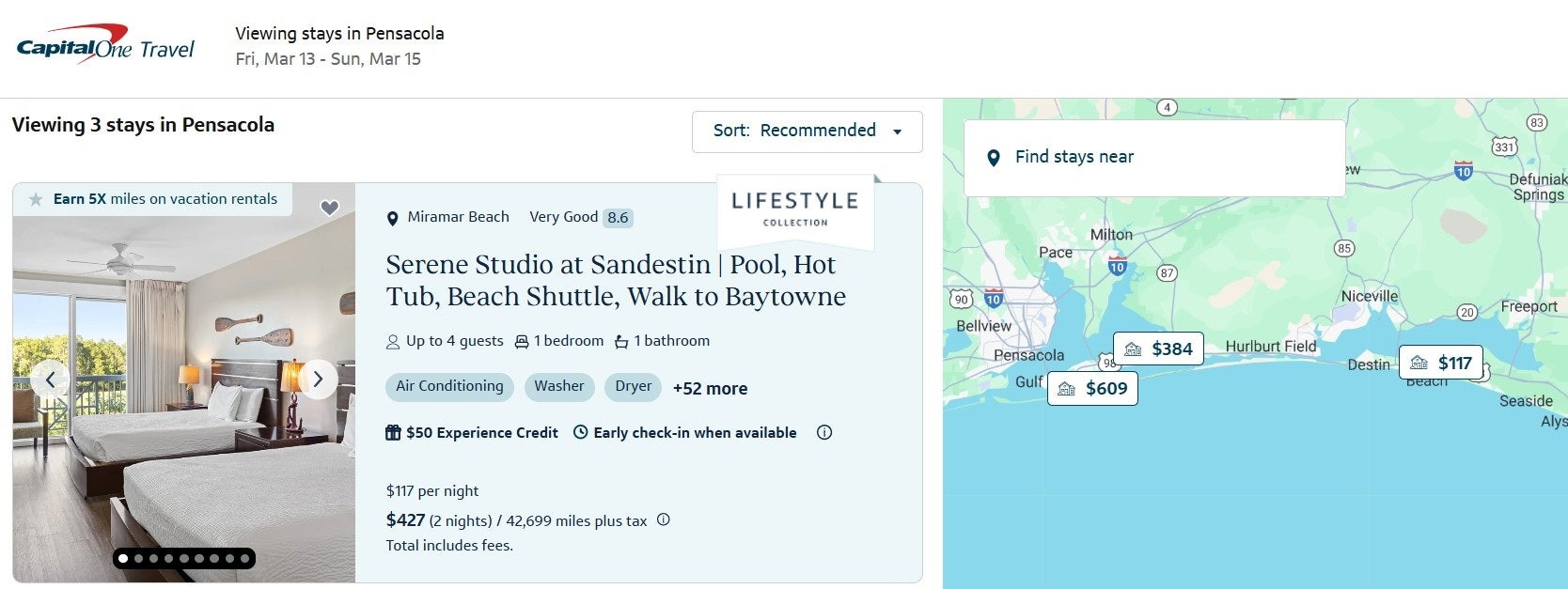

Perks on eligible Lifestyle Collection stays

Each time you make an eligible Lifestyle Collection booking through Capital One Travel, you'll get a $50 experience credit to enjoy during your stay. The booking must be made in the cardholder's name, and the cardholder must be staying on the eligible booking.

If you are staying at a hotel, the hotel will apply the credit at checkout to qualifying charges up to $50. Check with the hotel to determine which charges are qualifying, and then charge qualifying charges to your room during your stay. If you're staying at a vacation rental, the host provider will apply the credit when you book an eligible experience with a Capital One credit card. However, at some vacation rental properties, you may get the experience credit as a gift card.

You'll also enjoy other perks on eligible Lifestyle Collection stays, including complimentary Wi-Fi, early check-in and late checkout. However, early check-in and late checkout are only provided when available, and bookings may have a minimum stay requirement. At hotels, you are also eligible for a room upgrade (subject to availability).

Capital One Dining and Entertainment

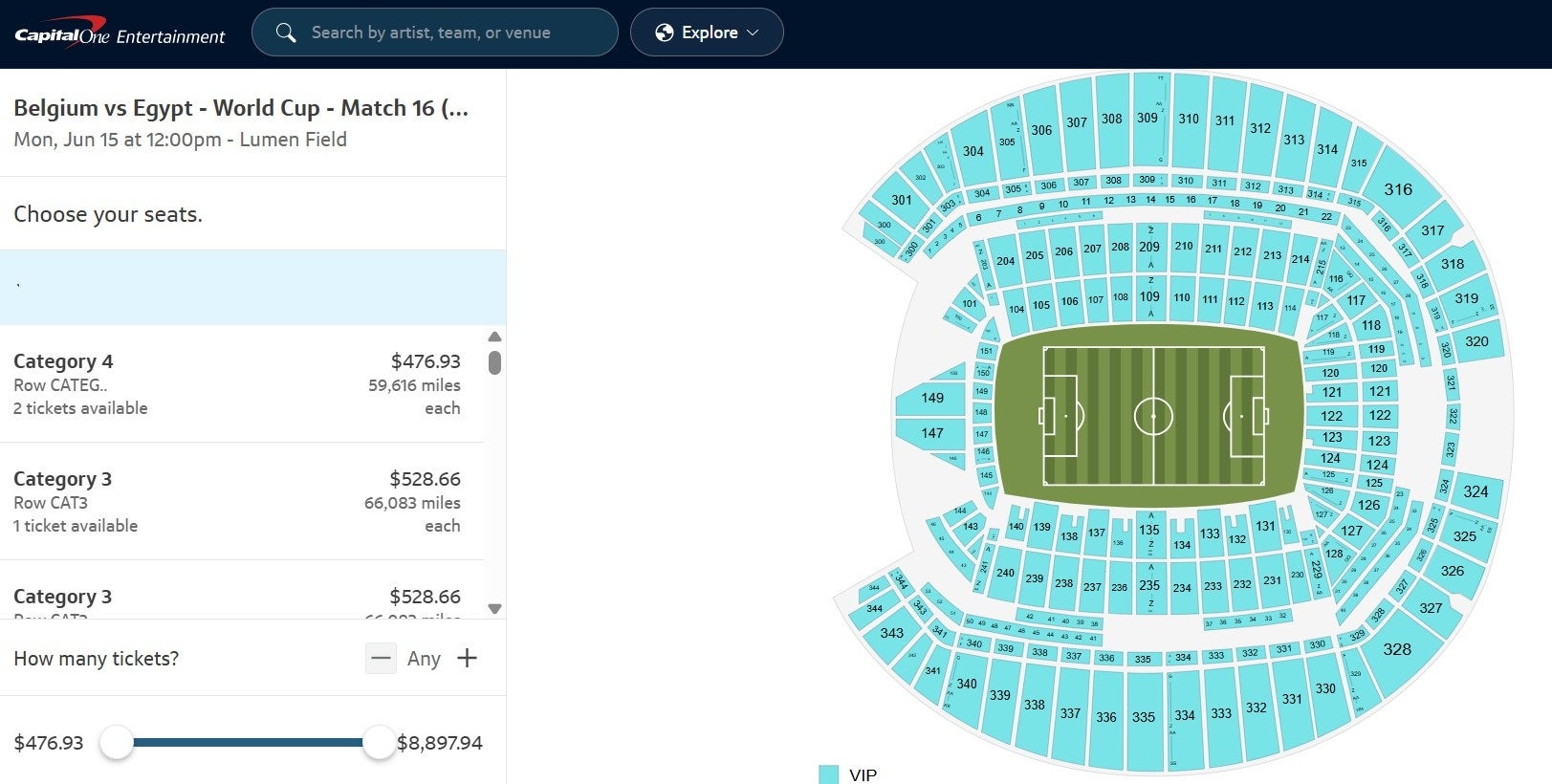

Capital One Venture Rewards cardholders also get access to Capital One Dining and Capital One Entertainment.

The entertainment platform may be your ticket to cardholder-only VIP packages and hard-to-secure tickets to popular games, concerts and shows. For example, you can secure tickets for the upcoming FIFA World Cup through Capital One Entertainment.

Meanwhile, the dining platform can help you secure hard-to-get reservations at top restaurants and provide access to exclusive dining events.

Related: Is the Capital One Venture Rewards card worth it?

How to earn and use your rewards

Capital One miles are easy to earn and redeem yet still offer significant value. Here's what you should know about earning and redeeming Capital One miles.

Earning miles

The Capital One Venture Rewards offers simple-to-remember earning rates. Specifically, you'll earn 5 miles per dollar spent on hotels, vacation rentals and rental cars booked through Capital One Travel and 2 miles per dollar spent on all other purchases.

These earning rates make the Capital One Venture Rewards an excellent option, whether it's your only card or you use it primarily for purchases that wouldn't earn bonus rewards on other cards. I often use my Capital One Venture Rewards for purchases that would earn just 1 point or mile per dollar spent if I used another rewards credit card.

Redeeming miles

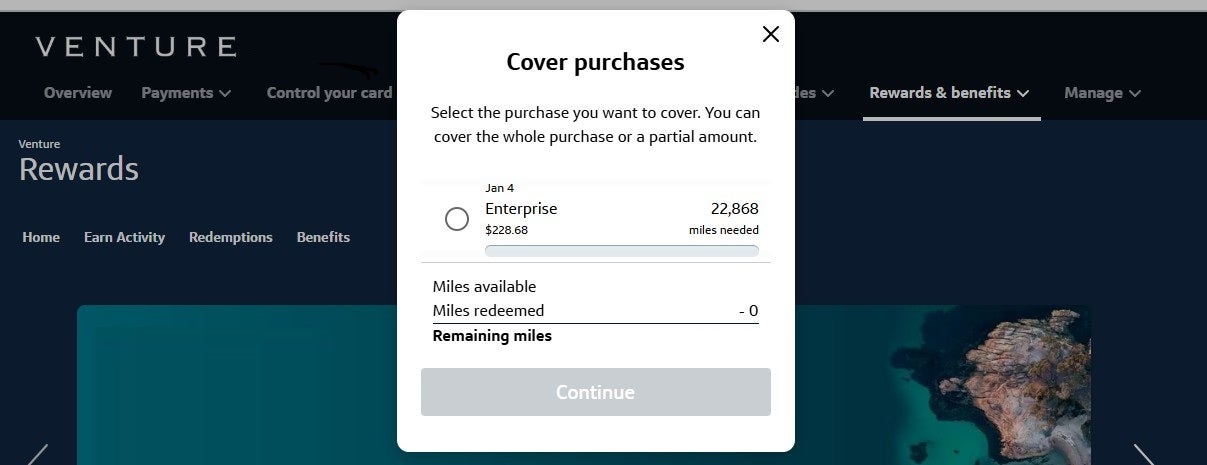

One of the big positives of the Capital One Venture Rewards is the flexibility of its miles. However, the two best ways to redeem Capital One miles are to cover recent travel purchases and to transfer earnings to select airline or hotel loyalty programs.

Redeeming Capital One miles to cover recent travel purchases gives you 1 cent per mile and is incredibly easy. Once you make an eligible travel purchase with your card, you'll have 90 days to log into the Capital One app or website and redeem rewards to cover your purchase.

However, I prefer to redeem my miles by transferring them to the 15-plus Capital One airline and hotel program partners. Some of my favorite options include Air France-KLM Flying Blue, Air Canada Aeroplan and Avianca LifeMiles, but you also have access to JetBlue TrueBlue, Wyndham Rewards and many other programs. I recently redeemed 80,000 Air Canada Aeroplan points (along with $85 in taxes and fees) to fly in business class from Cape Town to Perth, Australia, on an itinerary that would have otherwise cost $2,233.

As long as you get more than 1 cent per mile when transferring miles to partners, this is the most valuable redemption option. However, TPG's January 2026 valuations peg the value of Capital One miles at 1.85 cents each. So, you'll usually want to choose airline or hotel programs that offer at least this much value for your miles when you transfer them.

Related: Have the Capital One Venture Rewards Card but new to points and miles? Here's what you need to know

Downsides of the Capital One Venture Rewards Credit Card to consider

The Capital One Venture Rewards won't be the right card for everyone. Here are some drawbacks to keep in mind:

- You'll only earn 2 miles per dollar spent on most purchases (only hotels, vacation rentals and rental cars booked via Capital One Travel earn 5 miles per dollar spent).

- There are no airport lounge benefits.

- There are no annual statement credits or miles to help offset the annual fee.

- JetBlue is the only U.S. airline that is a transfer partner.

If the lack of airport lounge benefits and potential difficulty in offsetting the annual fee are your primary concerns about the Capital One Venture, it may be worth considering the Capital One Venture X Rewards Credit Card instead.

Capital One Venture Rewards vs. Venture X

The Capital One Venture X has a higher annual fee ($395) than the Venture ($95), but it offers $300 in annual credits toward bookings made through Capital One Travel. Therefore, theoretically, the annual fee of the two cards is the same, provided you book at least $300 of travel through Capital One Travel each account anniversary year.

Venture X cardholders also get 10,000 bonus miles on each account anniversary, starting with the first anniversary. Between the bonus miles and the annual travel credit, most consumers will get more value than the card's annual fee each year.

Plus, the Venture X offers 10 miles per dollar spent on hotels and rental cars booked through Capital One Travel, 5 miles per dollar spent on flights and vacation rentals booked through Capital One Travel and 2 miles per dollar spent on all other purchases. Capital One Venture X cardholders also get access to Priority Pass lounges and Capital One lounges.

Choose the Capital One Venture X if you prioritize:

- Credits and miles that can offset the annual fee

- Higher earning rates on some types of travel booked through Capital One Travel

- Access to Priority Pass and Capital One airport lounges

Choose the Capital One Venture Rewards if you prioritize:

- Paying a lower annual fee

- Potentially easier approval (especially if you have good, but not excellent, credit)

Related: Capital One Venture Rewards vs. Capital One Venture X: Worth the extra $300?

When to apply for the Capital One Venture Rewards Credit Card

You'll want to apply for the Capital One Venture Rewards Credit Card when its welcome offer is 75,000 miles or higher. We've only seen offers higher than 75,000 miles in airports from June 2023 to July 2024, and these offers were targeted.

As such, the current welcome offer is worth considering: Earn 75,000 bonus miles after spending $4,000 on purchases within the first three months from account opening.

However, Capital One won't approve you for a new Capital One Venture Rewards card if you opened a Venture Rewards or Venture X card and earned a bonus in the last 48 months. So, you'll need to wait at least 48 months after earning a welcome bonus on either of these cards before you apply for the Capital One Venture Rewards.

Related: Are you eligible for the Capital One Venture Rewards' welcome bonus?

Cards to consider if you don't want the Capital One Venture Rewards

If the Capital One Venture Rewards isn't right for you, here are a few other cards to consider:

- Capital One VentureOne Rewards Credit Card: The no-annual-fee sibling to the Venture also offers elevated earning rates; cardholders can earn 5 miles per dollar spent on hotels, vacation rentals and rental cars booked through Capital One Travel and 1.25 miles per dollar spent on all other purchases. Check out our full Capital One VentureOne review to learn more.

- Citi Double Cash® Card (see rates and fees): This no-annual-fee option from Citi offers at least 2% cash back on all purchases (provided as 1% cash back when you buy and 1% when you pay). Check out our full Citi Double Cash review to learn more.

- Chase Sapphire Preferred® Card (see rates and fees): With this Chase card, you'll enjoy more bonus categories and travel protections but lower earning rates on everyday spending. Check out our full Chase Sapphire Preferred review to learn more.

For other options, read our story on the best starter travel credit cards.

Related: How to pick the right travel credit card for you

Bottom line

The Capital One Venture Rewards Credit Card remains a popular travel rewards card due to its modest $95 annual fee, its simplicity and its flexibility.

If you only want one card or are looking for a card for purchases that don't earn bonus rewards on other cards, the Capital One Venture Rewards is a good choice. Plus, you can use rewards from the card at a fixed rate of 1 cent per mile or opt to transfer to any of the 15-plus Capital One travel partners.

This simplicity and flexibility are why I've kept the card for over 10 years.

Learn more: Capital One Venture Rewards Credit Card